Question: 8-8. The following information is available for the preparation of the government- wide financial statements for the City of Northern Pines for the year

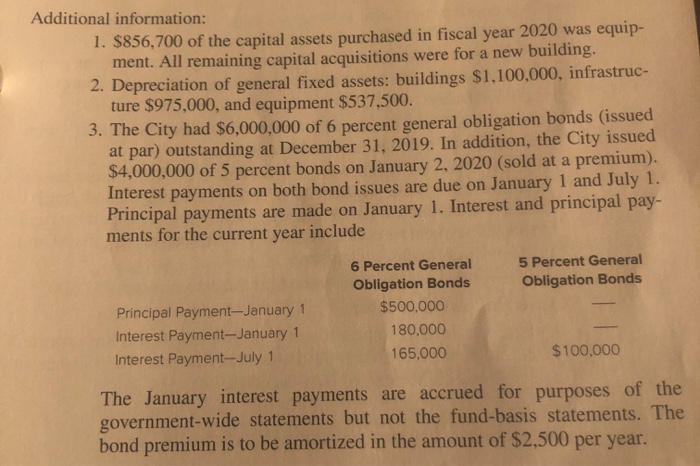

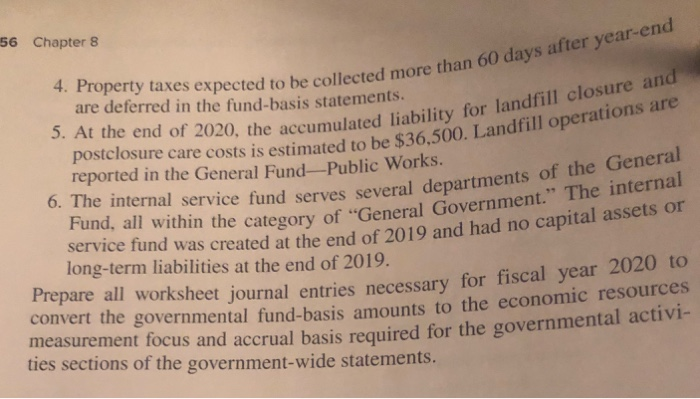

8-8. The following information is available for the preparation of the government- wide financial statements for the City of Northern Pines for the year ended June 30, 2020: Expenses: General government Public safety Public works $11,960,000 23,900,000 11,290,000 Health and sanitation 6,010,000 Culture and recreation 4,198,000 Interest on long-term debt, governmental type 721,000 Water and sewer system 10,710,000 Parking system 409,000 Revenues: Charges for services, general government 1,510,000 Charges for services, public safety 210,000 Operating grant, public safety 798,000 Charges for services, health and sanitation 2,355,000 Operating grant, health and sanitation 1,210,000 Charges for services, culture and recreation 1,998,000 Charges for services, water and sewer 11,588,000 Charges for services, parking system 388,000 Property taxes 27,112,000 20,698,000 Sales taxes 325,000 Investment earnings, business-type Special item-gain on sale of unused land, governmental type 1,250,000 Transfer from business-type activities to governmental activities 700,000 Net position, July 1, 2019, governmental 5,800,000 4,600,000 activities Net position, July 1, 2019, business-type activities From the previous information, prepare, in good form, a Statement of Activities for the City of Northern Pines for the year ended June 30, 2020. Northern Pines has no component units. 8-9. The City of Grinders Switch maintains its books in a manner that facilitates the preparation of fund accounting statements and uses worksheet adjustments to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations. 1. General fixed assets as of the beginning of the year, which had not been recorded, were as follows: Land Buildings Improvements Other Than Buildings Equipment Accumulated Depreciation, Capital Assets $7,554,000 33,355,000 14,820,000 11,690,000 25,800,000 2. During the year, expenditures for capital outlays amounted to $7,500,000. Of that amount, $4,800,000 was for buildings; the remainder was for improvements other than buildings. 3. The capital outlay expenditures outlined in (2) were completed at the end of the year (and will begin to be depreciated next year). For purposes of financial statement presentation, all capital assets are depreciated using the straight-line method, with no estimated salvage value. Estimated lives are as follows: buildings, 40 years; improvements other than buildings, 20 years; and equipment, 10 years. 4. In the governmental funds Statement of Revenues. Expenditures, and Changes in Fund Balances, the City reported proceeds from the sale of land in the amount of $600,000. The land originally cost $505,000. 5. At the beginning of the year, general obligation bonds were outstanding in the amount of $4,000,000. Unamortized bond premium amounted to $16,000. Note: This entry is not covered in the text, but is similar to entry 9 in the chapter. 250 Chapter 8 6. During the year, debt service expenditures for the year amounted to: interest, $580,000; principal, $412,000. For purposes of government- wide statements, $1,600 of the bond premium should be amortized. No adjustment is necessary for interest accrual. 7. At year-end, additional general obligation bonds were issued in the amount of $6,000,000, at par. LO 8-10. The City of South Pittsburgh maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations: 1. Deferred inflows of resources-property taxes of $51,200 at the end of the previous fiscal year were recognized as property tax revenue in the current year's Statement of Revenues, Expenditures, and Changes in Fund Balance. 2. The City levied property taxes for the current fiscal year in the amount of $10,000,000. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $200,000 is thought to be uncollectible, $349,000 would likely be collected during the 60-day period after the end of the fiscal year, and $53,800 would be collected after that time. The City had recognized the maximum of property taxes allowable under modified accrual accounting. 3. In addition to the expenditures recognized under modified accrual accounting, the City computed that $29,000 should be accrued for com- pensated absences and charged to public safety. 4. The City's actuary estimated that pension expense under the City's pub- lic safety employees pension plan is $229,000 for the current year. The City, however, only provided $212,000 to the pension plan during the current year. 5. In the Statement of Revenues, Expenditures, and Changes in Fund Balances, General Fund transfers out included $500,000 to a debt service fund, $200,000 to a special revenue fund, and $850,000 to an enterprise fund. 8-11. The City of Southern Pines maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to pre- pare government-wide statements. As such, the City's internal service fund, a motor pool fund, is included in the proprietary funds statements. Prepare necessary adjustments in order to incorporate the internal service fund in the government-wide statements as a part of governmental activities. 1. Balance sheet asset accounts include: Cash, $100,000; Investments, $125,000; Due from the General Fund, $15,000; Inventories, $325,000; and Capital Assets (net), $960,000. Liability accounts include: Accounts Payable, $50,000; Long-Term Advance from Enterprise Fund, $600,000. 2. The only transaction in the internal service fund that is external to the government is interest revenue in the amount of $3,600. Government-wide Statements, Capital Assets, Long-Term Debt 251 3. Exclusive of the interest revenue, the internal service fund reported net income in the amount of $24,000. An examination of the records indicates that services were provided as follows: one-third to gen- eral government, one-third to public safety, and one-third to public works. 8-12. Presented on the following pages are partial financial statements for the City of Shenandoah, including Fiscal year 2020: A. Total Governmental Funds: Balance Sheet Statement of Revenues, Expenditures, and Changes in Fund Balances B. Internal Service Fund: Statement of Net Position Statement of Revenues, Expenses, and Changes in Net Position Fiscal year 2019: A. Total Governmental Funds: Balance Sheet B. Government-wide-Governmental Activities: Statement of Net Position Assets CITY OF SHENANDOAH Balance Sheet Governmental Funds December 31, 2020 December 31, Total Governmental Funds 2019 Total Governmental Funds Cash and cash equivalents $1,372,900 $1,029,675 Investments 136,450 102,338 Receivables: Taxes Interest 97,522 73,142 28,768 31,325 Due from state government 513,000 384,750 Total assets 2,148,640 1,621,230 Liabilities and deferred inflows Accounts payable 46,600 17.950 Due to other funds 10,200 10.400 Deferred inflows: property taxes 78.000 65,000 Total liabilities and deferred inflows 134,800 93,350 (Continued Additional information: 1. $856,700 of the capital assets purchased in fiscal year 2020 was equip- ment. All remaining capital acquisitions were for a new building. 2. Depreciation of general fixed assets: buildings $1,100,000, infrastruc- ture $975,000, and equipment $537,500. 3. The City had $6,000,000 of 6 percent general obligation bonds (issued at par) outstanding at December 31, 2019. In addition, the City issued $4,000,000 of 5 percent bonds on January 2, 2020 (sold at a premium). Interest payments on both bond issues are due on January 1 and July 1. Principal payments are made on January 1. Interest and principal pay- ments for the current year include Principal Payment-January 1 Interest Payment-January 1 Interest Payment-July 1 6 Percent General Obligation Bonds 5 Percent General Obligation Bonds $500,000 180,000 165,000 $100,000 The January interest payments are accrued for purposes of the government-wide statements but not the fund-basis statements. The bond premium is to be amortized in the amount of $2,500 per year. 56 Chapter 8 4. Property taxes expected to be collected more than 60 days after year-end are deferred in the fund-basis statements. 5. At the end of 2020, the accumulated liability for landfill closure and postclosure care costs is estimated to be $36,500. Landfill operations are reported in the General Fund-Public Works. 6. The internal service fund serves several departments of the General Fund, all within the category of "General Government." The internal service fund was created at the end of 2019 and had no capital assets or long-term liabilities at the end of 2019. Prepare all worksheet journal entries necessary for fiscal year 2020 to convert the governmental fund-basis amounts to the economic resources measurement focus and accrual basis required for the governmental activi- ties sections of the government-wide statements.

Step by Step Solution

There are 3 Steps involved in it

To address the questions one at a time lets start with question 88 requesting the preparation of a S... View full answer

Get step-by-step solutions from verified subject matter experts