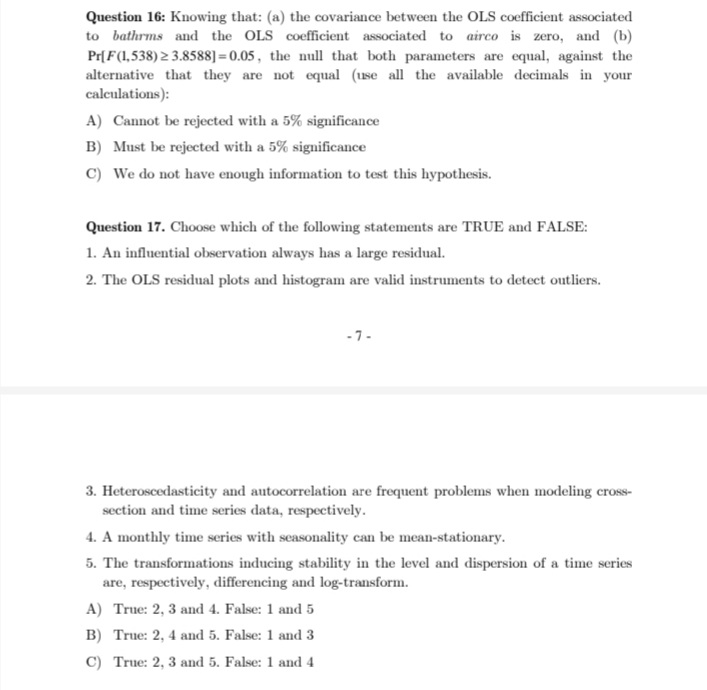

Question: Answer the following question please Table 6 Model : OLS, using observations 1960:2-2009:4 (T = 199) Dependent variable: d_c Coefficient Std. error T-ratio P-value const

![P-value const 0.00554085 0.000601578 9.2105 F*] C) 1-Pr[F (3,27) 2 F ]](https://s3.amazonaws.com/si.experts.images/answers/2024/06/666a9b0c4c913_540666a9b0c2b227.jpg)

![$4.61]=0.90 and Prix (2) $5.99]=0.95, the null that the model errors (U;](https://s3.amazonaws.com/si.experts.images/answers/2024/06/666a9b0e7a445_542666a9b0e4cfea.jpg)

Answer the following question please

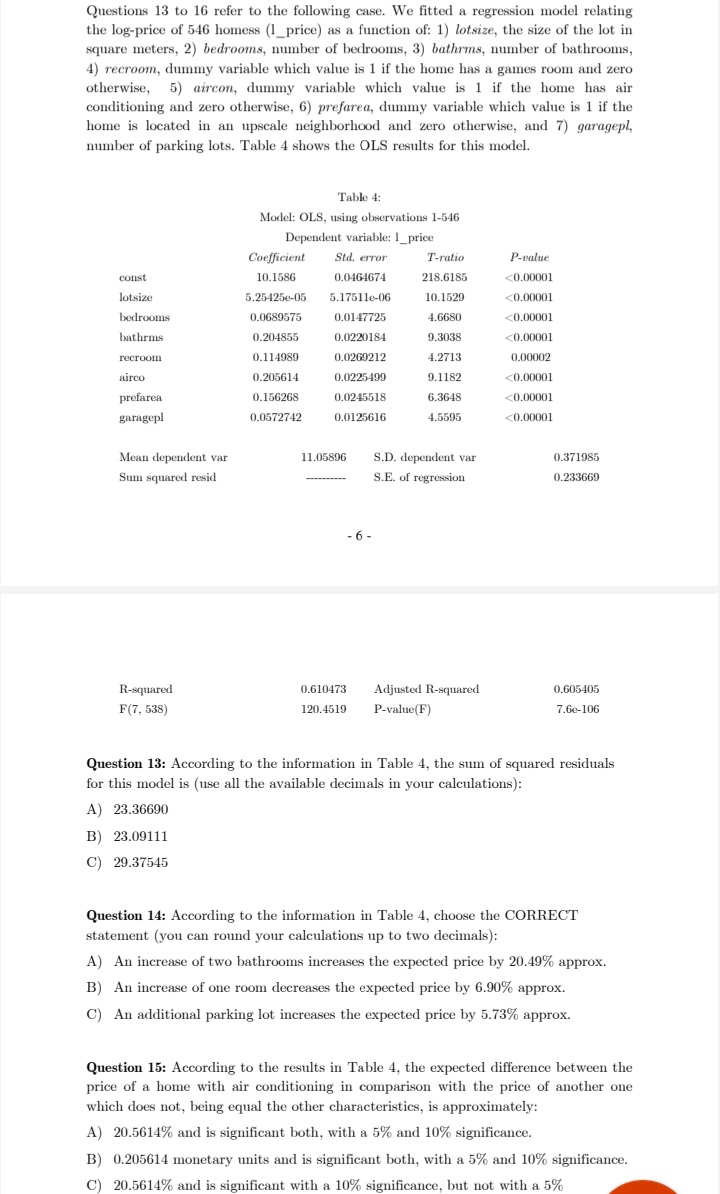

Table 6 Model : OLS, using observations 1960:2-2009:4 (T = 199) Dependent variable: d_c Coefficient Std. error T-ratio P-value const 0.00554085 0.000601578 9.2105 F*] C) 1-Pr[F (3,27) 2 F ] Question 7. Consider the model Y, = /+BX; +U, (i=1,2....,20), which OLS residuals are denoted by a; (i=1,2,...,20). Assume that the OLS estimation of the regression (with constant term) of U. as a function of X; and X? (i=1,2,...,20) yields a R' value of 0.35. If Pr[x (2) $4.61]=0.90 and Prix (2) $5.99]=0.95, the null that the model errors (U; ) are homoscedastic: A) Must be rejected with a 5% significance, but not with a 10% B) Must be rejected both, with a 5% and a 10% significance. C) Must be rejected with a 10% significance, but not with a 5% Question 8. The test used in the previous question is known as: A) Structural change test. B) Breusch-Godfrey test. C) White test.Question 1. After estimating by OLS a multiple regression model, the resulting residuals: A) Add up to zero if a constant term was included in the model. B) Are orthogonal to the model regressors only if a constant term was included in the model. C) Have constant variances and null covariances whenever the model errors have these properties. Question 2. In the regression model Y, = A + BX, +U, , t=1,2, ..., n where F =0 , the OLS estimator of B is: A) B= EY,x, SY,X, B) B =

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts