Question: Answer the following question: Class 1 4% Class 1 - NRB (6%) Class 8 20% Class 10 30% Class 12 100% Class 13 SL Class

Answer the following question:

| Class 1 4% | Class 1 - NRB (6%) | Class 8 20% | Class 10 30% | Class 12 100% | Class 13 SL | Class 14.1 5% | Class 17 8% | Class 44 25% | |

| UCC 01/01/22 | 200000 | 60000 | 80000 | 37500 | 0 | ||||

| Additions: | |||||||||

| Software | 300 | ||||||||

| Building | 700000 | ||||||||

| Paving | 20000 | ||||||||

| Office Furniture | 25000 | ||||||||

| Unlimited Life Franchise | 100000 | ||||||||

| 10-year license | 20000 | ||||||||

| Leasehold improvements | 28000 | ||||||||

| Disposals: | |||||||||

| Building | -180000 | ||||||||

| Tools | -500 | ||||||||

| Furniture | |||||||||

| UCC 12/31/22 | 20000 | 700000 | 81000 | 80000 | -200 | 65500 | 100000 | 20000 | 20000 |

| AII Adjustment | 350000 | 10500 | 50000 | 10000 | 10000 | ||||

| UCC before CCA | 20000 | 1050000 | 91500 | 80000 | -200 | 65500 | 150000 | 30000 | 30000 |

| CCA | -63000 | -18300 | -24000 | -11000 | -7500 | -2400 | -7500 | ||

| Terminal Loss | -20000 |

Only answer these questions and explain clearly:

1. Why is Class 1 - NRB (6%) and Class 17 (8%) included in th chart if they are in this list: Eligible property includes all property except for CCA classes 1 to 6 , 14.1, 17, 47, 49, and 51?

2. How is the 10500 calculated for Class 8 20% AII?

3. Why does Class 1 4% have a terminal loss and where did it come from?

4. Why is there no AII adjustment for the other classes such as Class 10, 12, 13 extra?

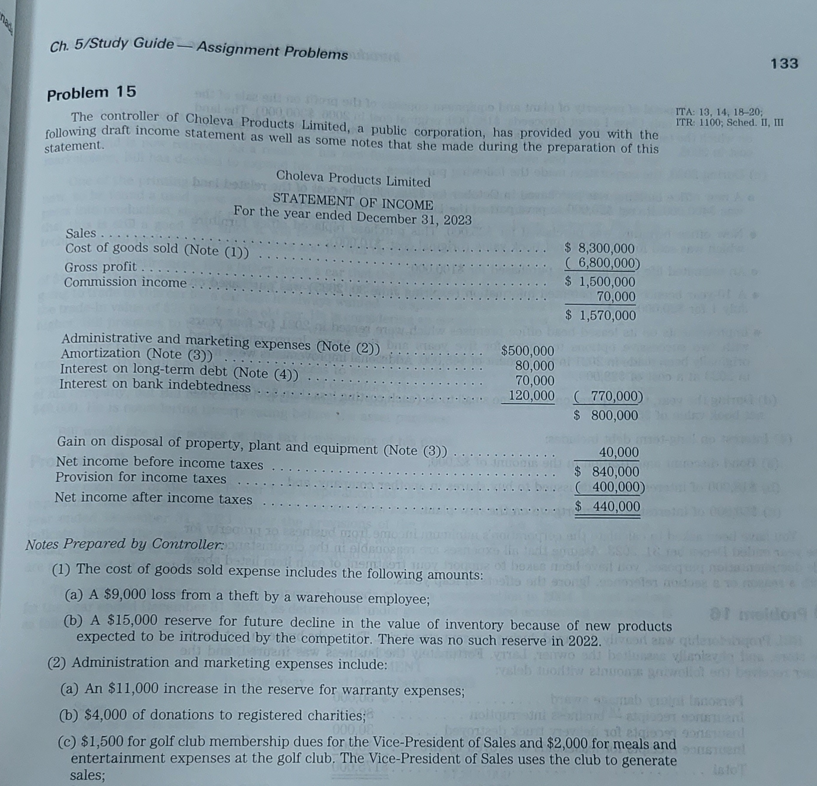

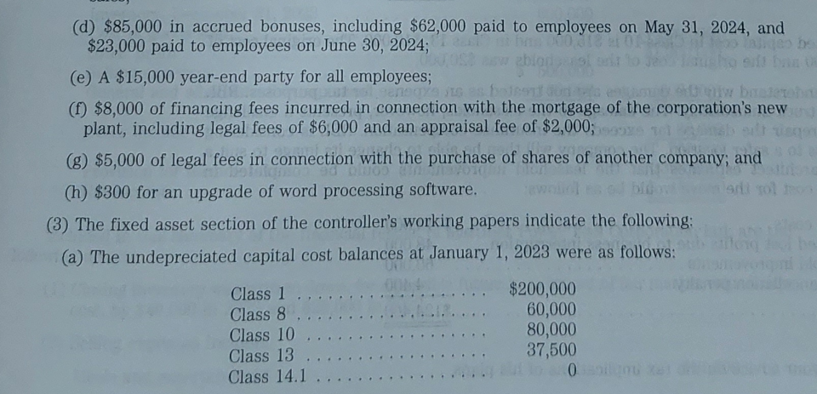

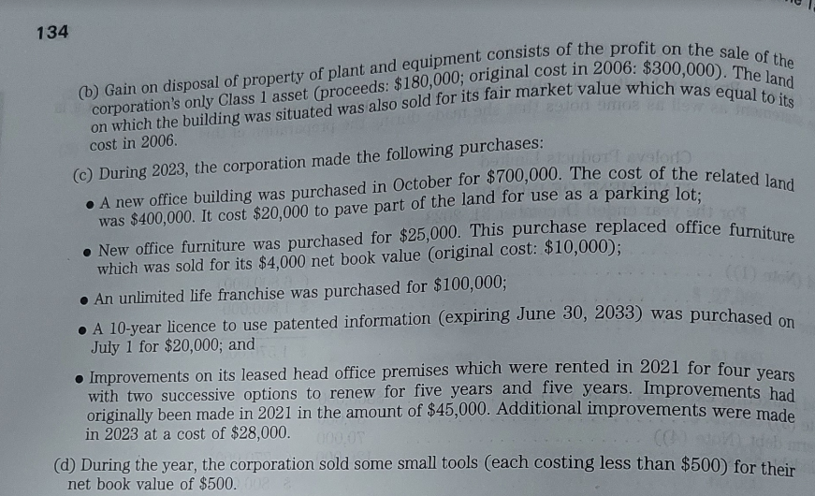

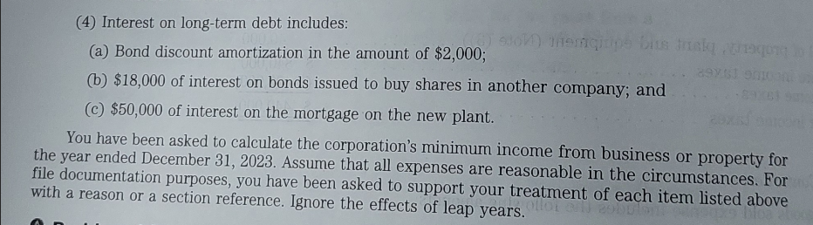

134 (b) Gain on disposal of property of plant and equipment consists of the profit on the sale of the corporation's only Class 1 asset (proceeds: $180,000; original cost in 2006:$300,000 ). The land on which the building was situated was also sold for its fair market value which was equal to its cost in 2006. (c) During 2023, the corporation made the following purchases: - A new office building was purchased in October for $700,000. The cost of the related land was $400,000. It cost $20,000 to pave part of the land for use as a parking lot; - New office furniture was purchased for $25,000. This purchase replaced office furniture which was sold for its $4,000 net book value (original cost: $10,000 ); - An unlimited life franchise was purchased for $100,000; - A 10-year licence to use patented information (expiring June 30, 2033) was purchased on July 1 for $20,000; and - Improvements on its leased head office premises which were rented in 2021 for four years with two successive options to renew for five years and five years. Improvements had originally been made in 2021 in the amount of $45,000. Additional improvements were made in 2023 at a cost of $28,000. (d) During the year, the corporation sold some small tools (each costing less than $500 ) for their net book value of $500. Droblem 15 TA: 13,14,1820; TR: 1100 ; Sched. II, III (a) An $11,000 increase in the reserve for warranty expenses; (b) $4,000 of donations to registered charities; (c) $1,500 for golf club membership dues for the Vice-President of Sales and $2,000 for meals and entertainment expenses at the golf club. The Vice-President of Sales uses the club to generate sales; (4) Interest on long-term debt includes: (a) Bond discount amortization in the amount of $2,000; (b) $18,000 of interest on bonds issued to buy shares in another company; and (c) $50,000 of interest on the mortgage on the new plant. You have been asked to calculate the corporation's minimum income from business or property for year ended December 31, 2023. Assume that all expenses are reasonable in the circumstances. For le documentation purposes, you have been asked to support your treatment of each item listed above th a reason or a section reference. Ignore the effects of leap years. (d) $85,000 in accrued bonuses, including $62,000 paid to employees on May 31,2024 , and $23,000 paid to employees on June 30,2024 ; (e) A $15,000 year-end party for all employees; (f) $8,000 of financing fees incurred in connection with the mortgage of the corporation's new plant, including legal fees of $6,000 and an appraisal fee of $2,000; (g) $5,000 of legal fees in connection with the purchase of shares of another company; and (h) $300 for an upgrade of word processing software. (3) The fixed asset section of the controller's working papers indicate the following

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts