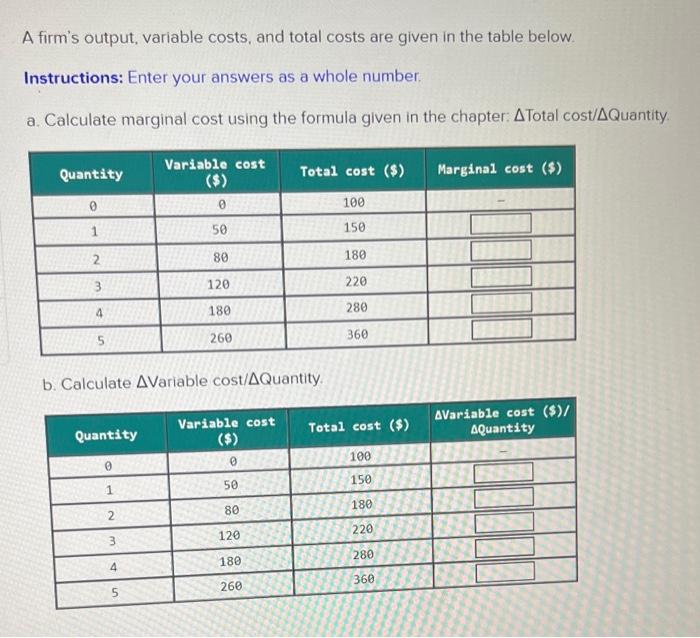

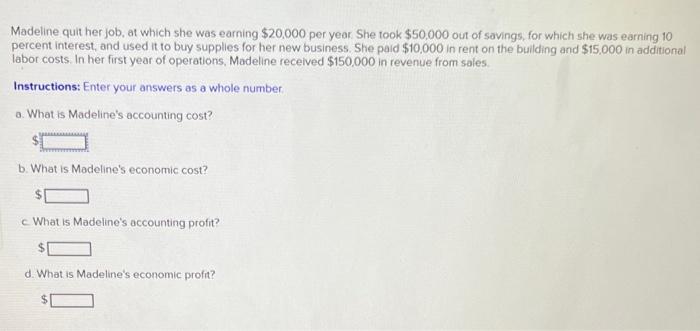

Question: Answer both questions please :) A firm's output, variable costs, and total costs are given in the table below. Instructions: Enter your answers as a

A firm's output, variable costs, and total costs are given in the table below. Instructions: Enter your answers as a whole number. a. Calculate marginal cost using the formula given in the chapter: Total cost/ Q Quntity. b. Calculate Variable cost/ Quantity. Madeline quit her job, at which she was earning $20,000 per year. She took $50,000 out of savings, for which she was earning 10 percent interest, and used it to buy supplies for her new business. She paid $10,000 in rent on the building and $15,000 in additional labor costs. In her first year of operations, Madeline received $150,000 in revenue from sales. Instructions: Enter your answers as a whole number a. What is Madeline's accounting cost? $ b. What is Madeline's economic cost? $ c. What is Madeline's accounting profit? $ d. What is Madeline's economic profit? $

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts