Question: Answer Questions 3 - 4 based on the following information. The following data are available relating to the performance of LU's Stock Fund and the

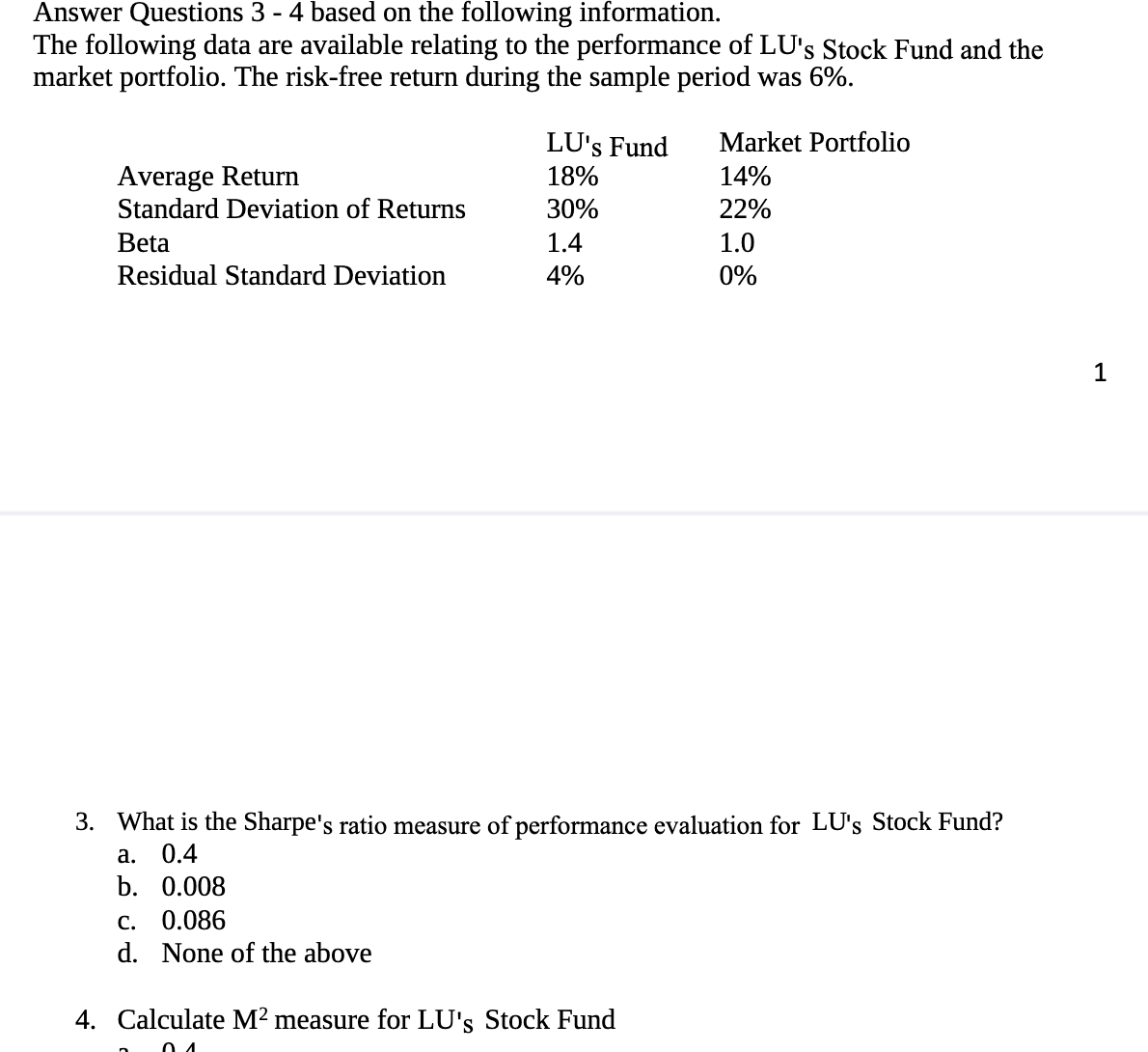

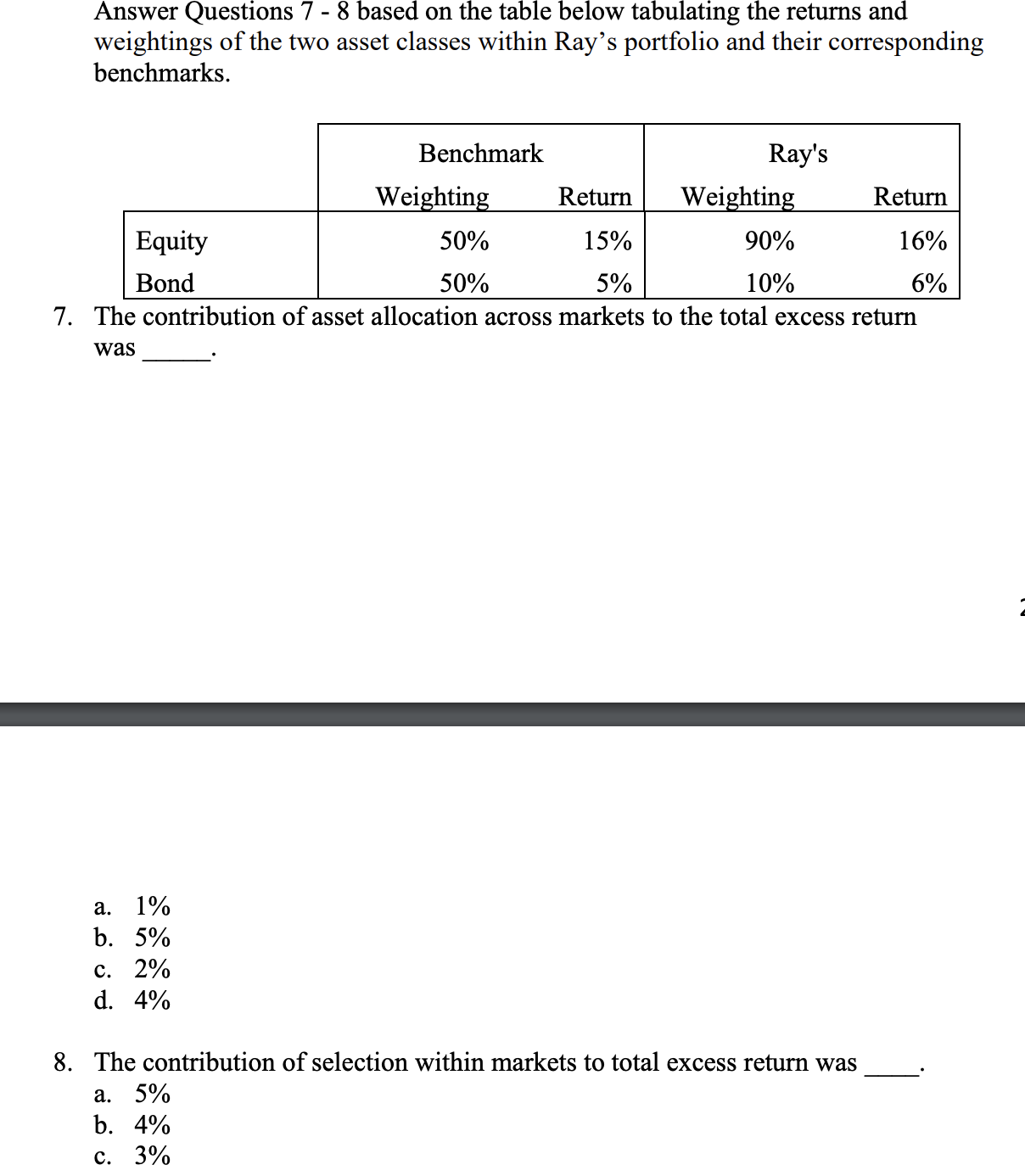

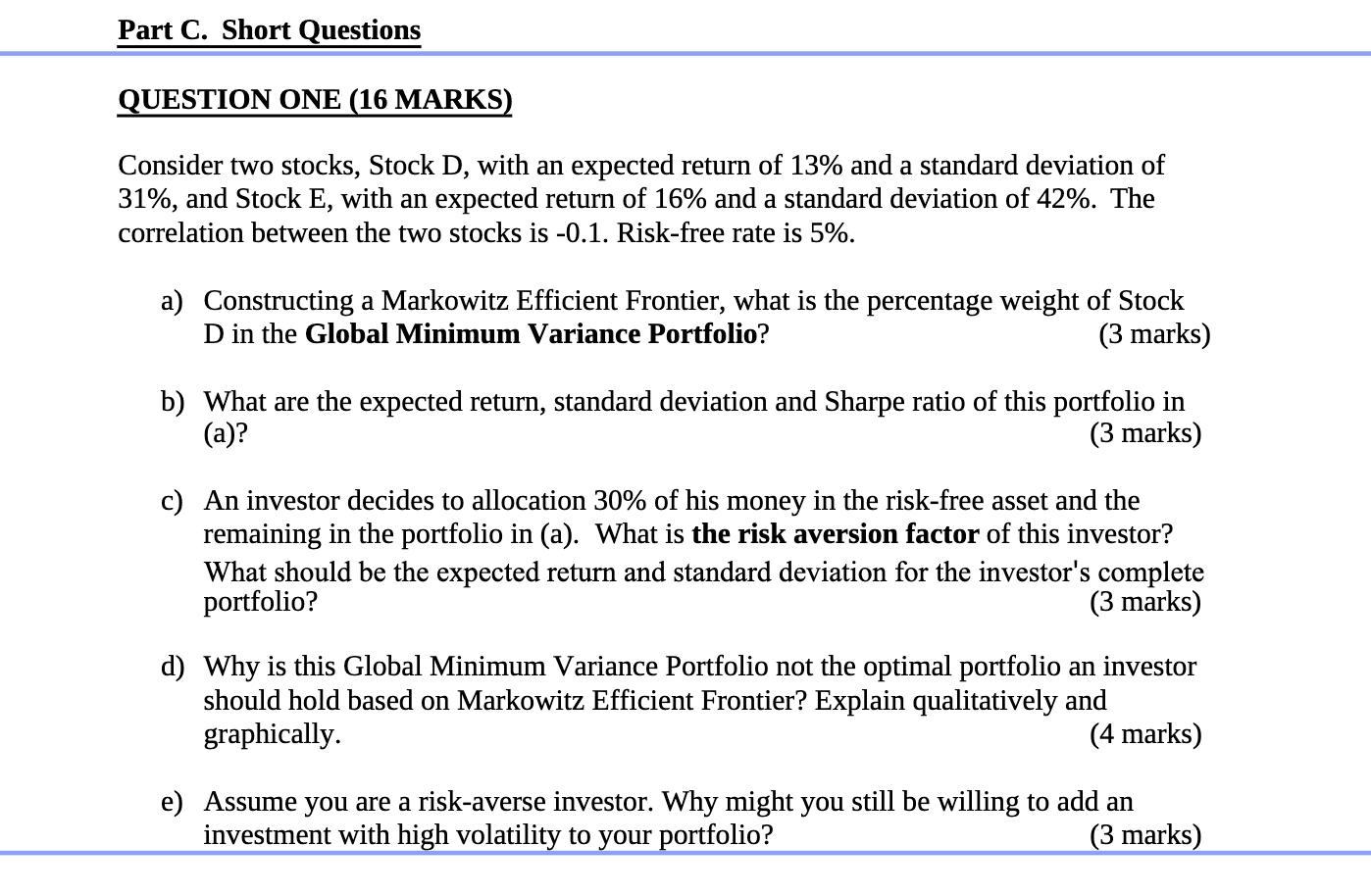

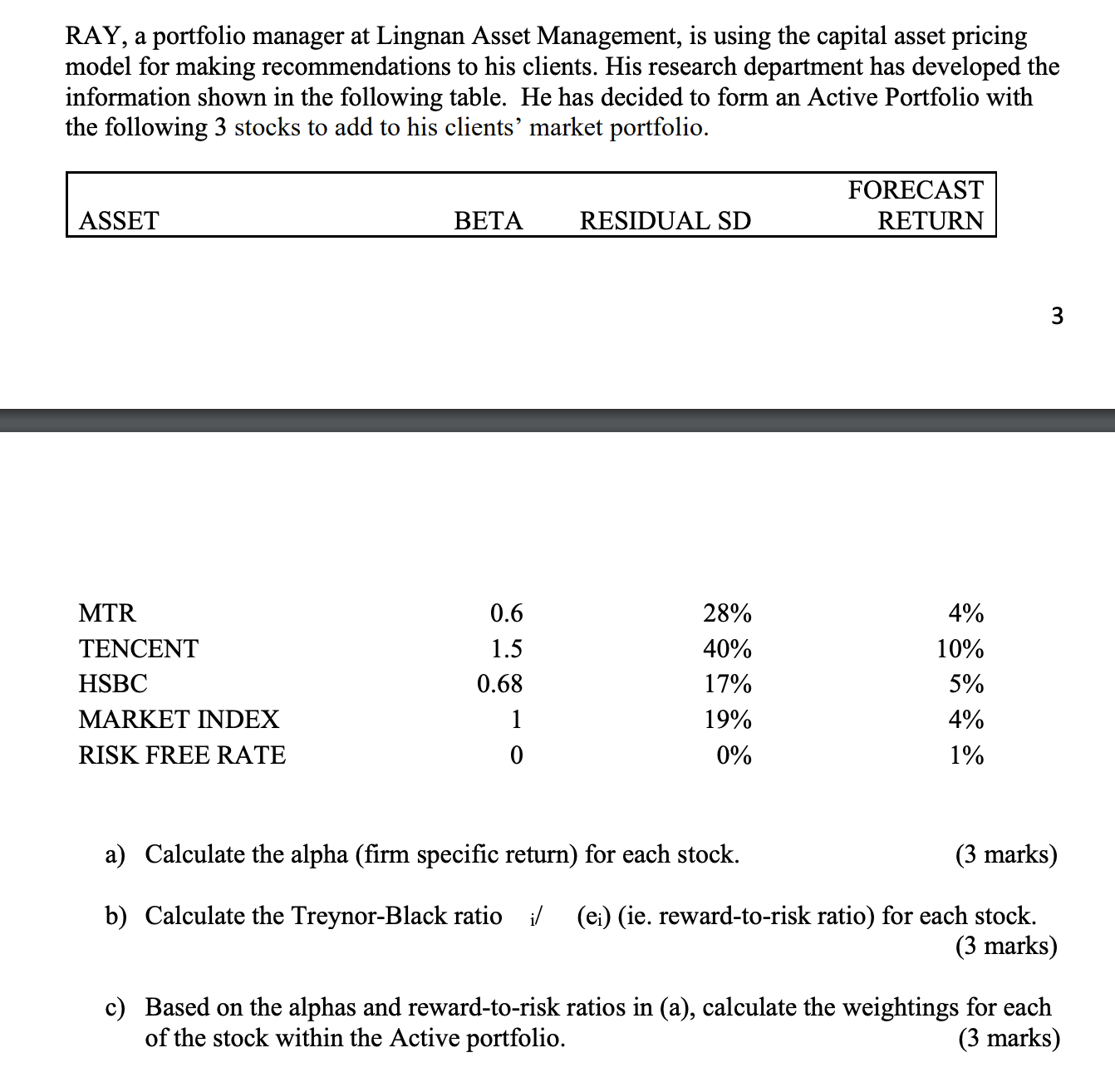

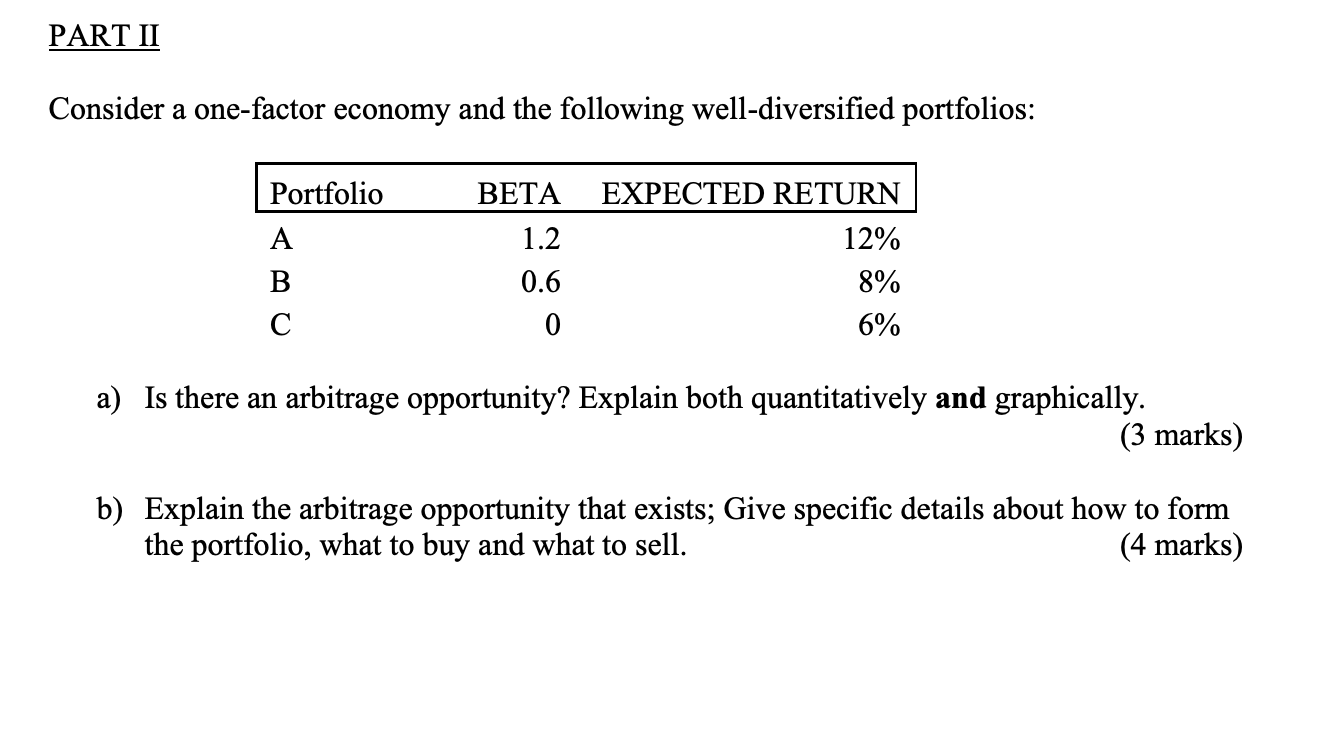

Answer Questions 3 - 4 based on the following information. The following data are available relating to the performance of LU's Stock Fund and the market portfolio. The risk-free return during the sample period was 6%. LU's Fund Market Portfolio Average Return 18% 14% Standard Deviation of Returns 30% 22% Beta 1.4 1.0 Residual Standard Deviation 4% 0% 3. What is the Sharpe's ratio measure of performance evaluation for LU's Stock Fund? a. 0.4 b. 0.008 c. 0.086 d. None of the above 4. Calculate M2 measure for LU's Stock Fund -~ n A 5. Based on a top-down investment approach, an investor should best follow the analyses order below: I. the global economy II. the industry outlook III. the value of a firm IV. the domestic economy IV, I, 11, then III L, IV, II then III IIL, IT, IV then I L, IIL, TV then II AN o 6. Suppose that the index model for a stock is estimated from the excess return with the following results: R =3% + 0.7 Rm + e; M = 20%; R-square = 0.2. What is the systematic standard deviation of this stock? a. 9.8% b. 14% c. 19.6% d. 31.3% Answer Questions 7 - 8 based on the table below tabulating the returns and weightings of the two asset classes within Ray's portfolio and their corresponding benchmarks. Benchmark Weighting Return | Weighting Return 50% 15% 90% 50% 5% 10% 7. The contribution of asset allocation across markets to the total excess return was Ray's a. 1% b. 5% c. 2% d. 4% 8. The contribution of selection within markets to total excess return was . a. 5% b. 4% c. 3% Part C. Short Questions QUESTION ONE (16 MARKS) Consider two stocks, Stock D, with an expected return of 13% and a standard deviation of 31%, and Stock E, with an expected return of 16% and a standard deviation of 42%. The correlation between the two stocks is -0.1. Risk-free rate is 5%. a) b) d) Constructing a Markowitz Efficient Frontier, what is the percentage weight of Stock D in the Global Minimum Variance Portfolio? (3 marks) What are the expected return, standard deviation and Sharpe ratio of this portfolio in (a)? (3 marks) An investor decides to allocation 30% of his money in the risk-free asset and the remaining in the portfolio in (a). What is the risk aversion factor of this investor? What should be the expected return and standard deviation for the investor's complete portfolio? (3 marks) Why is this Global Minimum Variance Portfolio not the optimal portfolio an investor should hold based on Markowitz Efficient Frontier? Explain qualitatively and graphically. (4 marks) Assume you are a risk-averse investor. Why might you still be willing to add an investment with high volatility to your portfolio? (3 marks) RAY, a portfolio manager at Lingnan Asset Management, is using the capital asset pricing model for making recommendations to his clients. His research department has developed the information shown in the following table. He has decided to form an Active Portfolio with the following 3 stocks to add to his clients\" market portfolio. FORECAST ASSET BETA RESIDUAL SD RETURN MTR 0.6 28% 4% TENCENT 1.5 40% 10% HSBC 0.68 17% 5% MARKET INDEX 1 19% 4% RISK FREE RATE 0 0% 1% a) Calculate the alpha (firm specific return) for each stock. (3 marks) b) Calculate the Treynor-Black ratio i/ (ei) (ie. reward-to-risk ratio) for each stock. (3 marks) ) Based on the alphas and reward-to-risk ratios in (a), calculate the weightings for each of the stock within the Active portfolio. (3 marks) PART II Consider a one-factor economy and the following well-diversified portfolios: Portfolio BETA EXPECTED RETURN A 1.2 12% B 0.6 8% C 0 6% a) Is there an arbitrage opportunity? Explain both quantitatively and graphically. (3 marks) b) Explain the arbitrage opportunity that exists; Give specific details about how to form the portfolio, what to buy and what to sell. (4 marks)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!