Question: answer : b The following information is used for the next SIX questions Fedsmoker Protocols is a firm that is headquartered in France. Resulting from

answer : b

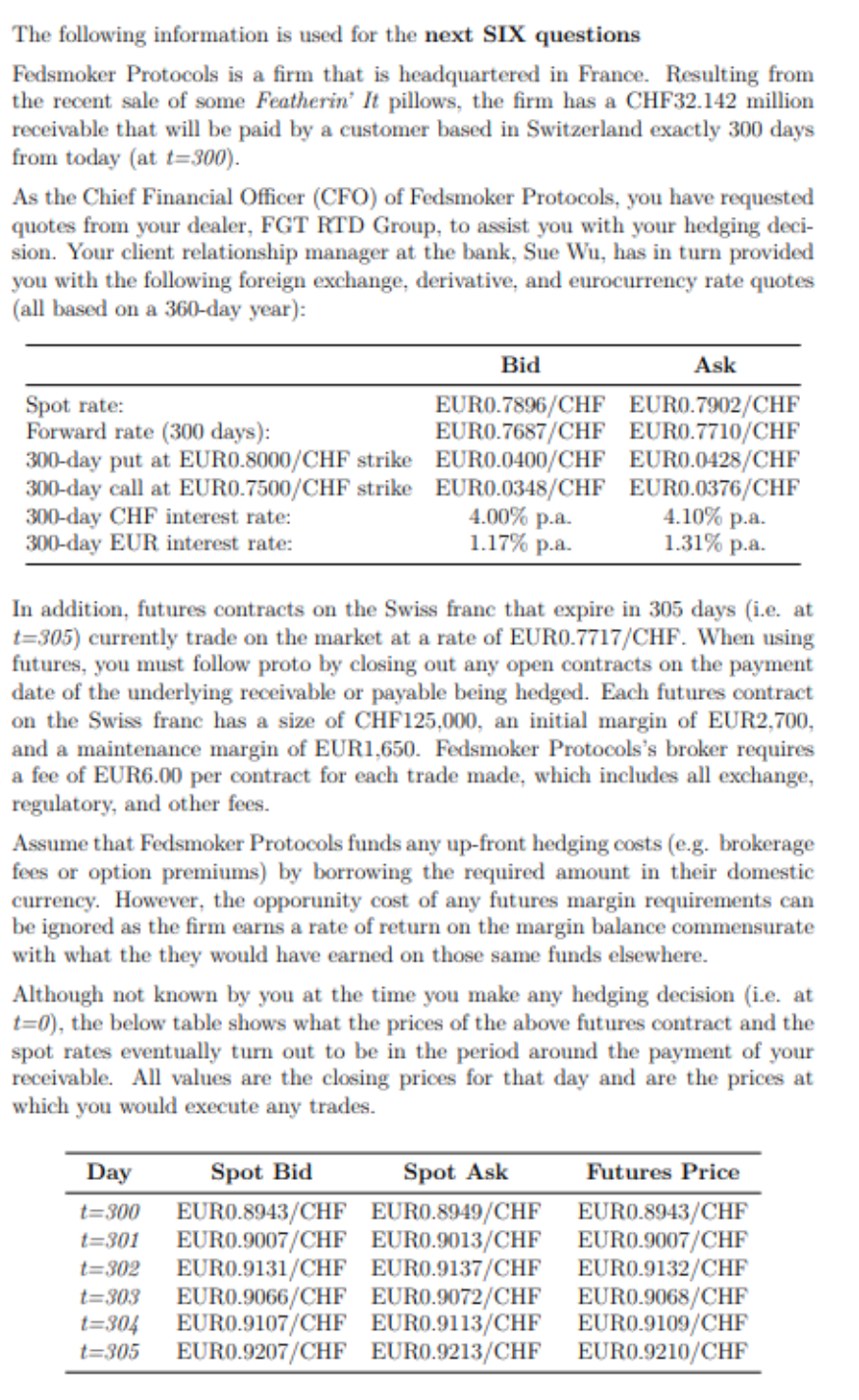

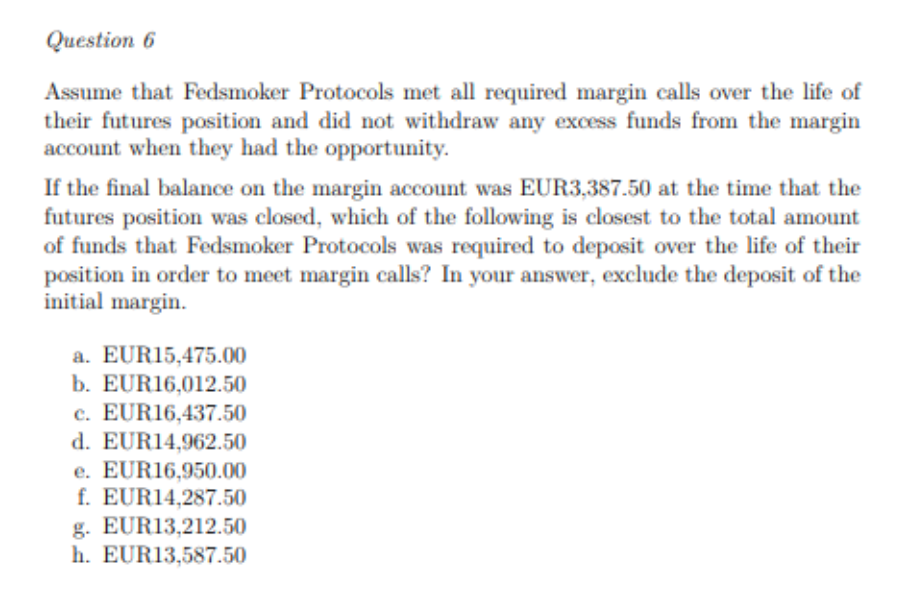

The following information is used for the next SIX questions Fedsmoker Protocols is a firm that is headquartered in France. Resulting from the recent sale of some Featherin' It pillows, the firm has a CHF32.142 million receivable that will be paid by a customer based in Switzerland exactly 300 days from today (at t=300). As the Chief Financial Officer (CFO) of Fedsmoker Protocols, you have requested quotes from your dealer, FGT RTD Group, to assist you with your hedging deci- sion. Your client relationship manager at the bank, Sue Wu, has in turn provided you with the following foreign exchange, derivative, and eurocurrency rate quotes (all based on a 360-day year): Bid Ask Spot rate: EUR0.7896/CHF EURO.7902/CHF Forward rate (300 days): EUR0.7687/CHF EURO.7710/CHF 300-day put at EUR0.8000/CHF strike EUR0.0400/CHF EURO.0428/CHF 300-day call at EURO.7500/CHF strike EUR0.0348/CHF EURO.0376/CHF 300-day CHF interest rate: 4.00% p.a. 4.10% p.a. 300-day EUR interest rate: 1.17% p.a. 1.31% p.a. In addition, futures contracts on the Swiss franc that expire in 305 days (i.e. at t=305) currently trade on the market at a rate of EUR0.7717/CHF. When using futures, you must follow proto by closing out any open contracts on the payment date of the underlying receivable or payable being hedged. Each futures contract on the Swiss franc has a size of CHF125,000, an initial margin of EUR2,700, and a maintenance margin of EUR1.650. Fedsmoker Protocols's broker requires a fee of EUR6.00 per contract for each trade made, which includes all exchange, regulatory, and other fees. Assume that Fedsmoker Protocols funds any up-front hedging costs (e.g. brokerage fees or option premiums) by borrowing the required amount in their domestic currency. However, the opporunity cost of any futures margin requirements can be ignored as the firm earns a rate of return on the margin balance commensurate with what the they would have earned on those same funds elsewhere. Although not known by you at the time you make any hedging decision (i.e. at t=0), the below table shows what the prices of the above futures contract and the spot rates eventually turn out to be in the period around the payment of your receivable. All values are the closing prices for that day and are the prices at which you would execute any trades. Day t=300 t=301 t=302 t=303 t=304 t=305 Spot Bid Spot Ask EURO.8943/CHF EUR0.8949/CHF EUR0.9007/CHF EUR0.9013/CHF EUR0.9131/CHF EUR0.9137/CHF EUR0.9066/CHF EUR0.9072/CHF EUR0.9107/CHF EUR0.9113/CHF EUR0.9207/CHF EUR0.9213/CHF Futures Price EUR0.8943/CHF EUR0.9007/CHF EUR0.9132/CHF EUR0.9068/CHF EUR0.9109/CHF EUR0.9210/CHF Question 6 Assume that Fedsmoker Protocols met all required margin calls over the life of their futures position and did not withdraw any excess funds from the margin account when they had the opportunity. If the final balance on the margin account was EUR3,387.50 at the time that the futures position was closed, which of the following is closest to the total amount of funds that Fedsmoker Protocols was required to deposit over the life of their position in order to meet margin calls? In your answer, exclude the deposit of the initial margin. a. EUR 15.475.00 b. EUR16,012.50 c. EUR16,437.50 d. EUR14,962.50 e. EUR16,950.00 f. EUR14,287.50 g. EUR13,212.50 h. EUR13,587.50 The following information is used for the next SIX questions Fedsmoker Protocols is a firm that is headquartered in France. Resulting from the recent sale of some Featherin' It pillows, the firm has a CHF32.142 million receivable that will be paid by a customer based in Switzerland exactly 300 days from today (at t=300). As the Chief Financial Officer (CFO) of Fedsmoker Protocols, you have requested quotes from your dealer, FGT RTD Group, to assist you with your hedging deci- sion. Your client relationship manager at the bank, Sue Wu, has in turn provided you with the following foreign exchange, derivative, and eurocurrency rate quotes (all based on a 360-day year): Bid Ask Spot rate: EUR0.7896/CHF EURO.7902/CHF Forward rate (300 days): EUR0.7687/CHF EURO.7710/CHF 300-day put at EUR0.8000/CHF strike EUR0.0400/CHF EURO.0428/CHF 300-day call at EURO.7500/CHF strike EUR0.0348/CHF EURO.0376/CHF 300-day CHF interest rate: 4.00% p.a. 4.10% p.a. 300-day EUR interest rate: 1.17% p.a. 1.31% p.a. In addition, futures contracts on the Swiss franc that expire in 305 days (i.e. at t=305) currently trade on the market at a rate of EUR0.7717/CHF. When using futures, you must follow proto by closing out any open contracts on the payment date of the underlying receivable or payable being hedged. Each futures contract on the Swiss franc has a size of CHF125,000, an initial margin of EUR2,700, and a maintenance margin of EUR1.650. Fedsmoker Protocols's broker requires a fee of EUR6.00 per contract for each trade made, which includes all exchange, regulatory, and other fees. Assume that Fedsmoker Protocols funds any up-front hedging costs (e.g. brokerage fees or option premiums) by borrowing the required amount in their domestic currency. However, the opporunity cost of any futures margin requirements can be ignored as the firm earns a rate of return on the margin balance commensurate with what the they would have earned on those same funds elsewhere. Although not known by you at the time you make any hedging decision (i.e. at t=0), the below table shows what the prices of the above futures contract and the spot rates eventually turn out to be in the period around the payment of your receivable. All values are the closing prices for that day and are the prices at which you would execute any trades. Day t=300 t=301 t=302 t=303 t=304 t=305 Spot Bid Spot Ask EURO.8943/CHF EUR0.8949/CHF EUR0.9007/CHF EUR0.9013/CHF EUR0.9131/CHF EUR0.9137/CHF EUR0.9066/CHF EUR0.9072/CHF EUR0.9107/CHF EUR0.9113/CHF EUR0.9207/CHF EUR0.9213/CHF Futures Price EUR0.8943/CHF EUR0.9007/CHF EUR0.9132/CHF EUR0.9068/CHF EUR0.9109/CHF EUR0.9210/CHF Question 6 Assume that Fedsmoker Protocols met all required margin calls over the life of their futures position and did not withdraw any excess funds from the margin account when they had the opportunity. If the final balance on the margin account was EUR3,387.50 at the time that the futures position was closed, which of the following is closest to the total amount of funds that Fedsmoker Protocols was required to deposit over the life of their position in order to meet margin calls? In your answer, exclude the deposit of the initial margin. a. EUR 15.475.00 b. EUR16,012.50 c. EUR16,437.50 d. EUR14,962.50 e. EUR16,950.00 f. EUR14,287.50 g. EUR13,212.50 h. EUR13,587.50

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts