Question: Answer the last one (1 point) We model the value of an asset at time T in the future, by S-100+10x where X is random

Answer the last one

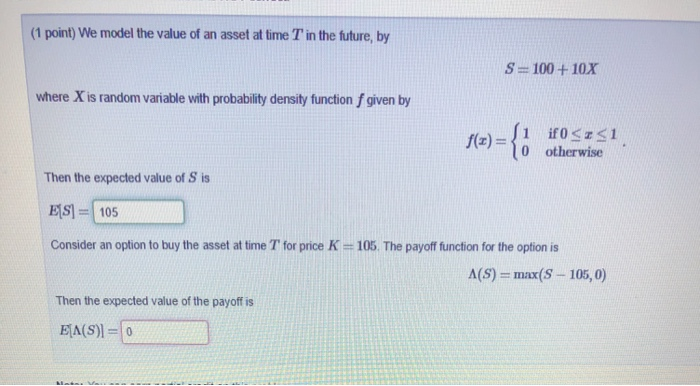

(1 point) We model the value of an asset at time T in the future, by S-100+10x where X is random variable with probability density function f given by f(x)-o otherwise Then the expected value of S is Es 105 Consider an option to buy the asset at time T for price K 105. The payoff function for the option is A(S) = max(S-105, 0) Then the expected value of the payoff is EA(S)-0

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock