Question: Answer question #6, please. Assume the Face value is 100 Use bootstrapping to obtain a continuously compounded zero rate curve given the prices of the

Answer question #6, please. Assume the Face value is 100

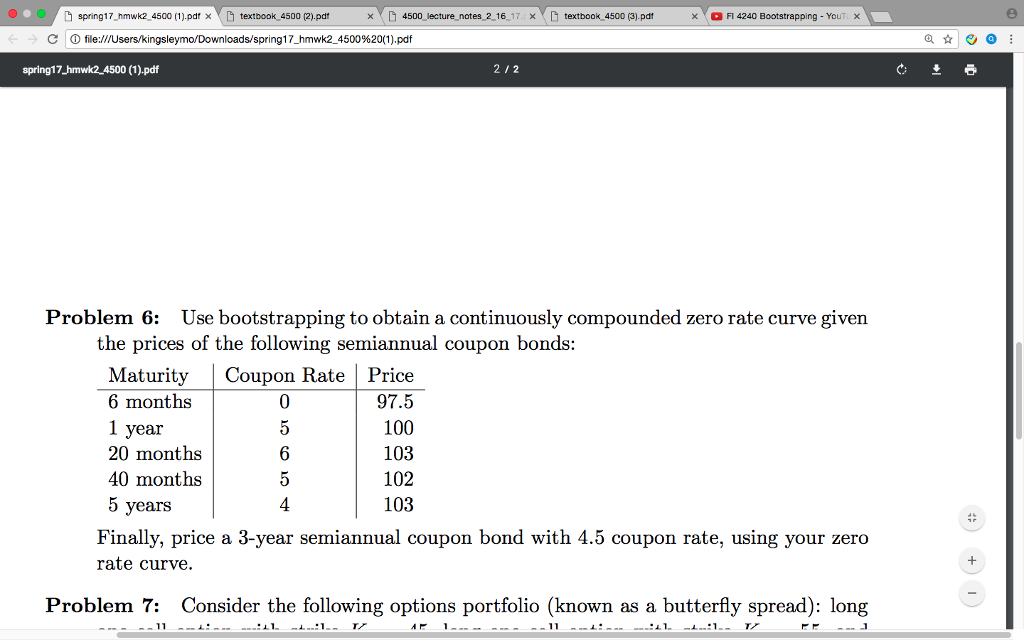

Use bootstrapping to obtain a continuously compounded zero rate curve given the prices of the following semiannual coupon bonds: Finally, price a 3-year semiannual coupon bond with 4.5 coupon rate, using your zero-rate curve. Consider the following options portfolio (known as a butterfly spread): long Use bootstrapping to obtain a continuously compounded zero rate curve given the prices of the following semiannual coupon bonds: Finally, price a 3-year semiannual coupon bond with 4.5 coupon rate, using your zero-rate curve. Consider the following options portfolio (known as a butterfly spread): long

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts