Question: answer c and d Problem 11-15 (Algo) You will be paying $12,000 a year in tuition expenses at the end of the next two years.

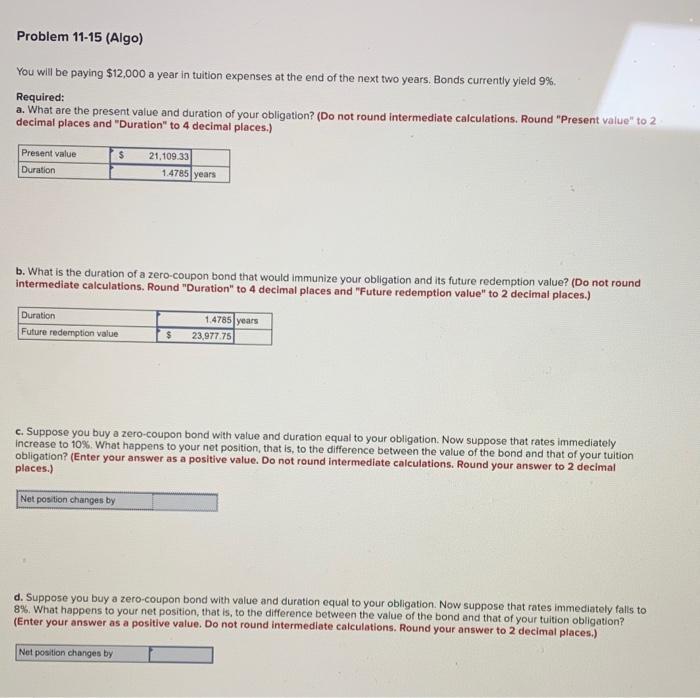

Problem 11-15 (Algo) You will be paying $12,000 a year in tuition expenses at the end of the next two years. Bonds currently yield 9% Required: a. What are the present value and duration of your obligation? (Do not round intermediate calculations. Round "Present value" to 2 decimal places and "Duration" to 4 decimal places.) Present value Duration $ 21.109.33 1.4785 years b. What is the duration of a zero-coupon bond that would immunize your obligation and its future redemption value? (Do not round intermediate calculations, Round "Duration" to 4 decimal places and "Future redemption value" to 2 decimal places.) Duration Future redemption value 1.4785 years 23,977.75 $ c. Suppose you buy a zero-coupon bond with value and duration equal to your obligation. Now suppose that rates immediately Increase to 10% What happens to your net position, that is, to the difference between the value of the bond and that of your tuition obligation? (Enter your answer as a positive value. Do not round intermediate calculations. Round your answer to 2 decimal places.) Net position changes by d. Suppose you buy a zero-coupon bond with value and duration equal to your obligation. Now suppose that rates immediately falls to 8% What happens to your net position, that is, to the difference between the value of the bond and that of your tuition obligation? (Enter your answer as a positive value. Do not round intermediate calculations. Round your answer to 2 decimal places.) Net position changes by

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts