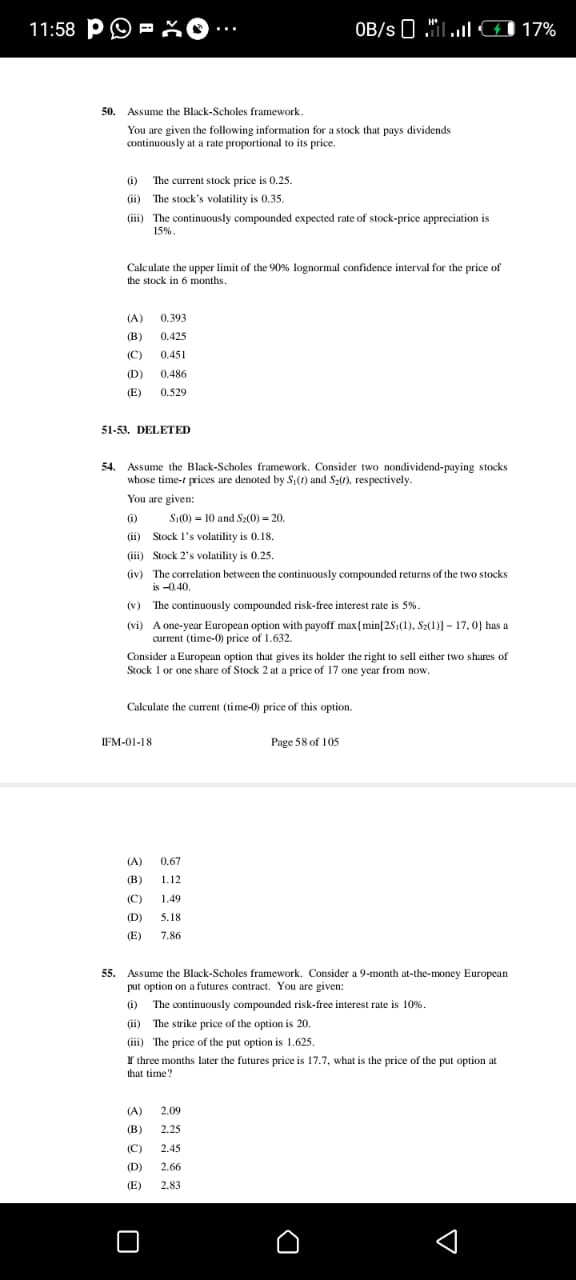

Question: Answer correctly. 11:58 P - XO ... OB/s O Mil all 1 17% 50. Assume the Black-Scholes framework. You are given the following information for

Answer correctly.

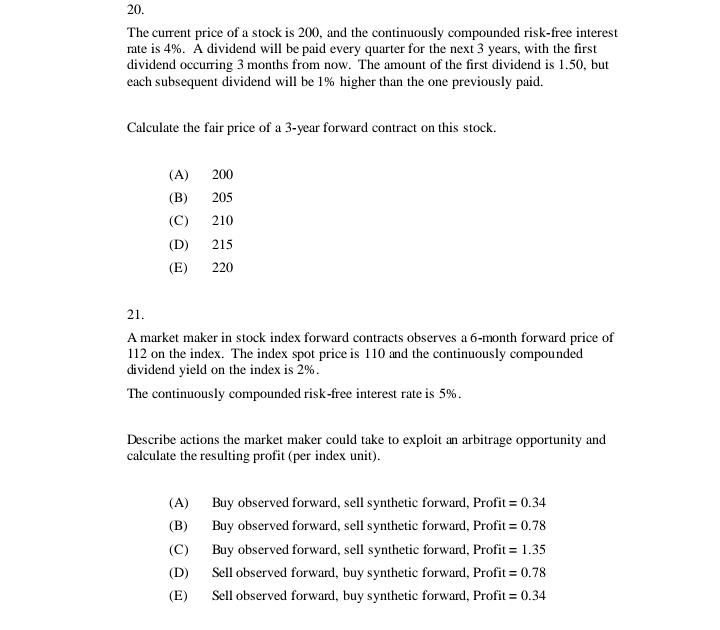

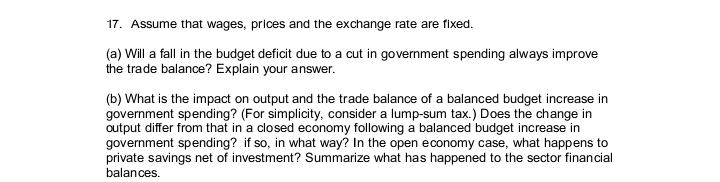

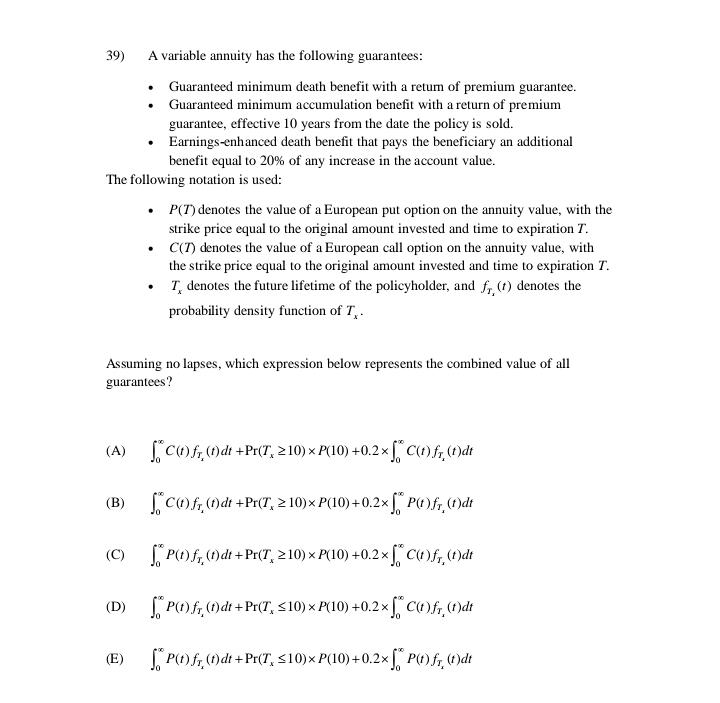

11:58 P - XO ... OB/s O Mil all 1 17% 50. Assume the Black-Scholes framework. You are given the following information for a stock that pays dividends continuously at a rate proportional to its price. () The current stock price is 0.25. (ii) The stock's volatility is 0.35. (if) The continuously compounded expected rate of stock-price appreciation is 15%. Calculate the upper limit of the 90% lognormal confidence interval for the price of the stock in 6 months. (A) 0.393 (B) 0.425 (C) 0.451 (D) 0.486 (E) 0.529 51-53, DELETED 54. Assume the Black-Scholes framework. Consider two nondividend-paying stocks whose time-/ prices are denoted by S,(t) and S_(), respectively. You are given: () S,(0) = 10 and Sz(0) = 20. (ii) Stock I's volatility is 0.18. (iii) Stock 2's volatility is 0.25. (iv) The correlation between the continuously compounded returns of the two stocks is -0.40. (v) The continuously compounded risk-free interest rate is 5%. (vi) A one-year European option with payoff max ( min[25,(1). Sz(1)] - 17. 0) has a current (time-0) price of 1.632. Consider a European option that gives its holder the right to sell either two shares of Stock I or one share of Stock 2 at a price of 17 one year from now. Calculate the current (time-0) price of this option. IFM-01-18 Page 58 of 105 (A) 0.67 (B) 1.12 (0) 1.49 (D) 5.18 (E) 7.80 55. Assume the Black-Scholes framework. Consider a 9-month at-the-money European put option on a futures contract. You are given: (i) The continuously compounded risk-free interest rate is 10%. (ii) The strike price of the option is 20. (ii) The price of the put option is 1.625. If three months later the futures price is 17.7, what is the price of the put option at that time? (A) 2.09 (B) 2.25 (C) 2.45 (D) 2.66 (E) 2.83 O17. Assume that wages, prices and the exchange rate are fixed. (a) Will a fall in the budget deficit due to a cut in government spending always improve the trade balance? Explain your answer. (b) What is the impact on output and the trade balance of a balanced budget increase in government spending? (For simplicity, consider a lump-sum tax.) Does the change in output differ from that in a closed economy following a balanced budget increase in government spending? if so, in what way? In the open economy case, what happens to private savings net of investment? Summarize what has happened to the sector financial balances.18. Use the Mundell-Fleming model and assume perfect capital mobility. Suppose there is a fall in the world interest rate. (a) Does this have an expansionary or contractionary impact on output in a small open economy? (b) Does the trade balance improve or deteriorate? Explain your answer. Look at both fixed and flexible exchange rate regimes.39) A variable annuity has the following guarantees: Guaranteed minimum death benefit with a return of premium guarantee. Guaranteed minimum accumulation benefit with a return of premium guarantee, effective 10 years from the date the policy is sold. Earnings-enhanced death benefit that pays the beneficiary an additional benefit equal to 20% of any increase in the account value. The following notation is used: . P(7) denotes the value of a European put option on the annuity value, with the strike price equal to the original amount invested and time to expiration I. C(7) denotes the value of a European call option on the annuity value, with the strike price equal to the original amount invested and time to expiration T. T, denotes the future lifetime of the policyholder, and f, (f) denotes the probability density function of T, - Assuming no lapses, which expression below represents the combined value of all guarantees? (A) [CQ)fr, (ndi +Pr(T, 210) x P(10) +0.2x [. C(1)fr, (1)dt (B) [C()fi, (Ddt +Pr(T, 2 10)x P(10)+0.2x [, P(1)fr, (1)dt (9 [" P(of,, (Ddi + PR(T, 210) * P(10) +0.2x[ Cu)fr, (1 )dt (D) [. P(1)fi, (ndi + Pr(T, 510) x P(10) +0.2x [, C()fr, (1)dt (E) [ P(D)f, (Ddi + Pr(T, 510)* P(10)+0.2x[" P()fr, (1)dt11. Stock XYZ has the following characteristics: The current price is 40. . The price of a 35-strike 1-year European call option is 9.12. . The price of a 40-strike 1-year European call option is 6.22. The price of a 45-strike 1-year European call option is 4.08. The annual effective risk-free interest rate is 8%. Let S be the price of the stock one year from now. All call positions being compared are long. Determine the range for S such that the 45-strike call produce a higher profit than the 40- strike call, but a lower profit than the 35-strike call. (A) S 42.31 (E) The range is empty. 12. Consider a European put option on a stock index without dividends, with 6 months to expiration and a strike price of 1,000. Suppose that the effective six-month interest rate is 2%, and that the put costs 74.20 today. Calculate the price that the index must be in 6 months so that being long in the put would produce the same profit as being short in the put. (A) 922.83 (B) 924.32 (C) 1,000.00 (D) 1,075.68 (E) 1,077.17 IFM-01-18 Page 8 of 105 13 A trader shorts one share of a stock index for 50 and buys a 60-strike European call option on that stock that expires in 2 years for 10. Assume the annual effective risk-free interest rate is 3%. The stock index increases to 75 after 2 years. Calculate the profit on your combined position, and determine an alternative name for this combined position. Profit Name (A) -22.64 Floor (B) -17.56 Floor (C) -22.64 Cap (D) -17.56 Cap (E) -22.64 "Written" Covered Call20. The current price of a stock is 200, and the continuously compounded risk-free interest rate is 4%. A dividend will be paid every quarter for the next 3 years, with the first dividend occurring 3 months from now. The amount of the first dividend is 1.50, but each subsequent dividend will be 1% higher than the one previously paid. Calculate the fair price of a 3-year forward contract on this stock. (A) 200 (B) 205 (C) 210 (D) 215 (E) 220 21. A market maker in stock index forward contracts observes a 6-month forward price of 112 on the index. The index spot price is 110 and the continuously compounded dividend yield on the index is 2%. The continuously compounded risk-free interest rate is 5%. Describe actions the market maker could take to exploit an arbitrage opportunity and calculate the resulting profit (per index unit). (A) Buy observed forward, sell synthetic forward, Profit = 0.34 (B) Buy observed forward, sell synthetic forward, Profit = 0.78 (C) Buy observed forward, sell synthetic forward, Profit = 1.35 (D) Sell observed forward, buy synthetic forward, Profit = 0.78 (E) Sell observed forward, buy synthetic forward, Profit = 0.344. Set up the new budget constraint (assuming the agents never receive the money paid to the government and the money is used to finance things for which individuals have no utility). Derive the first order conditions and provide the analogous two conditions for the marginal rates of substitutions (for ci vs ez and for c vs L). Explain the intuition of both equations. Is the MRS distorted? (i.e. are they different than they would be in the absence of taxation?) Why or why not

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts