Question: (Answer should follow the template provided deriving underlying and derivative price in the binomial tree construction) Consider a six-month American put option to sell one

(Answer should follow the template provided deriving underlying and derivative price in the binomial tree construction)

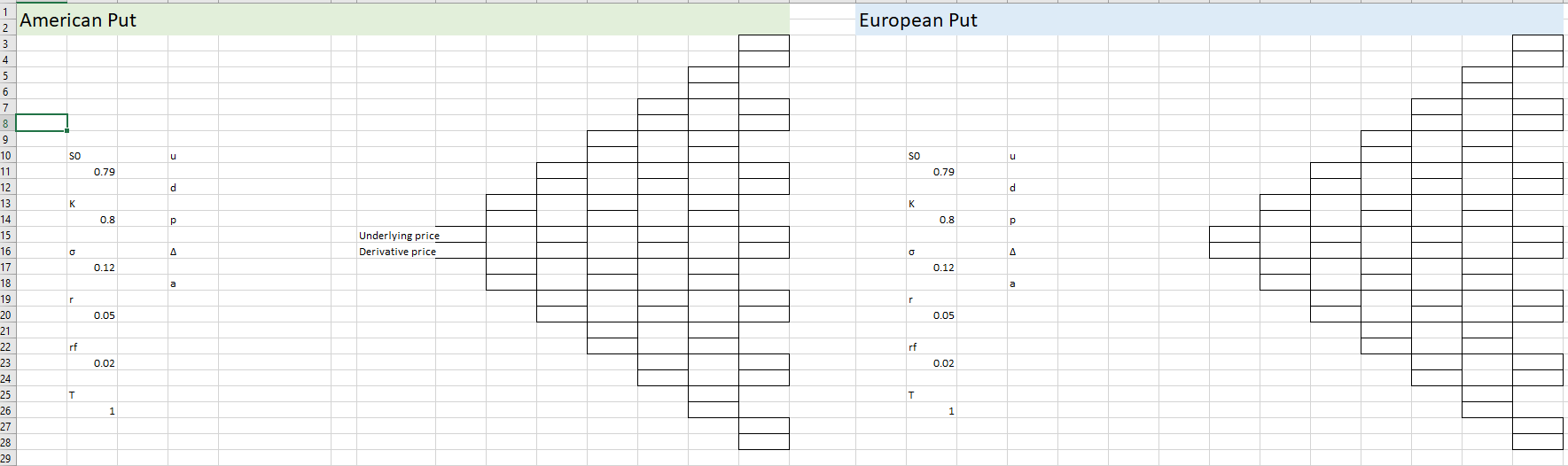

Consider a six-month American put option to sell one million units of a foreign currency. The current exchange rate is 0.79 and the strike price is 0.80 (both expressed as dollars per unit of the foreign currency). The volatility of the exchange rate is 12% per annum. The domestic and foreign risk-free rates are 5% and 2%, respectively.

a. Construct a six-step binomial tree for the price movement of the foreign currency.

b. Using the six-step binomial tree in Part (a), price the American put option by the riskneutral valuation method.

c. Calculate the early exercise premium for the American put option. (Early exercise premium is the cost of getting early exercise right.)

d. Suggest any improvement can be made in this valuation method.

European Put u SO u 0.79 d d K X p 0.8 p 1 American Put 3 4 5 6 7 8 9 10 SO 11 0.79 12 13 K 14 0.8 15 16 0 17 0.12 18 19 r 20 0.05 21 22 rf 23 0.02 24 25 26 1 27 28 29 Underlying price Derivative price A o A 0.12 a a 0.05 rf 0.02 T European Put u SO u 0.79 d d K X p 0.8 p 1 American Put 3 4 5 6 7 8 9 10 SO 11 0.79 12 13 K 14 0.8 15 16 0 17 0.12 18 19 r 20 0.05 21 22 rf 23 0.02 24 25 26 1 27 28 29 Underlying price Derivative price A o A 0.12 a a 0.05 rf 0.02 T

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts