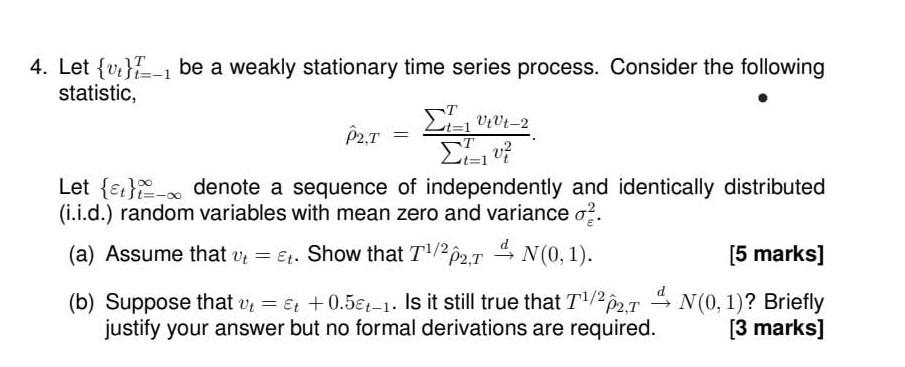

Question: answer both with explanation 4- Let {a L4 be a weakly stationary time series process. Consider the following statistic, . 2;] wt2 2:1 :2 Let

answer both with explanation

4- Let {a L4 be a weakly stationary time series process. Consider the following statistic, . 2;] \"wt2 2:1 \":2 Let {Ethics denote a sequence of independently and identically distributed {i.i.d.) random variables with mean zero and variance 3:. (a) Assume that a, = a. Show that Turf,\" it me, 1). [5 marks] PZT = (11) Suppose that o; = a, + 0.55:4. Is it still true that Til/\"pm d> MU, 1)? Briefly justify your answer but no formal derivations are required. [3 marks]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock