Answer more widely questions 2 and 6 from the case.

2. Which expatriate compensation elements at Bosch Group were already based on cost reduction considerations listed in the case study? Please suggest ways in which these could be improved further.

6. Do you believe that alternative assignments can substitute for traditional expatriate assignments in the long run? Please discuss major opportunities and barriers.

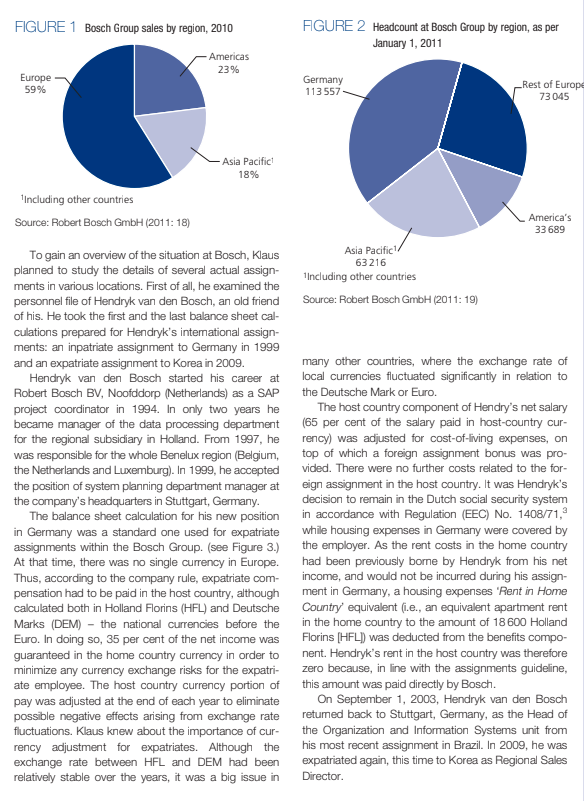

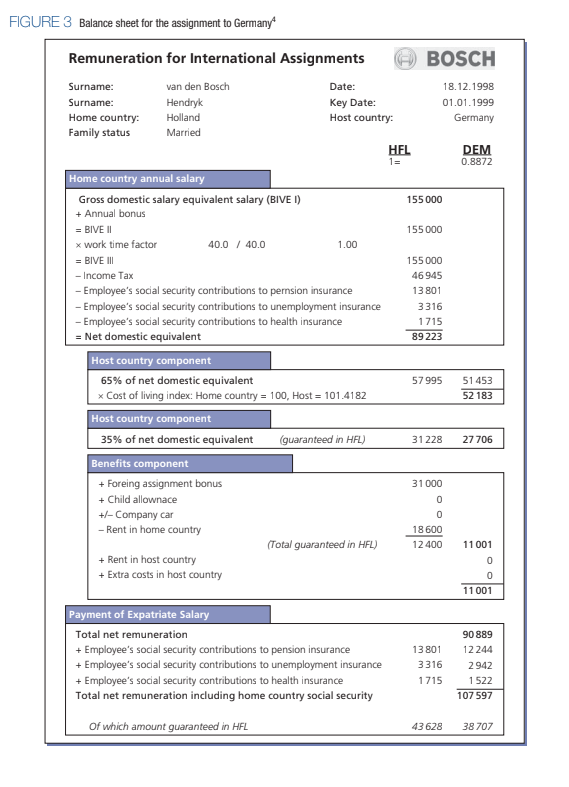

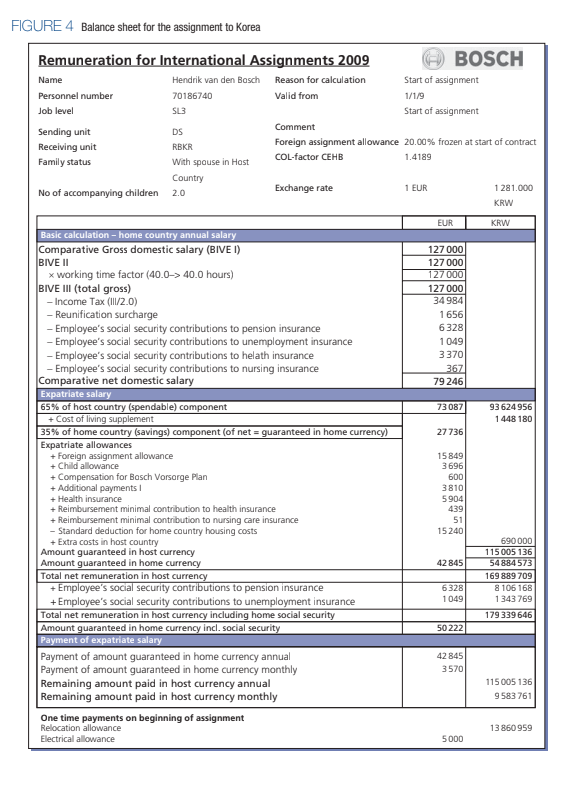

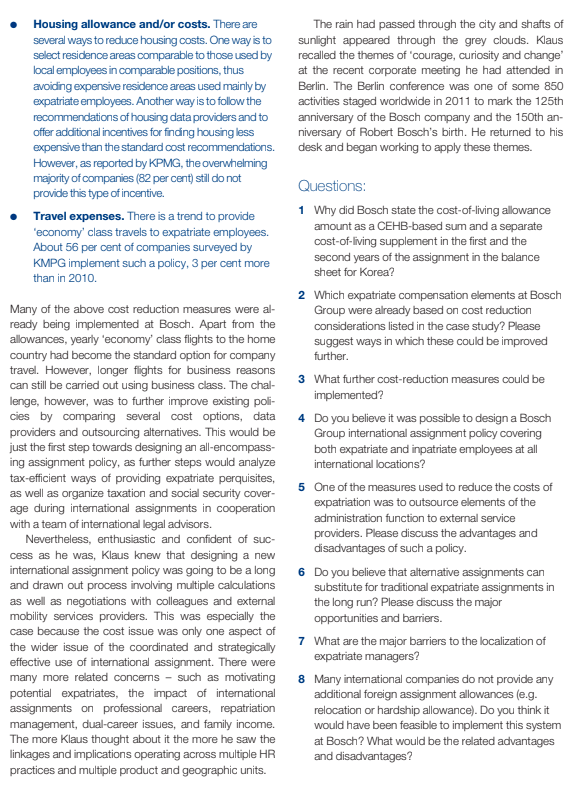

EXPATRIATE COMPENSATION AT ROBERT BOSCH GMBH: COPING WITH MODERN MOBILITY CHALLENGES By Ihar Sahakiants, Marion Festing, Manfred Froehlecke ' would rather lose money than trust.' Robert Bosch It was raining in Stuttgart. The new task which Klaus January 18. New presence in Southeast Asia: Meier, an employee of Robert Bosch GmbH's German Bosch Communication Center opens branch in headquarters' central International Assignments the Philippine capital Manila; department, received last week from his direct super- visor Michael Stein was simultaneously interesting and May 13. Bosch steps up its activities in Southeast extremely challenging: a new international assignment Asia: new headquarters opened in Singapore; policy had to be designed for the whole Bosch Group. July 5. Indian software subsidiary expands its The importance of a new international assign operations: Robert Bosch Engineering and ment policy is hard to overestimate. First it may be Business Solutions opens location in Vietnam; useful to take a look at some statistics for 2010 from September 13. Market entry in China. Bosch the latest annual report of the Bosch Group. The delivers 40 000 start-stop systems to the report, citing 2010 as 'a year of historic recovery' after automaker ChangAn; recession on a historic scale', highlighted that Bosch Group sales had skyrocketed by about 24 per cent October 11. Bosch builds new plant in India: to 47.3 billion euros. About 41 per cent of the Packaging Technology invests four million euros company's total sales were made outside Europe. in a facility near Goa; SB LiMotive opens a new (see Figure 1.) production plant in Ulsan, Korea, lithium-ion Out of 283 597 worldwide employees, 169950 - or battery cells for hybrid and electric vehicles will be about 60 per cent of the total headcount - were manufactured; located outside Germany, the home country of the November 16. New proving ground in Japan: in corporation. Moreover, 34.18 per cent of these per the north of Hokkaido, an extended proving sonnel were located outside Europe. (see Figure 2.) ground has been inaugurated - twice as big as the Statistics on the importance of international opera predecessor tions for Robert Bosch were indeed impressive, but (Robert Bosch GmbH, 2011:12-13) the figures on international mobility within the Bosch Group were even more so. In 2010, there were Although a whole range of issues related to interna- approximately 2200 executives on international proj- tional mobility needed to be addressed in the new ects requiring relocation to a foreign country and last- ing over two years, while the number of inpatriates international assignment policy, Klaus wanted to start with the financial aspects of the operation. As an inter- from Asia, the Americas and Europe on assignments national mobility professional himself, he knew only in Germany over the same two-year period reached too well about the high costs of expatriation. These 400 employees. costs included not only expensive expatriate compen- Each new location and new market meant addi- sation packages, but also huge administration tional flows of expatriate and inpatriate employees expenses and the costs of expatriate failure, e.g. the within the Bosch group. Klaus opened pages 12-13 premature termination of an assignment. These total of the report, which described the highlights of 2010 costs had the potential to make long-term assign- with respect to new markets, particularly noting: ments prohibitively expensive. FIGURE 1 Bosch Group sales by region, 2010 FIGURE 2 Headcount at Bosch Group by region, as per January 1, 2011 Americas 23% Europe 59% Germany 113557 Rest of Europe 73045 Asia Pacific 18% Including other countries Source: Robert Bosch GmbH (2011:18) America's 33 689 Asia Pacific 63216 Including other countries Source: Robert Bosch GmbH (2011:19) To gain an overview of the situation at Bosch, Klaus planned to study the details of several actual assign- ments in various locations. First of all, he examined the personnel file of Hendryk van den Bosch, an old friend of his. He took the first and the last balance sheet cal- culations prepared for Hendryk's international assign- ments: an inpatriate assignment to Germany in 1999 and an expatriate assignment to Korea in 2009. Hendryk van den Bosch started his career at Robert Bosch BV, Noofddorp (Netherlands) as a SAP project coordinator in 1994. In only two years he became manager of the data processing department for the regional subsidiary in Holland. From 1997, he was responsible for the whole Benelux region (Belgium, the Netherlands and Luxemburg). In 1999, he accepted the position of system planning department manager at the company's headquarters in Stuttgart, Germany. The balance sheet calculation for his new position in Germany was a standard one used for expatriate assignments within the Bosch Group. (see Figure 3.) At that time, there was no single currency in Europe. Thus, according to the company rule, expatriate com- pensation had to be paid in the host country, although calculated both in Holland Florins (HFL) and Deutsche Marks (DEM) - the national currencies before the Euro. In doing so, 35 per cent of the net income was guaranteed in the home country currency in order to minimize any currency exchange risks for the expatri- ate employee. The host country currency portion of pay was adjusted at the end of each year to eliminate possible negative effects arising from exchange rate fluctuations. Klaus knew about the importance of cur- rency adjustment for expatriates. Although the exchange rate between HFL and DEM had been relatively stable over the years, it was a big issue in many other countries, where the exchange rate of local currencies fluctuated significantly in relation to the Deutsche Mark or Euro. The host country component of Hendry's net salary (65 per cent of the salary paid in host-country cur- rency) was adjusted for cost-of-living expenses, on top of which a foreign assignment bonus was pro- vided. There were no further costs related to the for- eign assignment in the host country. It was Hendryk's decision to remain in the Dutch social security system in accordance with Regulation (EEC) No. 1408/71, while housing expenses in Germany were covered by the employer. As the rent costs in the home country had been previously borne by Hendryk from his net income, and would not be incurred during his assign- ment in Germany, a housing expenses 'Rent in Home Country equivalent (i.e., an equivalent apartment rent in the home country to the amount of 18600 Holland Florins (HFL) was deducted from the benefits compo- nent. Hendryk's rent in the host country was therefore zero because, in line with the assignments guideline, this amount was paid directly by Bosch. On September 1, 2003, Hendryk van den Bosch retumed back to Stuttgart, Germany, as the Head of the Organization and Information Systems unit from his most recent assignment in Brazil. In 2009, he was expatriated again, this time to Korea as Regional Sales Director. FIGURE 3 Balance sheet for the assignment to Germany Remuneration for International Assignments BOSCH Surname: Surname: Home country: Family status van den Bosch Hendryk Holland Married Date: Key Date: Host country: 18.12.1998 01.01.1999 Germany HEL 1= DEM 0.8872 155 000 155 000 1.00 155 000 46 945 13801 3316 1715 89 223 Home country annual salary Gross domestic salary equivalent salary (BIVE I) + Annual bonus = BIVE 11 x work time factor 40.0 / 40.0 = BIVE II - Income Tax - Employee's social security contributions to persion insurance - Employee's social security contributions to unemployment insurance - Employee's social security contributions to health insurance = Net domestic equivalent Host country component 65% of net domestic equivalent * Cost of living index: Home country = 100, Host = 101.4182 Host country component 35% of net domestic equivalent guaranteed in HEL) Benefits component + Foreing assignment bonus + Child allownace +/- Company car - Rent in home country (Total guaranteed in HFL) + Rent in host country + Extra costs in host country 57 995 51453 52 183 31 228 27 706 31000 0 0 18 600 12400 11 001 0 0 11 001 Payment of Expatriate Salary Total net remuneration + Employee's social security contributions to pension insurance + Employee's social security contributions to unemployment insurance + Employee's social security contributions to health insurance Total net remuneration including home country social security 13 801 3316 1715 90 889 12 244 2942 1522 107 597 of which amount guaranteed in HFL 43 628 38 707 The pay calculation for his assignment to Korea was more complex. (see Figure 4.) At that point, Hendryk had two children, which meant additional expenses in the host country as well as the loss of child allowance in Germany (then 1848 Euros per child, per year). However, the latter was compensated by Robert Bosch GmbH in accordance with internal company policy, while housing expenses in the host country were again borne by the company. A couple of years prior to that, several changes were introduced in the assignment policy, triggered ini- tially by increasingly refined market data comparisons. For instance, a change of the cost-of-living data pro- vider made it possible to make a differentiated use of indices and technically sophisticated and detailed cal- culations. Although this also contributed to a reduction in assignment costs for the Bosch Group, the primary goal of these changes in the compensation policy was to offer assignment conditions in line with local market conditions. According to the new policy, the foreign assignment alowance was determined and frozen at the beginning of the assignment. As such, cost-of-living calculations were based on two indices: a more generous Standard Home Base Index and a so-called Cost Effective Home Base (CEHB) Index. The Standard Home Base Index was used in the first and second years of the assignment whereas, only starting from the third year, expatriate compensation was calculated based on the CEHB Index. The decision to use the latter index was based on the assumption that costs of living decreases during the course of an assignment. This logic was based on the notion that, over time, an expatriate employee would be expected to use less expensive shopping opportunities and to refrain from expensive imports by increasingly using cheaper local products. However, calculations for the first year were also based on the CEHB Index in order to indicate to the expatriate his future income and to make clear that using the Standard Home Base Index represented more generous support at the start of an international assignment. Therefore, the difference between CEHB-based and Standard Home Base Index-based income was compensated as a cost-of-liv- ing supplement. Furthermore, lump sum payments were used in order to facilitate cost control. Kaus knew all too well how a group discussion on ways to reduce expatriation costs might proceed. One of the proposed solutions was to use increasingly alter- native forms of international assignments, including short-term international assignments lasting up to one year, frequent flyer assignments, commuter and rota- tional assignments, global virtual teams, etc. Many of these forms became more and more popular due to the rapid development of telecommunication technologies and transport, and they were used increasingly at Bosch. Moreover, one of the explicit goals of the Bosch Group was to increase the percentage of local senior executives in its foreign locations to at least 80 per cent. However, although it was a strong cost-reducing factor, this meas- ure could not possibly hinder the rapid increase of stand- ard expatriate assignments given the importance of international markets. Thus, Klaus had to consider first and foremost a number of cost reduction opportunities related to standard expatriate assignments. Based on an analysis of multiple sources stemming from the academic literature, as well as management consulting and practitioner publications, Klaus made a list of feasible potential cost-reducing solutions. In order to form an idea of the prevalence of these meas- ures among leading international companies, he checked the latest 'Global Assignment Policies and Practices' survey by KPMG. He started his analysis with the top five positions on the list: Relocation allowance. A way to reduce costs related to the relocation allowance is to provide lump sum payments at the beginning and at the end of an assignment. According to the KPMG survey about 54 per cent of all companies, including 47 per cent of European participants, implement this policy. Only 13 per cent of respondents worldwide do not provide any relocation allowance at all. Efficient calculations of the cost-of-living allowance. There is a clear trend among multinationals to increasingly implement an 'efficient purchaser index' in their cost-of-living calculations. According to the KPMG Survey, 32 per cent of all responding companies use this index, a 10 per cent increase since 2003. Cap on allowances. Capping expatriate allowances makes it possible to reduce significantly the overall costs of foreign assignments. All allowances, including the cost- of-living, hardship or other company-specific allowances can be frozen for expatriates with an expatriate income exceeding a certain level. The KMPG survey shows that the majority of companies still do not cap the major allowances. FIGURE 4 Balance sheet for the assignment to Korea Remuneration for International Assignments 2009 BOSCH Name Hendrik van den Bosch Reason for calculation Start of assignment Personnel number 70186740 Valid from 1/1/9 Job level SL3 Start of assignment Sending unit DS Comment Receiving unit RBKR Foreign assignment allowance 20.00% frozen at start of contract Family status 1.4189 With spouse in Hast COL-factor CEHB Country No of accompanying children Exchange rate 2.0 1 EUR 1 281.000 KRW EUR KRW 127 000 127 000 127 000 127 000 34 984 1656 6 328 1049 3370 367 79 246 73087 93624956 1 448 180 27 736 Basic calculation - home country annual salary Comparative Gross domestic salary (BIVE I) BIVE 11 x working time factor (40.0-> 40.0 hours) BIVE III (total gross) - Income Tax (11/2.0) - Reunification surcharge - Employee's social security contributions to pension insurance - Employee's social security contributions to unemployment insurance - Employee's social security contributions to helath insurance - Employee's social security contributions to nursing insurance Comparative net domestic salary Expatriate salary 65% of host country (spendable) component + Cost of living supplement 35% of home country (savings) component (of net = guaranteed in home currency) Expatriate allowances + Foreign assignment allowance + Child allowance + Compensation for Bosch Vorsorge Plan + Additional payments + Health insurance + Reimbursement minimal contribution to health insurance + Reimbursement minimal contribution to nursing care insurance - Standard deduction for home country housing costs + Extra costs in host country Amount guaranteed in host currency Amount guaranteed in home currency Total net remuneration in host currency + Employee's social security contributions to pension insurance +Employee's social security contributions to unemployment insurance Total net remuneration in host currency including home social security Amount guaranteed in home currency incl. social security Payment of expatriate salary Payment of amount guaranteed in home currency annual Payment of amount guaranteed in home currency monthly Remaining amount paid in host currency annual Remaining amount paid in host currency monthly One time payments on beginning of assignment Relocation allowance Electrical allowance 15849 3696 600 3810 5904 439 51 15240 42845 690 000 115 005 136 54884573 169 889 709 8 106 168 1 343 769 6328 1049 179 339 646 50 222 42 845 3570 115 005 136 9 583 761 13 860 959 5000 Housing allowance and/or costs. There are several ways to reduce housing costs. One way is to select residence areas comparable to those used by local employees in comparable positions, thus avoiding expensive residence areas used mainly by expatriate employees. Another way is to follow the recommendations of housing data providers and to offer additional incentives for finding housing less expensive than the standard cost recommendations. However, as reported by KPMG, the overwhelming majority of companies (82 per cent) still do not provide this type of incentive. Travel expenses. There is a trend to provide 'economy' class travels to expatriate employees. About 56 per cent of companies surveyed by KMPG implement such a policy, 3 per cent more than in 2010. The rain had passed through the city and shafts of sunlight appeared through the grey clouds. Klaus recalled the themes of courage, curiosity and change" at the recent corporate meeting he had attended in Berlin. The Berlin conference was one of some 850 activities staged worldwide in 2011 to mark the 125th anniversary of the Bosch company and the 150th an- niversary of Robert Bosch's birth. He returned to his desk and began working to apply these themes. Many of the above cost reduction measures were al- ready being implemented at Bosch. Apart from the allowances, yearly 'economy' class flights to the home country had become the standard option for company travel. However, longer flights for business reasons can still be carried out using business class. The chal- lenge, however, was to further improve existing poli- cies by comparing several cost options, data providers and outsourcing alternatives. This would be just the first step towards designing an all-encompass- ing assignment policy, as further steps would analyze tax-efficient ways of providing expatriate perquisites, as well as organize taxation and social security cover- age during international assignments in cooperation with a team of international legal advisors. Nevertheless, enthusiastic and confident of suc- cess as he was, Klaus knew that designing a new international assignment policy was going to be a long and drawn out process involving multiple calculations as well as negotiations with colleagues and external mobility services providers. This was especially the case because the cost issue was only one aspect of the wider issue of the coordinated and strategically effective use of international assignment. There were many more related concerns - such as motivating potential expatriates, the impact of international assignments on professional careers, repatriation management, dual-career issues, and family income. The more Klaus thought about it the more he saw the linkages and implications operating across multiple HR practices and multiple product and geographic units. Questions: 1 Why did Bosch state the cost-of-living allowance amount as a CEHB-based sum and a separate cost-of-living supplement in the first and the second years of the assignment in the balance sheet for Korea? 2 Which expatriate compensation elements at Bosch Group were already based on cost reduction considerations listed in the case study? Please suggest ways in which these could be improved further. 3 What further cost-reduction measures could be implemented? 4 Do you believe it was possible to design a Bosch Group international assignment policy covering both expatriate and inpatriate employees at all international locations? 5 One of the measures used to reduce the costs of expatriation was to outsource elements of the administration function to external service providers. Please discuss the advantages and disadvantages of such a policy. 6 Do you believe that alternative assignments can substitute for traditional expatriate assignments in the long run? Please discuss the major opportunities and barriers. 7 What are the major barriers to the localization of expatriate managers? 8 Many international companies do not provide any additional foreign assignment allowances (e.g. relocation or hardship allowance). Do you think it would have been feasible to implement this system at Bosch? What would be the related advantages and disadvantages