Question: answer E-G please 5. The following table gives the current balance sheet for Travellers Inn Inc. (TIT), a company that was formed by merging a

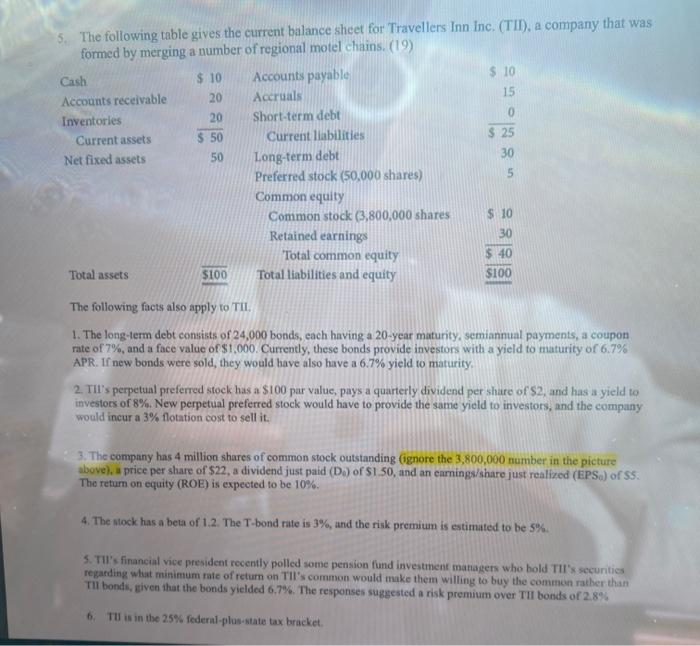

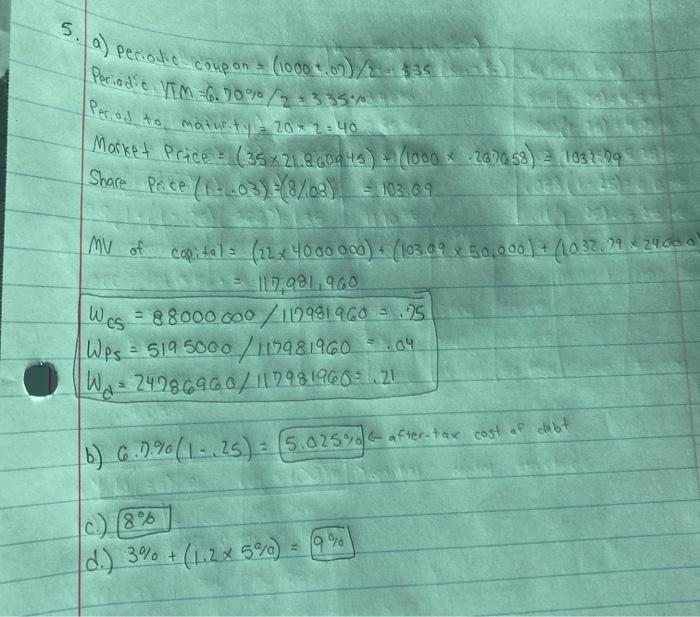

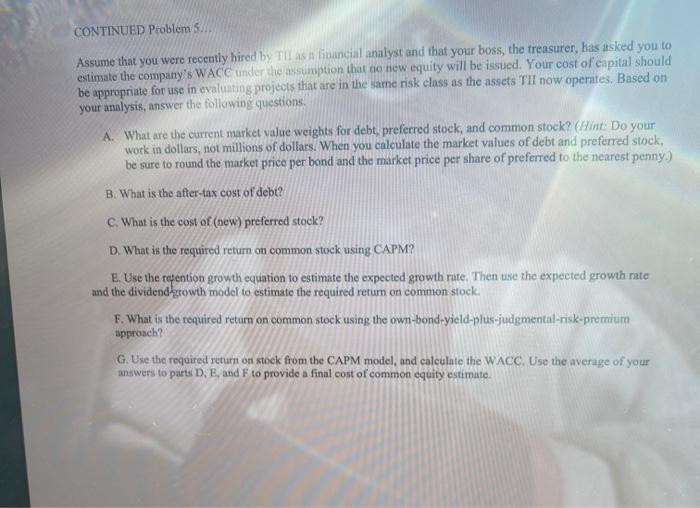

5. The following table gives the current balance sheet for Travellers Inn Inc. (TIT), a company that was formed by merging a number of regional motel chains. (19) Cash $ 10 Accounts payable $ 10 Accounts receivable 20 15 Accruals Inventories 20 0 Short-term debt Current assets $50 Current liabilities $ 25 Net fixed assets 50 Long-term debt 30 Preferred stock (50,000 shares) Common equity Common stock (3,800,000 shares $ 10 Retained earnings 30 Total common equity $ 40 Total assets $100 Total liabilities and equity $100 The following facts also apply to TIL. 5 1. The long-term debt consists of 24,000 bonds, each having a 20-year maturity, semiannual payments, a coupon rate of 7%, and a face value of $1,000. Currently, these bonds provide investors with a yield to maturity of 6.7% APR. If new bonds were sold, they would have also have a 6.7% yield to maturity, 2. Til's perpetual preferred stock has a $100 par value, pays a quarterly dividend per share of 'S2, and has a yield to investors of 8% New perpetual preferred stock would have to provide the same yield to investors, and the company would incur a 3% flotation cost to sell it. 3. The company has 4 million shares of common stock outstanding (ignore the 3,800,000 number in the picture above), a price per share of $22, a dividend just paid (D) of S150, and an earnings/share just realized (EPS) of SS. The return on equity (ROE) is expected to be 10% 4. The mock has a beta of 1.2. The T-bond rate is 3%, and the risk premium is estimated to be 5% 5. Tul's financial vice president recently polled some pension fund investment managers who hold Til's securities regarding what minimum rate of return on Til's common would make them willing to buy the common rather than Tul bonds, given that the bonds yielded 6,7%. The responses suggested a risk premium over Til bonds of 2.8% 6. THI is in the 25% federal-plus-state tax bracket. 5. (a) periodic coupon = (1000 1,022 $35. Market Price (35X21.8 GD945) (1000 x 20)658) 3.1032.99 YEM 20* 1.40 Periodic TM-6. 107/223357 Period to maturity Share Price 12.03) = 8/68) = 103.69 capitals (22x 40 00 000) + (103.09 x 50,000) + (1032.24 24 06 0 117,981.960 Wes - 88000 000/119981960 3.75 Wps = 5195000 / 119981960 - 104 Wo= 24986900/119981960321 (6) 6.D.% (1.,25) = (5.025%06 after-tax cost of debt 19% d.) 3% + (1.2% 5%) CONTINUED Problem 5. Assume that you were recently hired by the financial analyst and that your boss, the treasurer, has asked you to estimate the company's WACC under the assumption that no new equity will be issued. Your cost of capital should be appropriate for use in evaluating projects that are in the same risk class as the assets TII now operates. Based on your analysis, answer the following questions A. What are the current market value weights for debt, preferred stock, and common stock? (Hint: Do your work in dollars, not millions of dollars. When you calculate the market values of debt and preferred stock, be sure to round the market price per bond and the market price per share of preferred to the nearest penny.) B. What is the after-tax cost of debt? C. What is the cost of (new) preferred stock? D. What is the required return on common stock using CAPM? E. Use the rention growth equation to estimate the expected growth rate. Then use the expected growth rato and the dividend growth model to estimate the required return on common stock. F. What is the required return on common stock using the own-bond-yield-plus-judgmental-risk-premium approach G. Use the required return on stock from the CAPM model, and calculate the WACC. Use the average of your answers to parts D, E, and F to provide a final cost of common equity estimate 5. The following table gives the current balance sheet for Travellers Inn Inc. (TIT), a company that was formed by merging a number of regional motel chains. (19) Cash $ 10 Accounts payable $ 10 Accounts receivable 20 15 Accruals Inventories 20 0 Short-term debt Current assets $50 Current liabilities $ 25 Net fixed assets 50 Long-term debt 30 Preferred stock (50,000 shares) Common equity Common stock (3,800,000 shares $ 10 Retained earnings 30 Total common equity $ 40 Total assets $100 Total liabilities and equity $100 The following facts also apply to TIL. 5 1. The long-term debt consists of 24,000 bonds, each having a 20-year maturity, semiannual payments, a coupon rate of 7%, and a face value of $1,000. Currently, these bonds provide investors with a yield to maturity of 6.7% APR. If new bonds were sold, they would have also have a 6.7% yield to maturity, 2. Til's perpetual preferred stock has a $100 par value, pays a quarterly dividend per share of 'S2, and has a yield to investors of 8% New perpetual preferred stock would have to provide the same yield to investors, and the company would incur a 3% flotation cost to sell it. 3. The company has 4 million shares of common stock outstanding (ignore the 3,800,000 number in the picture above), a price per share of $22, a dividend just paid (D) of S150, and an earnings/share just realized (EPS) of SS. The return on equity (ROE) is expected to be 10% 4. The mock has a beta of 1.2. The T-bond rate is 3%, and the risk premium is estimated to be 5% 5. Tul's financial vice president recently polled some pension fund investment managers who hold Til's securities regarding what minimum rate of return on Til's common would make them willing to buy the common rather than Tul bonds, given that the bonds yielded 6,7%. The responses suggested a risk premium over Til bonds of 2.8% 6. THI is in the 25% federal-plus-state tax bracket. 5. (a) periodic coupon = (1000 1,022 $35. Market Price (35X21.8 GD945) (1000 x 20)658) 3.1032.99 YEM 20* 1.40 Periodic TM-6. 107/223357 Period to maturity Share Price 12.03) = 8/68) = 103.69 capitals (22x 40 00 000) + (103.09 x 50,000) + (1032.24 24 06 0 117,981.960 Wes - 88000 000/119981960 3.75 Wps = 5195000 / 119981960 - 104 Wo= 24986900/119981960321 (6) 6.D.% (1.,25) = (5.025%06 after-tax cost of debt 19% d.) 3% + (1.2% 5%) CONTINUED Problem 5. Assume that you were recently hired by the financial analyst and that your boss, the treasurer, has asked you to estimate the company's WACC under the assumption that no new equity will be issued. Your cost of capital should be appropriate for use in evaluating projects that are in the same risk class as the assets TII now operates. Based on your analysis, answer the following questions A. What are the current market value weights for debt, preferred stock, and common stock? (Hint: Do your work in dollars, not millions of dollars. When you calculate the market values of debt and preferred stock, be sure to round the market price per bond and the market price per share of preferred to the nearest penny.) B. What is the after-tax cost of debt? C. What is the cost of (new) preferred stock? D. What is the required return on common stock using CAPM? E. Use the rention growth equation to estimate the expected growth rate. Then use the expected growth rato and the dividend growth model to estimate the required return on common stock. F. What is the required return on common stock using the own-bond-yield-plus-judgmental-risk-premium approach G. Use the required return on stock from the CAPM model, and calculate the WACC. Use the average of your answers to parts D, E, and F to provide a final cost of common equity estimate

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts