Question: answer both correctly for an upvote You are given the following information about two options, A and B, on the same stock: B Stock Price

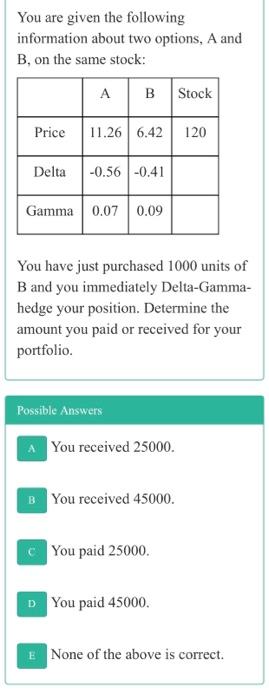

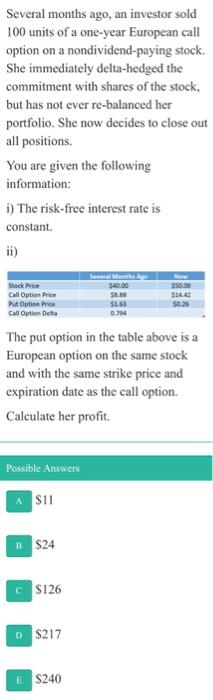

You are given the following information about two options, A and B, on the same stock: B Stock Price 11.26 6.42 120 Delta -0.56 -0.41 Gamma 0.07 0.09 You have just purchased 1000 units of B and you immediately Delta-Gamma- hedge your position. Determine the amount you paid or received for your portfolio Possible Answers You received 25000 B You received 45000. You paid 25000 D You paid 45000 E None of the above is correct. Several months ago, an investor sold 100 units of a one-year European call option on a nondividend paying stock. She immediately delta-hedged the commitment with shares of the stock, but has not ever re-balanced her portfolio. She now decides to close out all positions. You are given the following information: i) The risk-free interest rate is constant. ii) Stack Price CallOption Price P. Option Price Call Option Delta $50.00 S. 50 5163 0.74 The put option in the table above is a European option on the same stock and with the same strike price and expiration date as the call option. Calculate her profit. Possible Answers A S11 # $24

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts