Question: Answer and give an explanation, please 1. The minimum possible average total cost of producing generic antidepressant medication in the long run is $10 per

Answer and give an explanation, please

1.

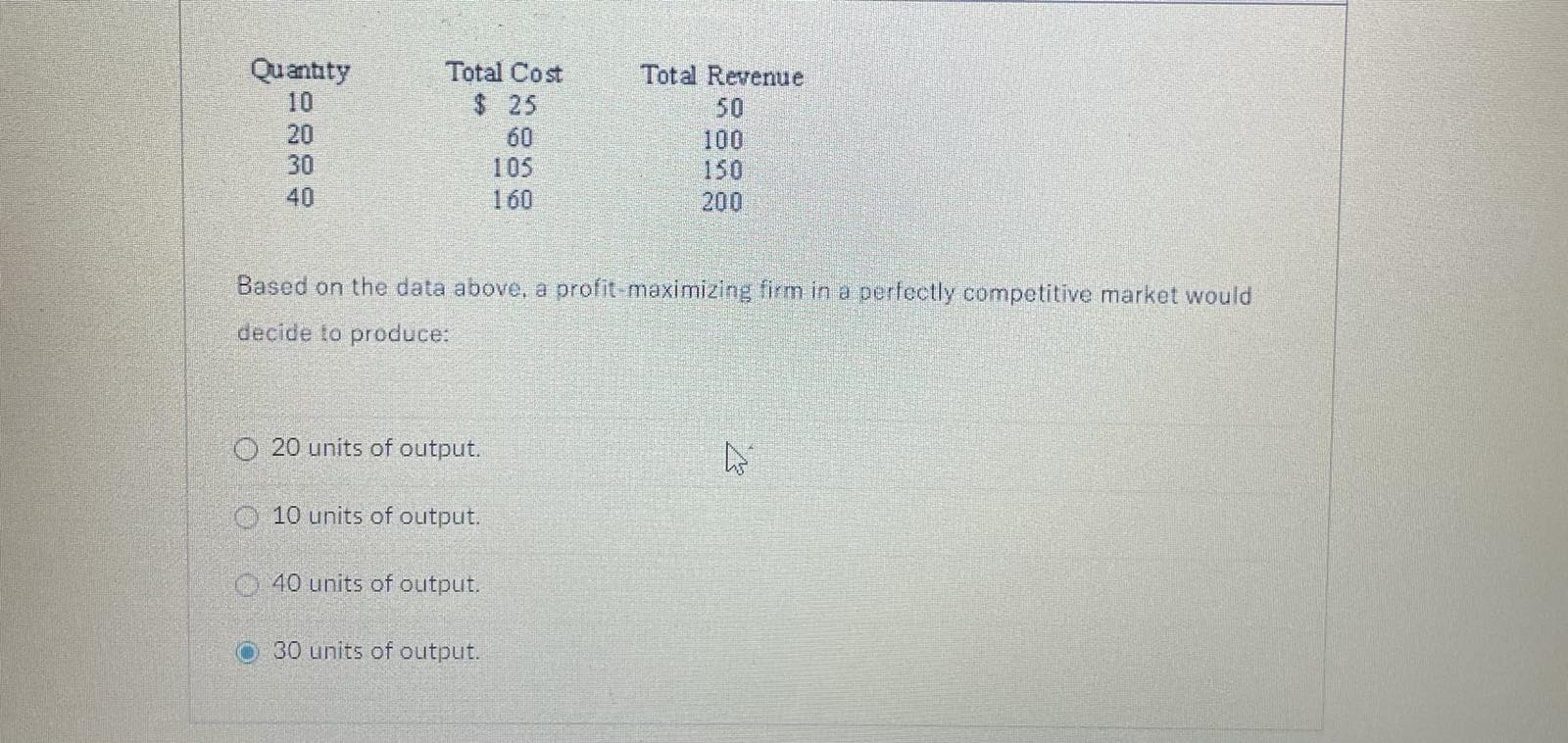

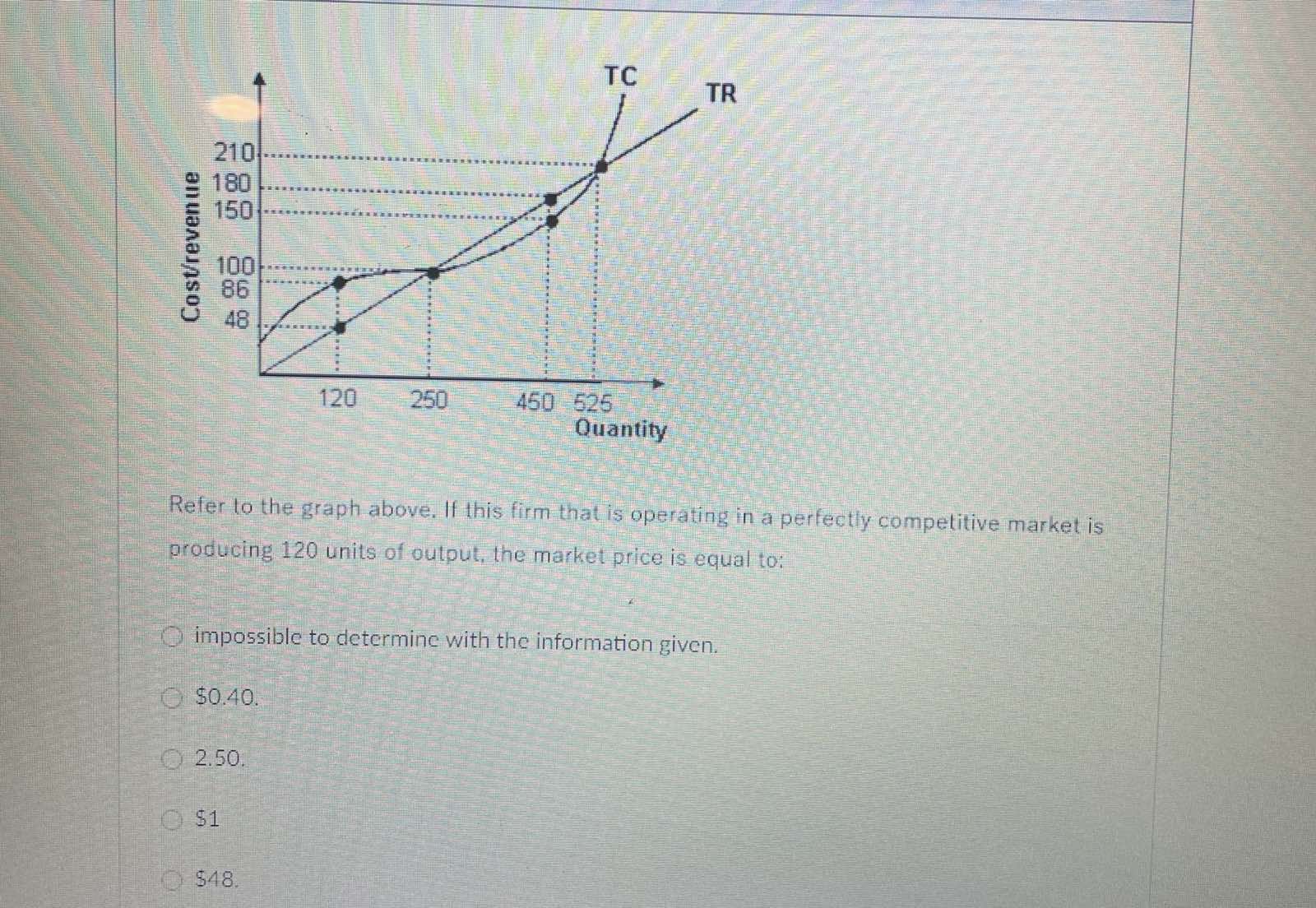

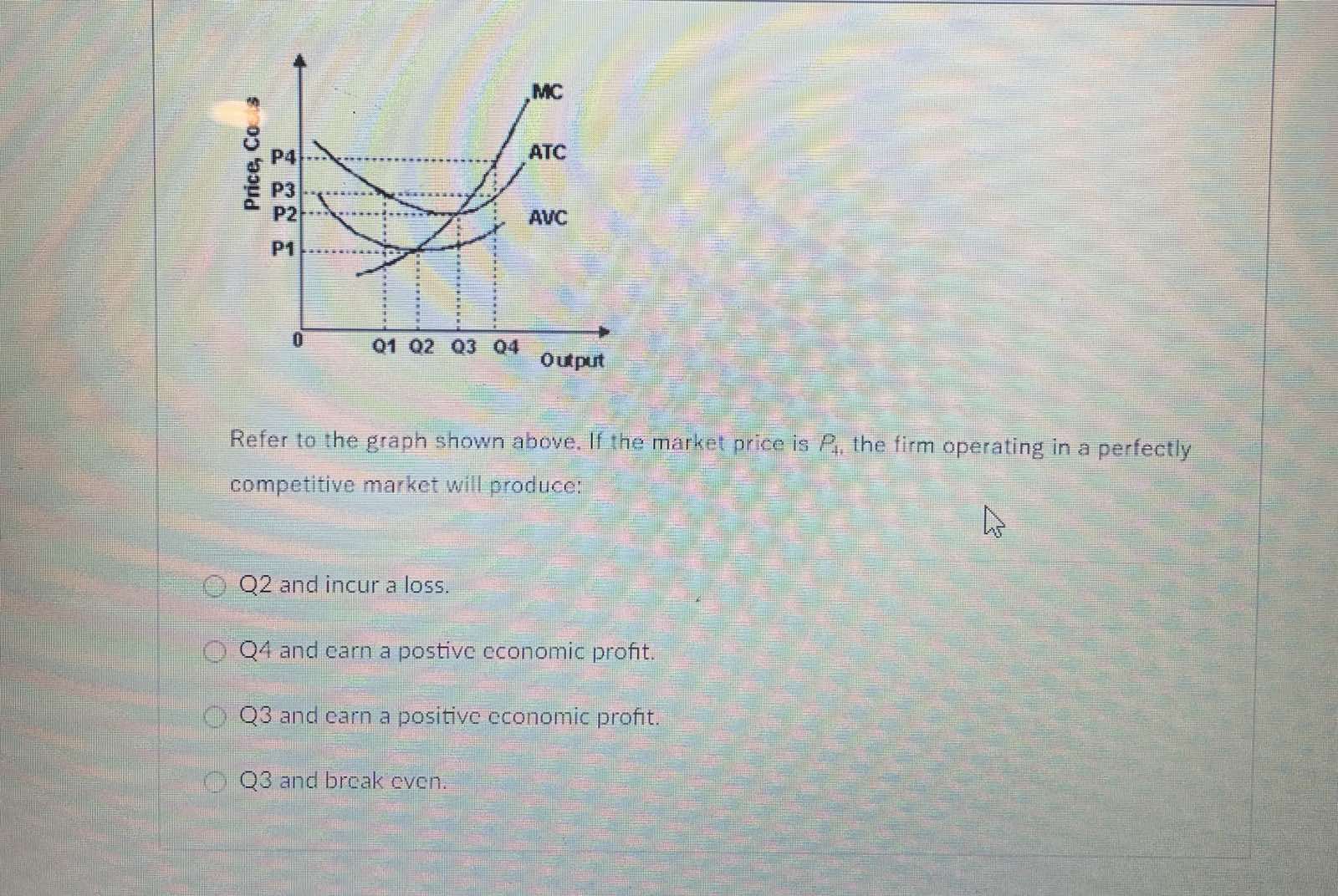

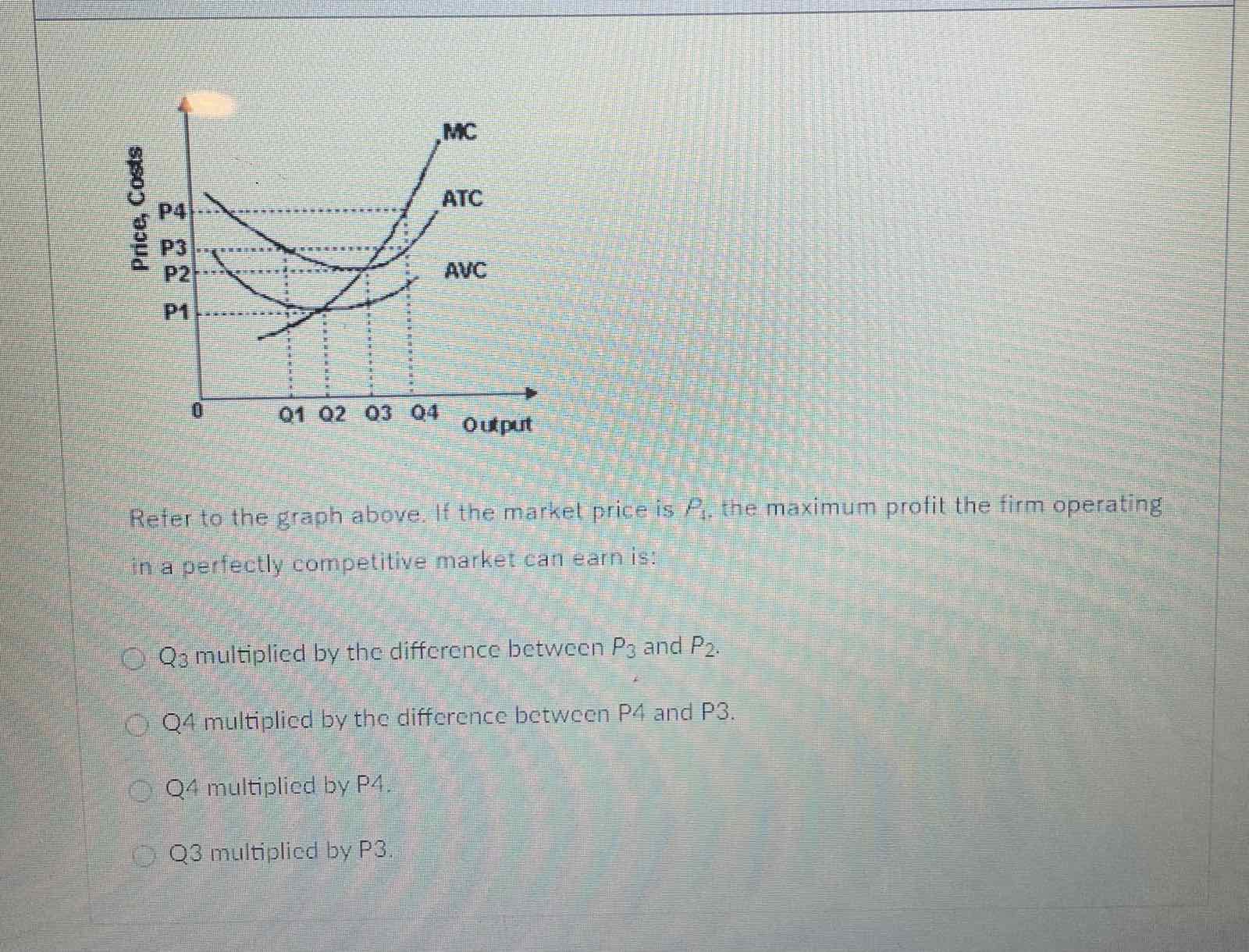

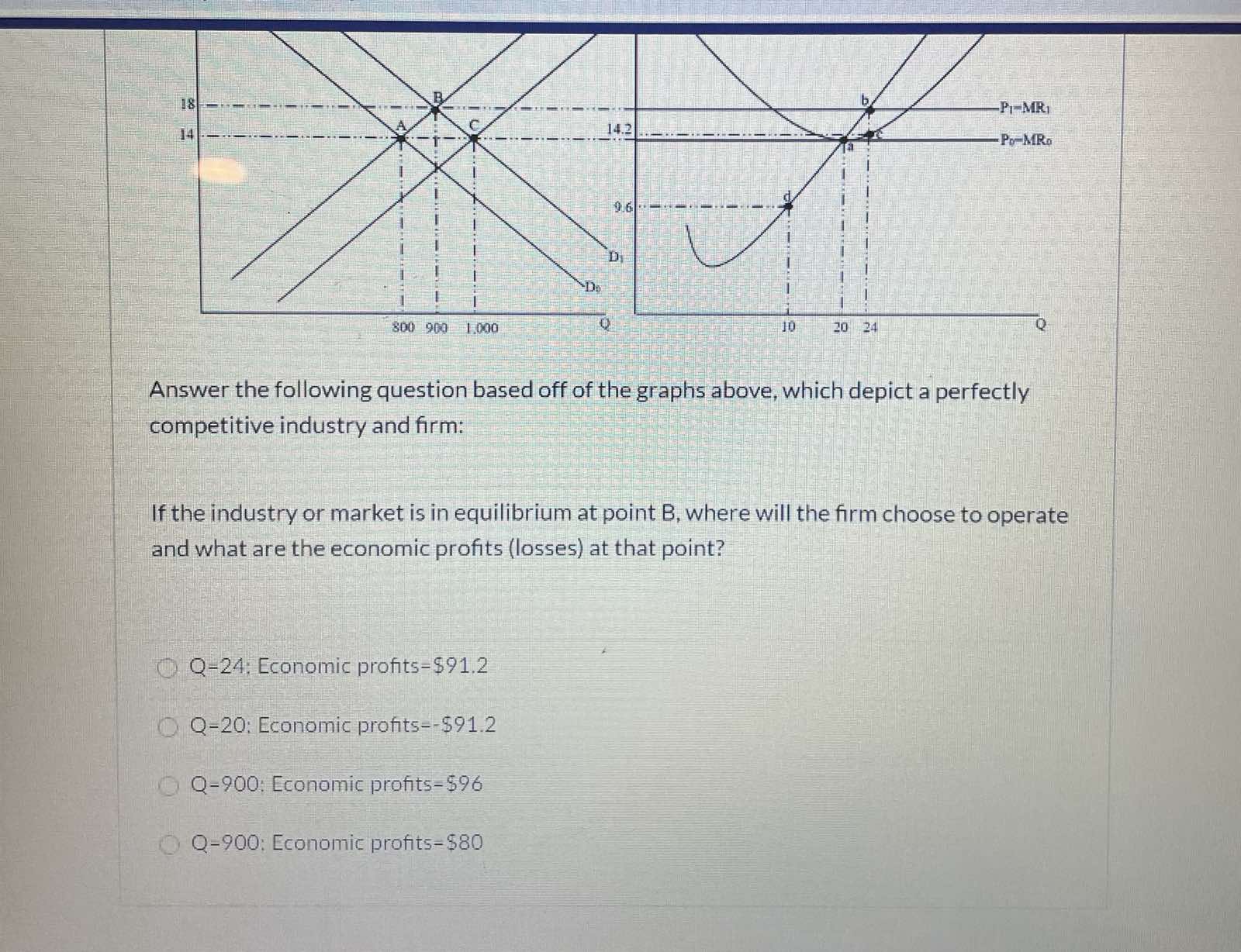

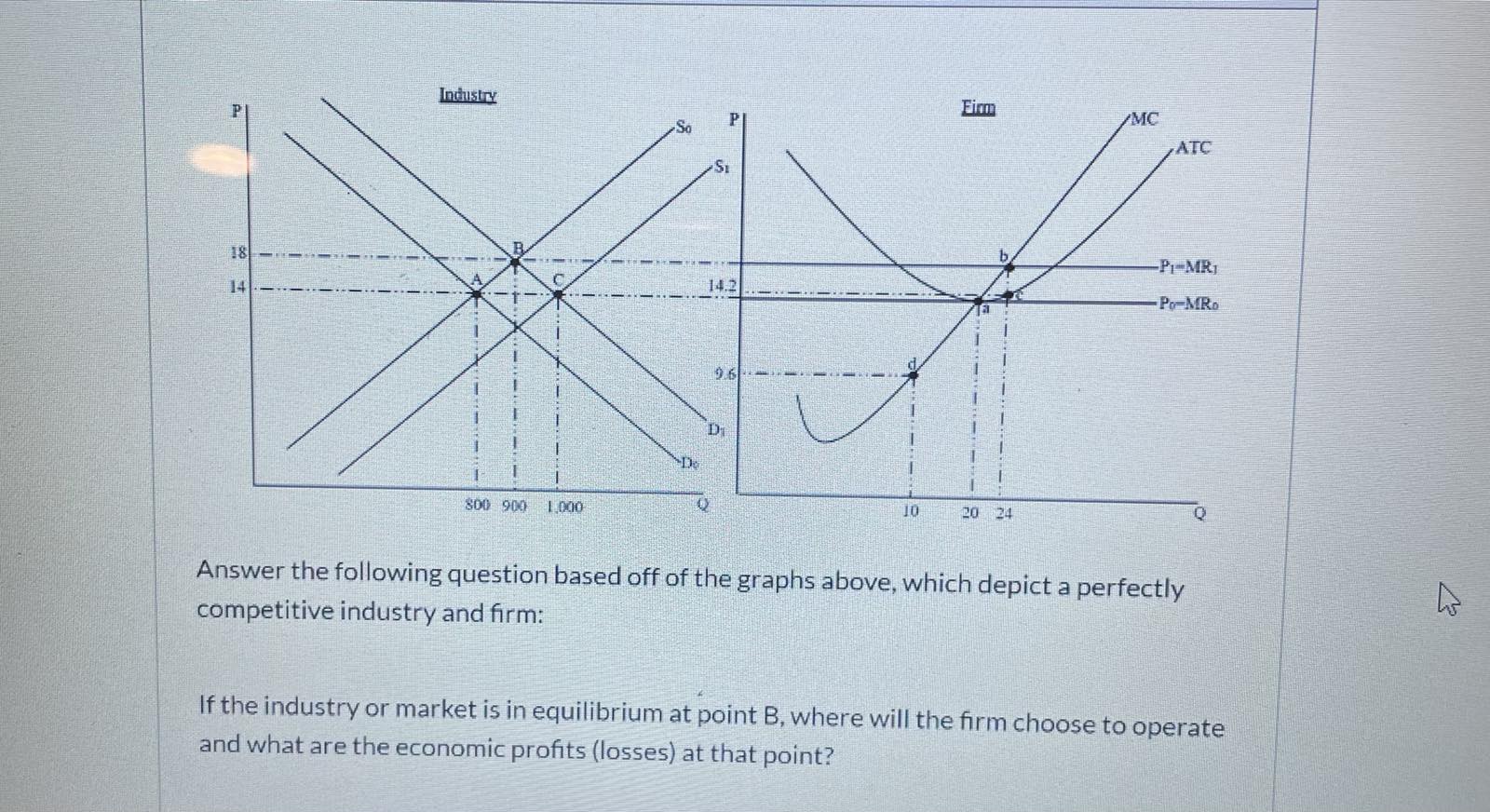

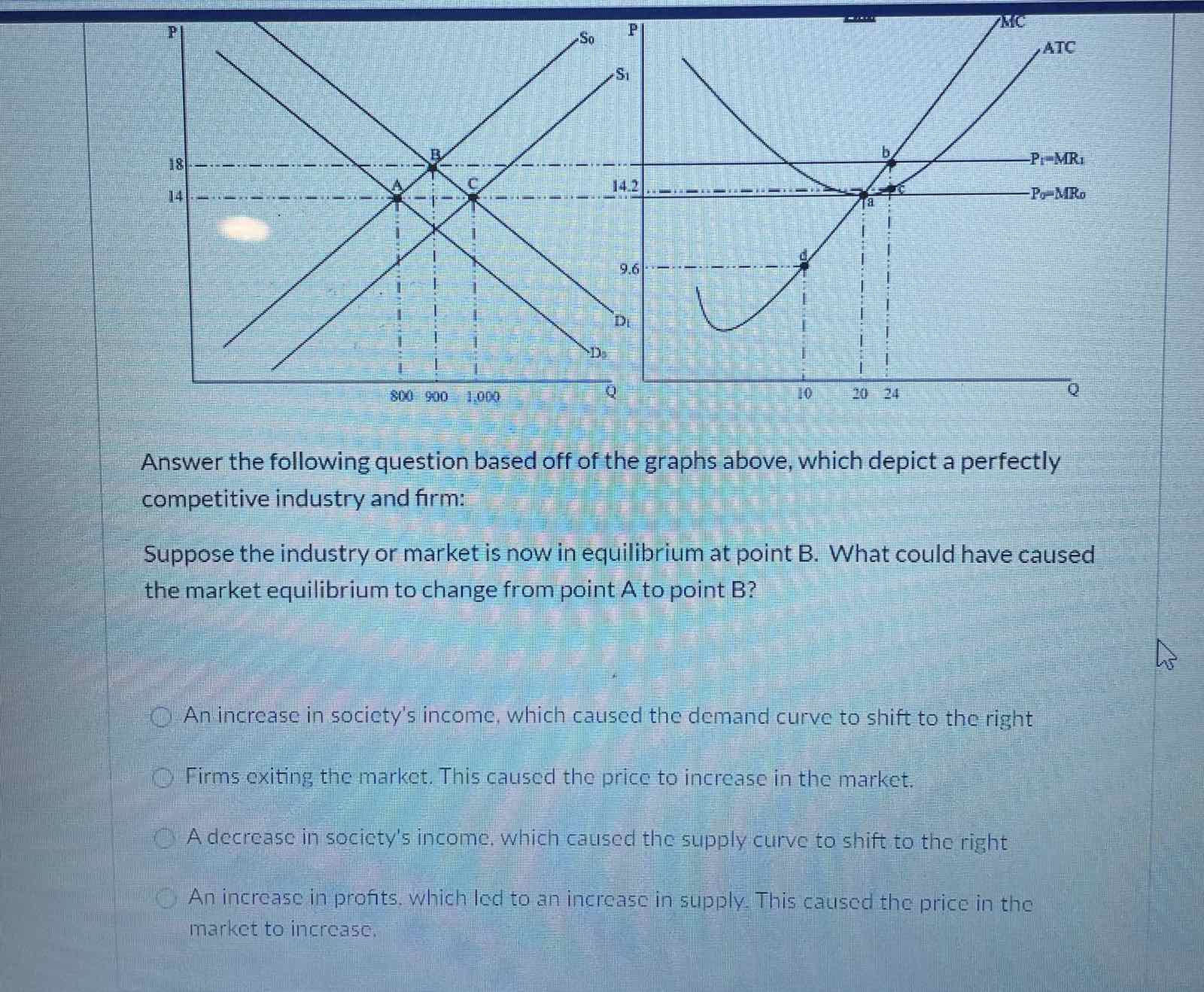

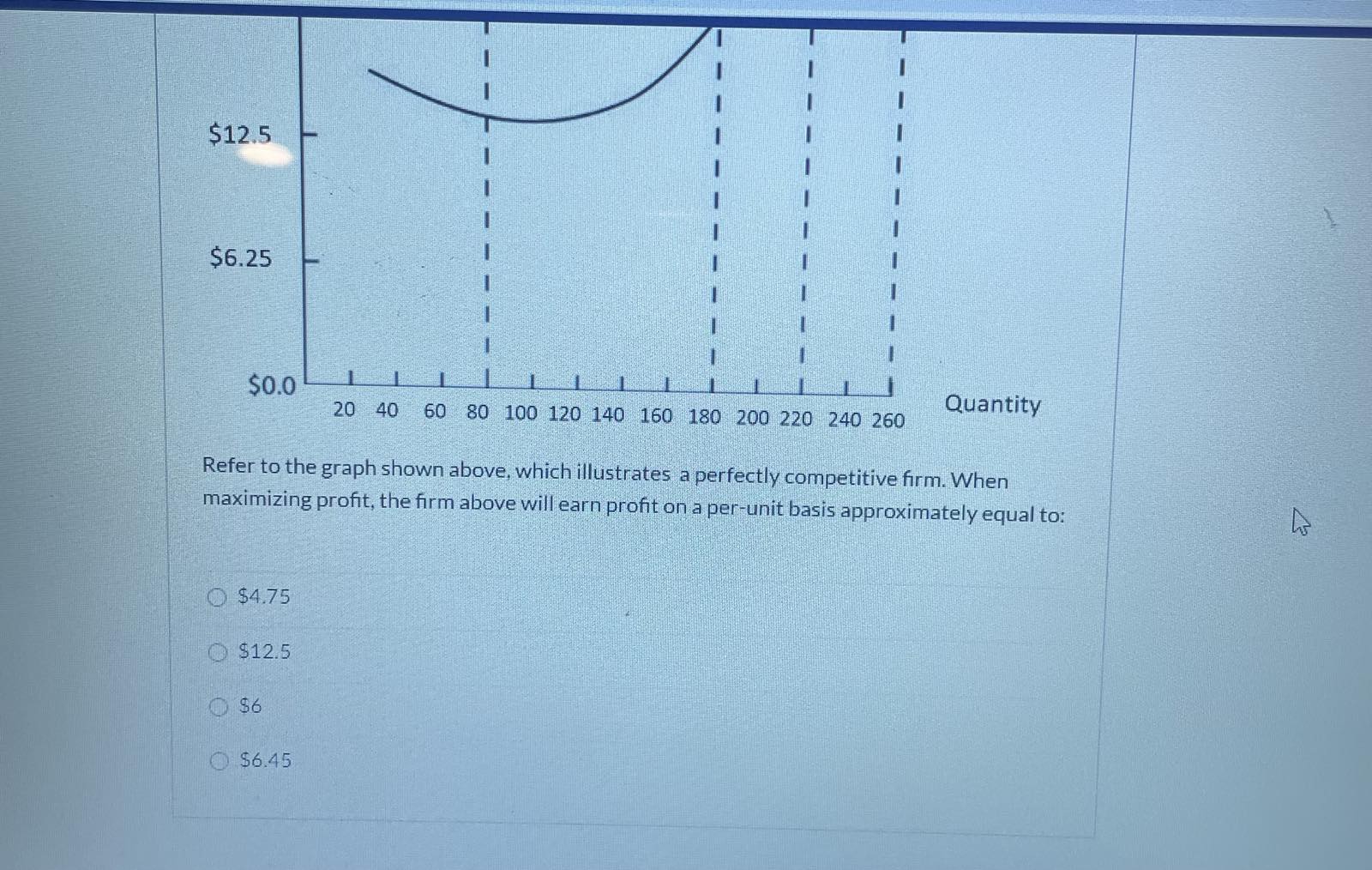

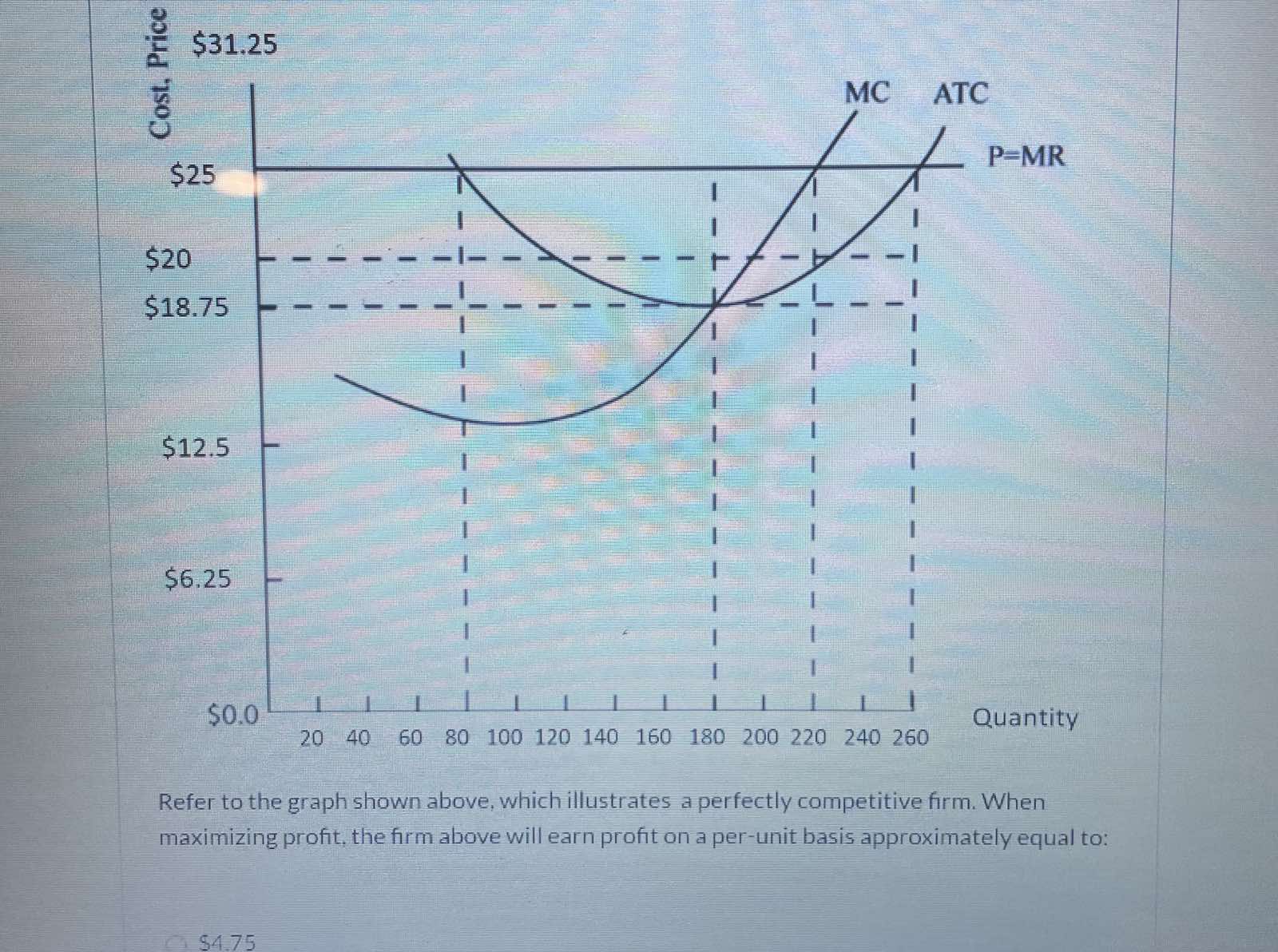

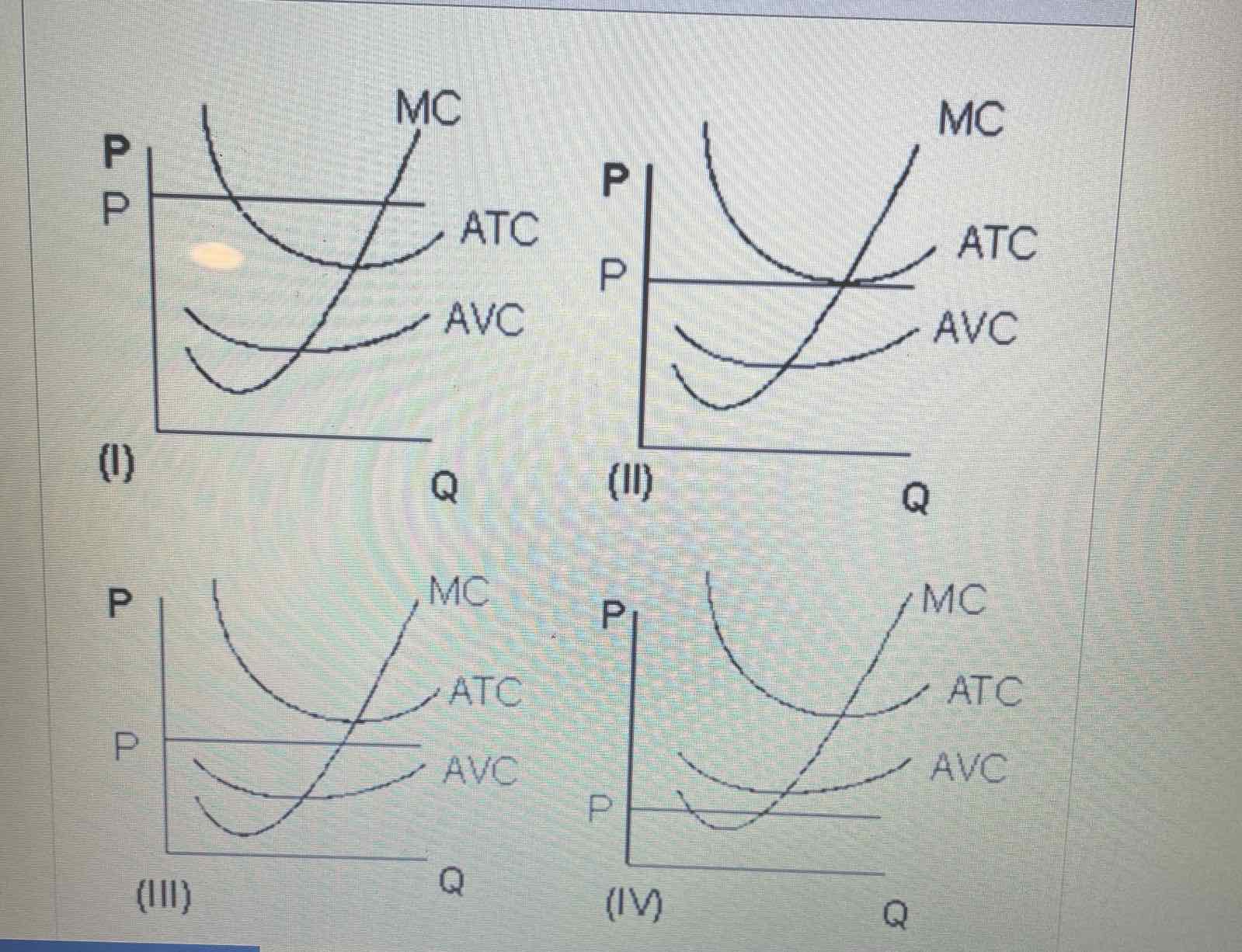

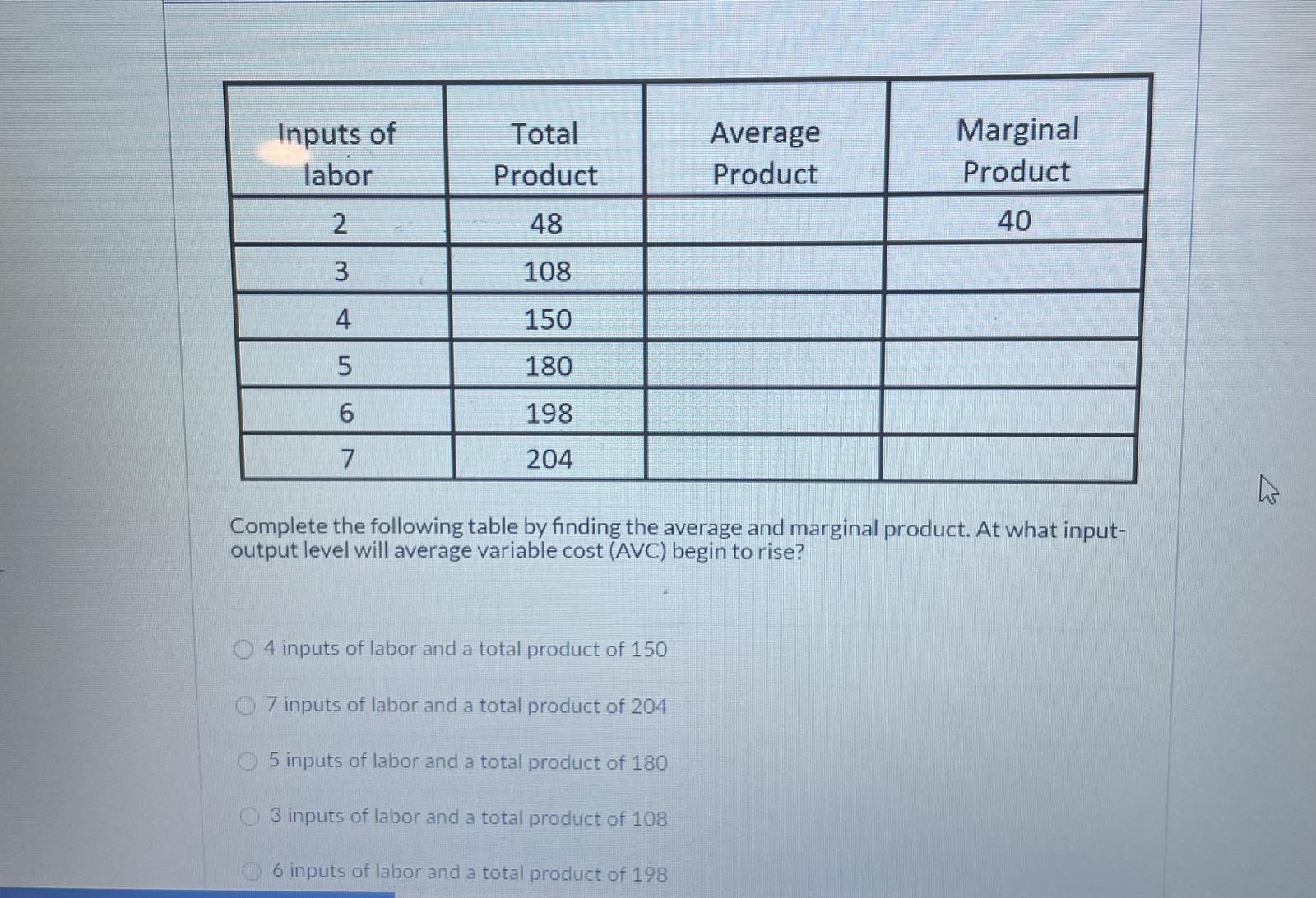

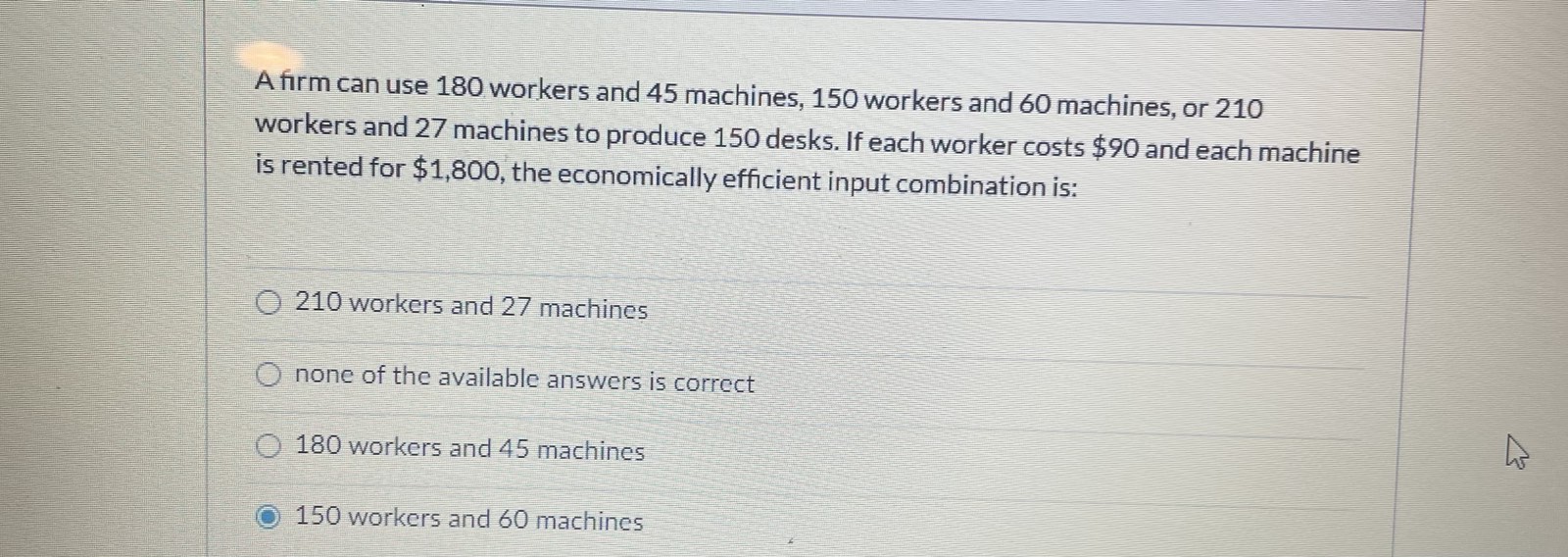

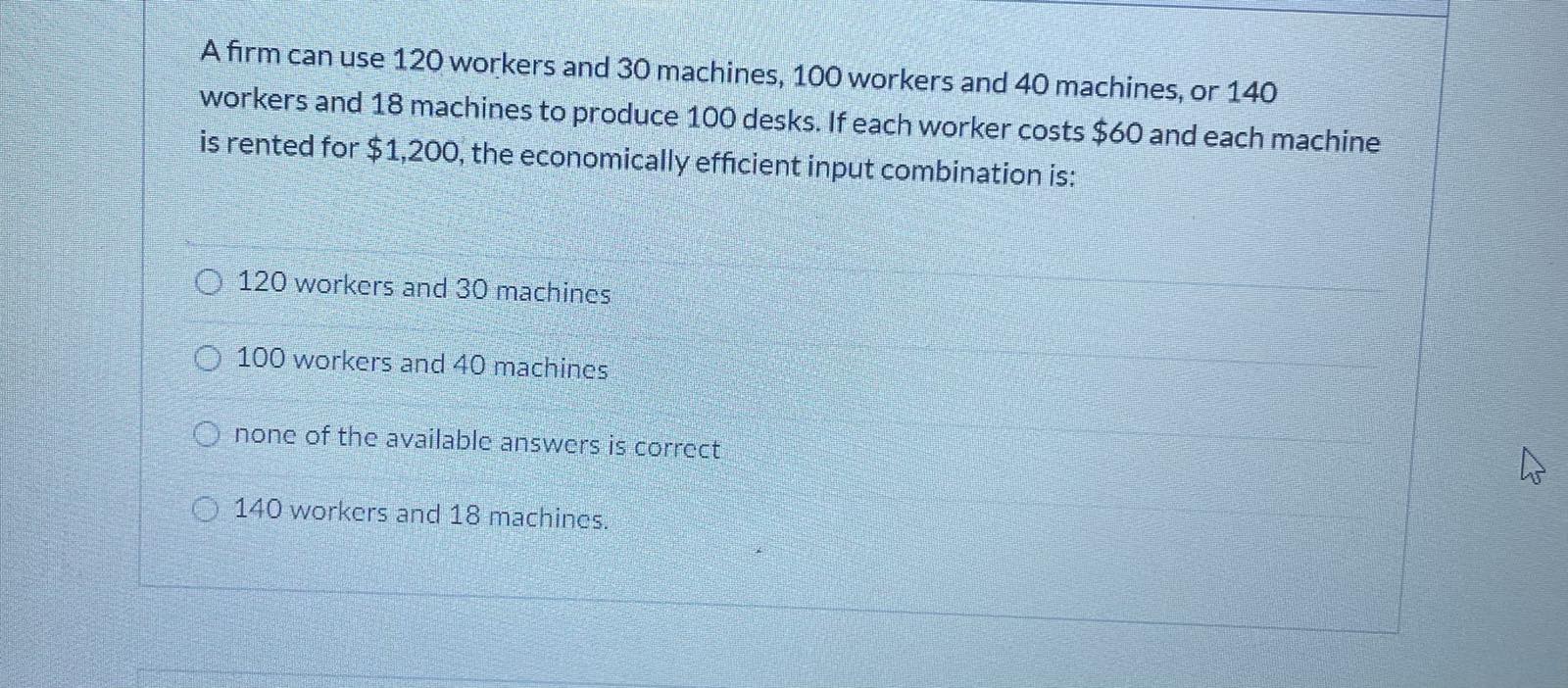

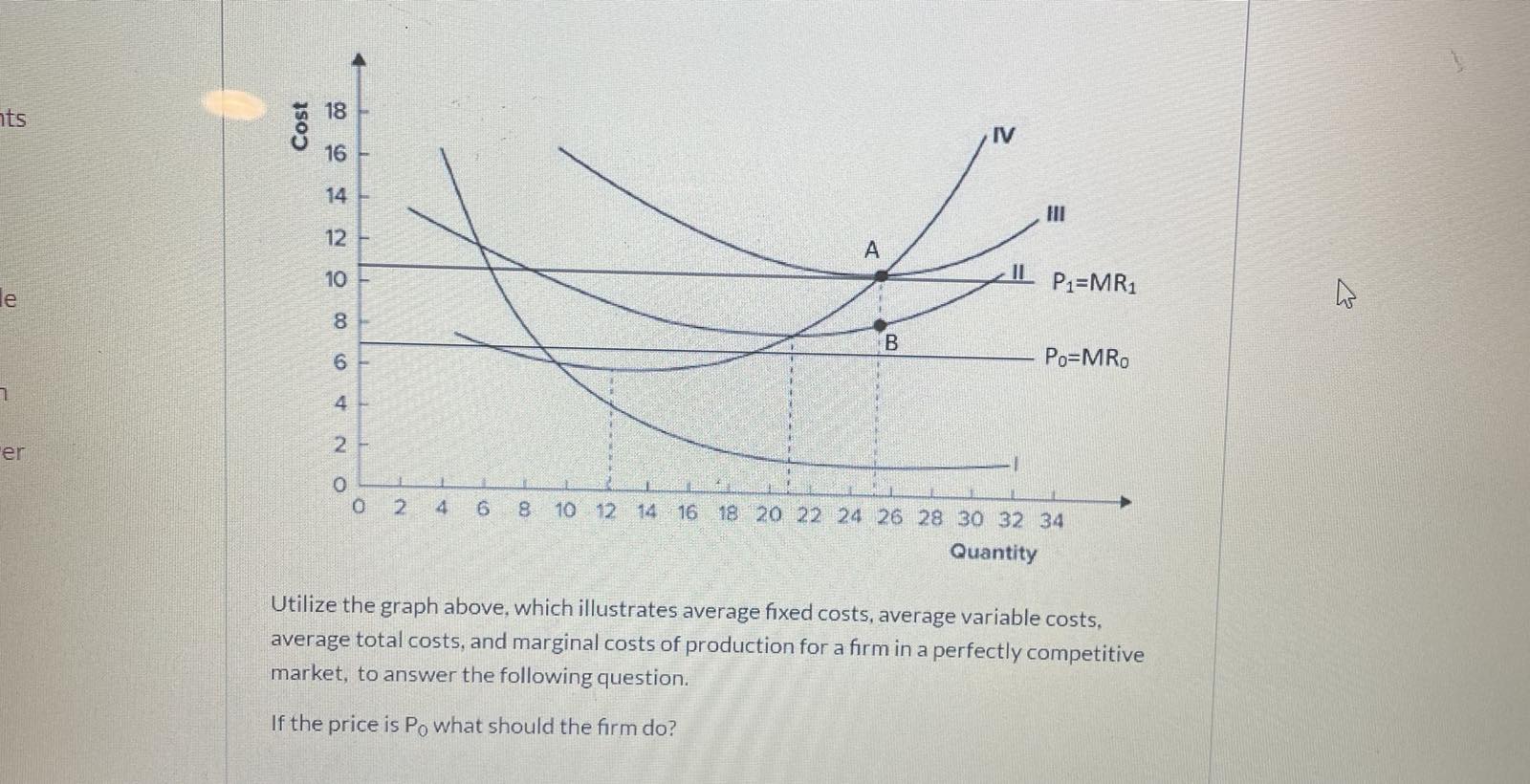

The minimum possible average total cost of producing generic antidepressant medication in the long run is $10 per bottle. Suppose in this perfectly competitive industry firms are receiving a price of $20 per bottle for their product in the short run and there are constant returns to scale. Other things being equal, it follows that: O the price of generic antidepressants will be between $10 and $20 in the long run O the price of generic antidepressants will be $20 in the long run O the price of generic antidepressants will be $10 in the long run O there is not enough information to give a definitive answer 5 3 ntsQuantity Total Cost Total Revenue 10 $ 25 50 20 60 100 30 105 150 40 160 200 Based on the data above, a profit-maximizing firm in a perfectly competitive market would decide to produce: O 20 units of output. 10 units of output. 40 units of output. 30 units of output.TC TR 210 180 150 Cost/revenue 100 86 48 120 250 450 525 Quantity Refer to the graph above. If this firm that is operating in a perfectly competitive market is producing 120 units of output, the market price is equal to: impossible to determine with the information given. $0.40. 2.50 $1 $48.MC ATC Price, Cous 3 33 2 AVC Q1 02 03 04 Output Refer to the graph shown above. If the market price is A, the firm operating in a perfectly competitive market will produce Q2 and incur a loss. Q4 and carn a postive economic profit. Q3 and earn a positive economic profit. Q3 and break even.MC ATC Price, Costs 2 38 2 AVC 01 02 03 04 Output Refer to the graph above. If the market price is A. the maximum profit the firm operating in a perfectly competitive market can earn is: Q3 multiplied by the difference between Pa and P2. Q4 multiplied by the difference between P4 and P3 Q4 multiplied by P4. Q3 multiplied by P3cost of producing 45 units is $135. These numbers imply that O diminishing marginal productivity is present, but this is dependent on a myriad of factors O economies of scope are present diseconomies of scale are present economies of scale are presentP1-MRI 14 4.2 -Po-MRo 800 900 1.000 10 20 24 Answer the following question based off of the graphs above, which depict a perfectly competitive industry and firm: If the industry or market is in equilibrium at point B, where will the firm choose to operate and what are the economic profits (losses) at that point? Q-24: Economic profits-$91.2 Q-20: Economic profits--$91.2 Q-900: Economic profits-$96 Q-900: Economic profits-$80Industry Firm MC ATC 18 -PI-MRI Po-MRo 800 900 1:000 10 20 24 Answer the following question based off of the graphs above, which depict a perfectly competitive industry and firm: If the industry or market is in equilibrium at point B, where will the firm choose to operate and what are the economic profits (losses) at that point?ATC 18 P.-MR Po-MRo 2.6 800 900 1.009 20 24 Answer the following question based off of the graphs above, which depict a perfectly competitive industry and firm: Suppose the industry or market is now in equilibrium at point B. What could have caused the market equilibrium to change from point A to point B? An increase in society's income, which caused the demand curve to shift to the right Firms exiting the market. This caused the price to increase in the market. A decrease in society's income, which caused the supply curve to shift to the right :1).An increase in profits. which led to an increase in supply. This caused the price in the -market to increase.7 - - $12.5 $6.25 $0.0 20 40 60 80 100 120 140 160 180 200 220 240 260 Quantity Refer to the graph shown above, which illustrates a perfectly competitive firm. When maximizing profit, the firm above will earn profit on a per-unit basis approximately equal to: $4.75 $12.5 $6 $6.45$31.25 Cost. Price MC ATC P-MR $25 $20 $18.75 $12.5 $6.25 $0.0 Quantity 20 40 60 80 100 120 140 160 180 200 220 240 260 Refer to the graph shown above, which illustrates a perfectly competitive firm. When maximizing profit, the firm above will earn profit on a per-unit basis approximately equal to:Refer to the graphs above of perfectly competitive firms. Which of the following statements is correct? In graph (IV) the firm is earning an economic loss. Therefore, firms will enter the market and compete away the negative economic profits. This is due to the fact that prices will decline from the increase in supply. In the long-run, the the firm depicted will shut down. In graph (I) the firm is enjoying positive economic profits. Therefore, firms will enter the market and compete away the positive economic profits. This is due to the fact that prices will decrease from the decrease in demand. In graph (IV) the firm is earning an economic loss. However, the firm will continue to operate in the short-run because price is greater than average variable costs. Therefore, the firm is covering average variable costs and reducing the overall burden of total fixed costs. In graph (III) the firm is enjoying positive economic profits. Therefore, firms will enter the market and compete away the positive economic profits. This is due to the fact that prices will decline from the increase in supply. In graph (II) economic profits for the firm is $0. Therefore, firms will not have an incentive to enter or exit the market. However, in the long run this firm will exit the market because of an influx of new firms in the long-run.\fInputs of Total Average Marginal labor Product Product Product 2 48 40 3 108 4 150 5 180 6 198 7 204 Complete the following table by finding the average and marginal product. At what input- output level will average variable cost (AVC) begin to rise? 4 inputs of labor and a total product of 150 7 inputs of labor and a total product of 204 5 inputs of labor and a total product of 180 3 inputs of labor and a total product of 108 6 inputs of labor and a total product of 198A firm can use 180 workers and 45 machines, 150 workers and 60 machines, or 210 workers and 27 machines to produce 150 desks. If each worker costs $90 and each machine is rented for $1,800, the economically efficient input combination is: 210 workers and 27 machines O none of the available answers is correct 180 workers and 45 machines O 150 workers and 60 machinesA firm can use 120 workers and 30 machines, 100 workers and 40 machines, or 140 workers and 18 machines to produce 100 desks. If each worker costs $60 and each machine is rented for $1,200, the economically efficient input combination is: 120 workers and 30 machines 100 workers and 40 machines Onone of the available answers is correct 140 workers and 18 machines.20 22 24 26 28 30 32 34 Quantity Utilize the graph above, which illustrates average fixed costs, average variable costs, average total costs, and marginal costs of production for a firm in a perfectly competitive market, to answer the following question. If the price is Po what should the firm do? O The firm should increase production because marginal cost is less than marginal revenue. Therefore, the firm has not maximized operating economic profits. O The firm should shut down in the short-run because price is below AVC. In the long-run, they will assess the market conditions to see whether they should reopen for business or exit the market. The firm should decrease production because marginal revenue is greater than marginal cost. Therefore, the firm has not maximized operating profits. The firm should exit the market because firms will soon enter. This will drive the price below ATC, which will cause the firm to earn economic losses. The firm should shut down in the long-run because price is below AVC. In the long-run, they will assess the market conditions to see whether they should reopen for business or exit the market. They will reopen if price remains below AVC.18 its Cost IV A P1=MR1 le ON DOO ONTO B Po=MRo er 0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 Quantity Utilize the graph above, which illustrates average fixed costs, average variable costs, average total costs, and marginal costs of production for a firm in a perfectly competitive market, to answer the following question. If the price is Po what should the firm do

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts