Question: ANSWER ONLY NO.3 AND CREATE A CONCLUSION AND RECOMMENDATION REGARDING THIS PROBLEM That old equipment for producing subassemblies is worn out, said Paul Taylor, president

ANSWER ONLY NO.3 AND CREATE A CONCLUSION AND RECOMMENDATION REGARDING THIS PROBLEM

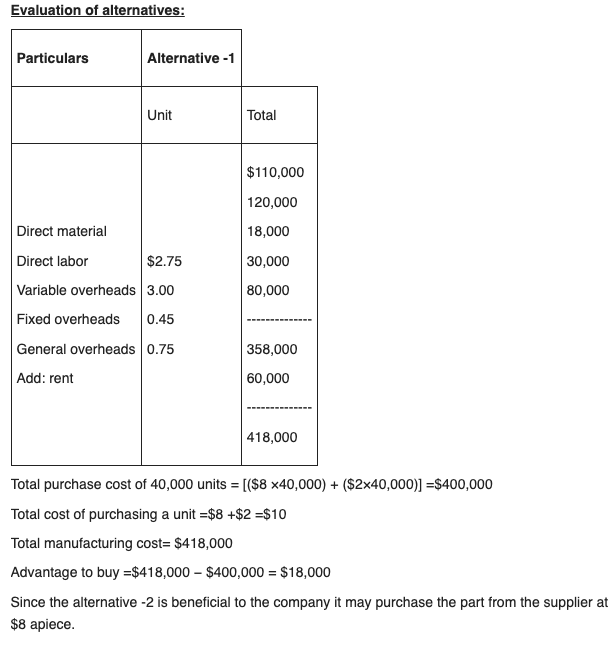

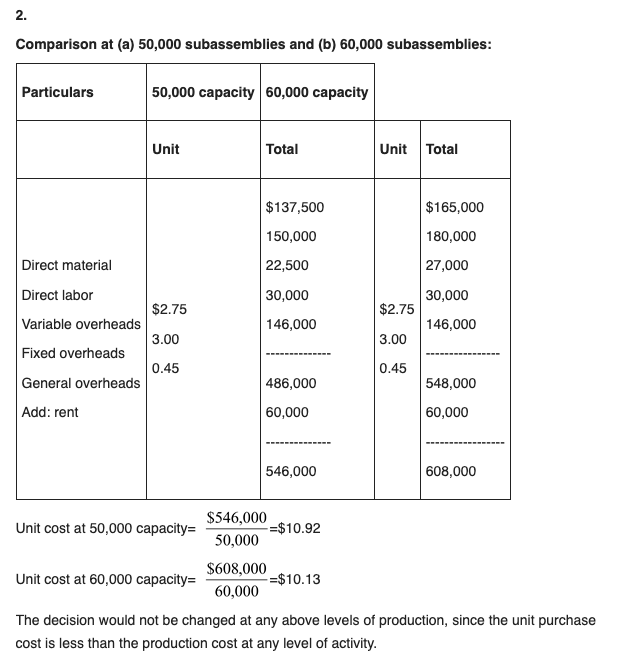

"That old equipment for producing subassemblies is worn out," said Paul Taylor, president of Timkin Company. "We need to make a decision quickly." The company is trying to decide whether it should rent new equipment and continue to make its subassemblies internally or whether it should discontinue production of its subassemblies and purchase them from an outside supplier. The alternatives follow: Alternative 1: Rent new equipment for producing the subassemblies for $60,000 per year. Alternative 2: Purchase subassemblies from an outside supplier for $8 each. Timkin Company's present costs per unit of producing the subassemblies internally (with the old equipment) are given below. These costs are based on a current activity level of 40,000 subassemblies per year: Direct materials $2.75 Direct labor 4.00 Variable overhead 0.60 Fixed overhead ($0.75 supervision, $0.90 depreciation, and $2 general 3.65 company overhead) Total cost per unit $ 11.00 The new equipment would be more efficient and, according to the manufacturer, would reduce direct labor costs and variable overhead costs by 25%. Supervision cost ($30,000 per year) and direct materials cost per unit would not be affected by the new equipment. The new equipment's capacity would be 60,000 subassemblies per year. The total general company overhead would be unaffected by this decision. 1. The president is unsure what the company should do and would like an analysis showing the unit costs and total costs for each of the two alternatives given above. Assume that 40,000 subassemblies are needed each year. Which course of action would you recommend to the president? 2. Would your recommendation in (1) above be the same if the company's needs were: (a) 50,000 subassemblies per year, or (b) 60,000 subassemblies per year? Show computations in good form. What other factors would you recommend that the company consider before making a decision? 3. Evaluation of alternatives: Particulars Alternative - 1 Unit Total $110,000 120,000 18,000 30,000 80,000 Direct material Direct labor $2.75 Variable overheads 3.00 Fixed overheads 0.45 General overheads 0.75 Add: rent 358,000 60,000 418,000 - Total purchase cost of 40,000 units = [($8 x40,000) + ($2x40,000)] =$400,000 Total cost of purchasing a unit =$8 +$2 =$10 Total manufacturing cost= $418,000 Advantage to buy =$418,000 - $400,000 = $18,000 Since the alternative-2 is beneficial to the company it may purchase the part from the supplier at $8 apiece. 2. Comparison at (a) 50,000 subassemblies and (b) 60,000 subassemblies: Particulars 50,000 capacity 60,000 capacity Unit Total Unit Total $165,000 $137,500 150,000 22,500 180,000 27,000 30,000 30,000 $2.75 $2.75 146,000 146,000 Direct material Direct labor Variable overheads Fixed overheads General overheads Add: rent 3.00 3.00 0.45 0.45 486,000 548,000 60,000 60,000 546,000 608,000 $546,000 Unit cost at 50,000 capacity= -=$10.92 50,000 $608,000 Unit cost at 60,000 capacity= -=$10.13 60,000 The decision would not be changed at any above levels of production, since the unit purchase cost is less than the production cost at any level of activity

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts