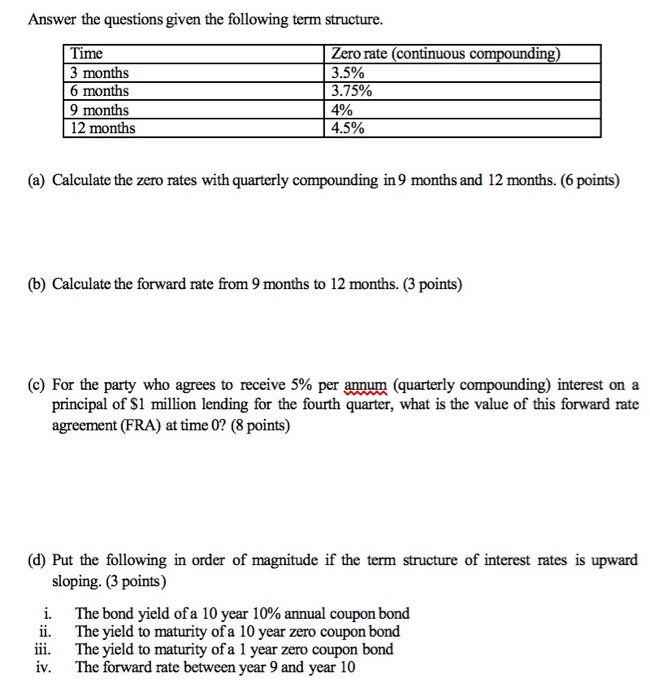

Question: Answer the questions given the following term structure. Time 3 months 6 months 9 months 12 months Zero rate (continuous compounding) 3.5% 3.75% 4% 4.5%

Answer the questions given the following term structure. Time 3 months 6 months 9 months 12 months Zero rate (continuous compounding) 3.5% 3.75% 4% 4.5% (a) Calculate the zero rates with quarterly compounding in 9 months and 12 months. (6 points) (b) Calculate the forward rate from 9 months to 12 months. (3 points) (c) For the party who agrees to receive 5% per annum (quarterly compounding) interest on a principal of $1 million lending for the fourth quarter, what is the value of this forward rate agreement (FRA) at time 0? (8 points) (d) Put the following in order of magnitude if the term structure of interest rates is upward sloping. (3 points) i. The bond yield of a 10 year 10% annual coupon bond ii. The yield to maturity of a 10 year zero coupon bond iii. The yield to maturity of a 1 year zero coupon bond iv. The forward rate between year 9 and year 10

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts