Question: Answer what is required on problem 6-2,6-3 and 6-4 Forms of income statement Functional income statement PAS 1, paragraph 99, provides that an entity shall

Answer what is required on problem 6-2,6-3 and 6-4

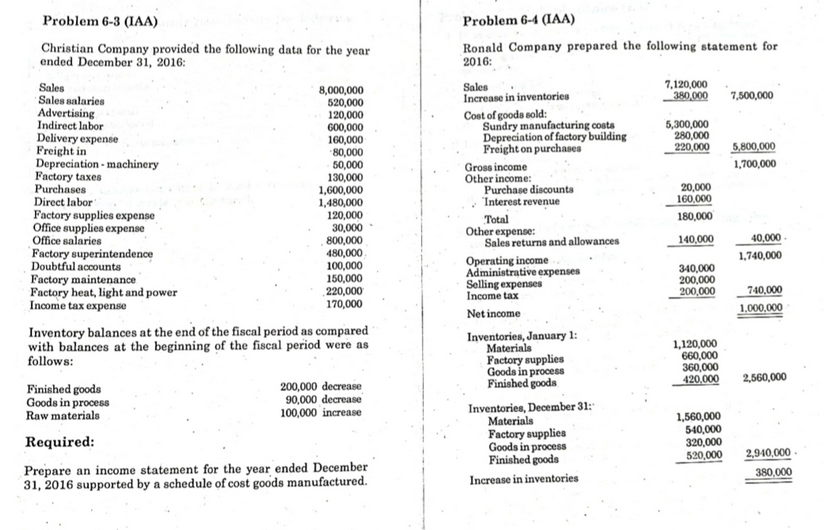

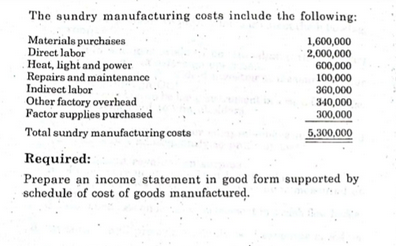

Forms of income statement "Functional" income statement PAS 1, paragraph 99, provides that an entity shall present an analysis of expenses recognized in profit or loss using a EXAMPLAR COMPANY classification based on either the function of expenses or their Income Statement nature within the entity, whichever provides information Year ended December 31, 2016 that in reliable and more relevant Note Net sales (1) Accordingly, the income statement may be presented in two 9,000,000 ways, namely functional and natural. Cost of goods sold (6.400,000) Gross income 3,600,000 Functional presentation Other income (3) 900,000 Investment income 500,000 This form classifies expenses according to their function as Total income 5,000,00D part of cost of goods sold, distribution costs, administrative expenses and other expenses. Expenses: Distribution costs 1,350,000 Administrative expenses 1.000.000 The functional presentation is also known as the cost of goods Other expenses 320,000 sold method. Finance cost 200.000 2,870.000 An entity classifying expenses by function shall disclose Income before tax 2.130,000 additional information on the nature of expenses, including Income tax expense 580,080 depreciation, amortization and employee benefit costs. Net income .550.000 Natural presentation Note 1 - Net sales The natural presentation is referred to as the nature of Gross sales 9.300,000 100,000) expense method. Sales return and allowance Sales discount 200,000) Under this form, expenses are aggregated according to their Net sales 9,000,000 nature and not allocated among the various functions within the entity. Note 2 - Cost of goods sold In other words, the expenses are no longer classified as cost 1,500,000 of goods sold, distribution costs, administrative expenses and Inventory, January 1 other expenses. Purchases 5,000,000 Freight in 300,000 The expenses which are of the same nature are grouped or Total 6,300,000 Purchase return and allowance 150,000) aggregated and presented as one item. Purchase discount 250,000) 5,900,000 For example, depreciation, purchases of raw materials, Goods available for sale 7.400,000 transport costs, employee benefit costs and advertising costs Inventory, December 31 (2,000,000) are presented separately. Cost of sales 5.400,000 156 157 Presentation of comprehensive income Components of expense An entity has two options of presenting comprehensive income, namely: . Cost of goods sold or cost of sales 1. Two statements: b. Distribution costs or selling expenses c. Administrative expenses d. Other expenses or loss. a. An income statement showing the components of profit - c. Income tax expense b. A statement of comprehensive income beginning with profit or loss as shown in the income statement plus Cost of goods sold of merchandising concern or minus the components of other comprehensive income. Beginning inventory 500,000 Net purchases 2.000,090 2. Single statement of comprehensive income Goods available for sale 2,500,000 Ending inventory (300.000) This is the combined statement showing the components 2.200.000 of profit or loss and components of other comprehensive Cost of goods sold income in a single statement. Gross purchases 1,900,000 Sources of income Freight in 150.000 Total 2,050,000 Sales of merchandise to customers Purchase returns, allowances and discounts 50.000) The income from sales shall include all sales to customers Net purchases 2.000.000 during the period. Cost of goods sold of manufacturing concern Sales returns, allowances and discounts shall be deducted 500,000 from gross sales to arrive at net sales. Beginning raw materials Net purchases 2.000.000 b. Rendering of services Raw materials available for use 2,500,090 Ending raw materials (100 050) Income from rendering of services, among others, includes professional fees, media advertising commissions. Raw materials used 2,200,000 insurance agency commissions, admission fees for artistic Direct Inbor 3,000,000 Factory overhead 1.300.000 performance and tuition fees. 5,500,000 Total manufacturing cost 900,000 C. Use of entity resources Beginning goods in process Total cost of goods in process 7.400,000 This income category includes interest, rent, royalty and 1,000.900 * Ending goods in process dividend income. 5.400,000 Cost of goods manufactured 1,600,000 d. Disposal of resources other than products Beginning finished goods 8,000,090 Goods available for sale 1,500,000) Examples include gain on sale of investments, gain on Ending finished goods sale of property, plant and equipment and gain on sale of 6,500,000 Cost of goods sold intangible assets. 153 152 Note 3 - Other income Interest revenue "Natural" income statement Dividend revenue 180,000 Rent revenue 120,000 EXAMPLAR COMPANY Gain from expropriation 100,000 Income Statement Total 500,000 Year ended December 31, 2016 900.000 Note Note 4 - Investment income Net sales 9,000,000 Other income Share in net income of associate (25%) 900,000 500,000 Investment income 500,000 Note 5 - Distribution costs Total income 10.400,000 Sales salaries SSS and Philhealth - sales 600,000 Expenses: Sales commission 20,000 Increase in inventory ( 500,000) Advertising 180,000 Net purchases (5) 5,900,000 Employee benefit costs 10 1.400.000 Store supplies expense 100,000 Sales comm 160.000 50,000 Delivery expense Advertising 100,000 250,000 Supplica expense 120,000 Depreciation - store equipment 150,000 Delivery expense 250,000 Total distribution costs 1.250,000 Depreciation (5) 240,000 Taxes and 20,000 Note 6 - Administrative expenses Doubtful accounts Other expenses (9) 320.000 Office salaries Finance cost (10) 650,000 200.000 8.270.000 SSS and Philhealth - office 30,000 Income before tax 2,130,000 Bonuses 00,000 Income tax expense 580,000 Office supplies expense 70,000 Taxes and licenses Net income 1,550,000 20,000 Doubtful accounts 40,000 Depreciation - office equipment 90,00 Note 1-Net sales Total administrative expenses 1,000,000 Gross sales 9,300,000 100,000) Note 7 - Other expenses Sales return and allowance Sales discount 200,000) Loss on sale of investment 30,000 Net sales 9,000,000 Loss on sale of property 120,000 Casualty loss from earthquake 170,000 Note 2 -Other income Total 320,000 Interest revenue 180,000 Note 8 - Finance cost Dividend revenue 120,000 Interest expense on bank loan 50.000 Rent revenue 100,000 Gain from expropriation 500,000 Interest expense on bonds payable 150,000 900,000 Total finance cost 260,000 Total 159 Note 9-Other expensesNote 35 Investment income 2.36 Note 9-Other SP. Yep 61 Share in net income of associate (25%%) 500.090 Loss on sale of investment DOO'OE Loss on disposal of property 20,900 Note 4 - Increase in inventory Casualty loan from earthquake 170,090 320,000 Inventory . December 31 Total 2,000,000 Inventory . January 1 1,500,009 Note 10-Finance cost Increase in inventory 500,000 Interest expense on bank loan 50,000 Note 5 - Net purchases Interest expense on bonds payable 150,000 Total finance cost 200.000 Purchases 6,000,000 Freight in 300,000 Which form of income statement? Purchase return and allowance 150,000) Purchase discount (250,000) PAS 1 does not prescribe any format. Net purchases 5900.000 Paragraph 106 simply states that "because each method of Note 6 - Employee benefit costs presentation has merit for different types of entities, management is required to select the presentation that is Sales salaries 600,080 reliable and more relevant". SSS and Philhealth - sales 20.000 Office anlaries $50,000 Statement of comprehensive income SSS and Philhealth - office 30,000 Bonuses 100.000 As stated earlier, in addition to the income statement, a Total employee conta 1,400,000 statement of comprehensive income is also prepared in order to show the total comprehensive income. Note 7 -Supplies expense The statement of comprehensive income starts with the profit Store supplies 50.000 or loss as shown in the income statement plus or minus the Office supplies 70,000 components of other comprehensive . Total supplies expense 120,000 The purpose of this statement is to provide a more comprehensive information on financial performance Note 8 - Depreciation measured more broadly than the income as traditionally Depreciation . store 150,000 computed. Depreciation - office 10,000 Total depreciation 240.090 161 160 Illustration EXAMPLAR COMPANY Using the data in the preceding illustration, the statement Statement of Comprehensive Income of comprehensive income may appear as follows: Year Ended December 31, 2016 Net sales 9,000,000 EXAMPLAR COMPANY Statement of Comprehensive Income Cost of goods sold (5.400,000) Year Ended December 31, 2016 Gross income 3,600,000 Other income 900,000 Net income 1,560,000 Investment income 500,000 Other comprehensive income to be reclassified to profit or loss: 5,000,000 Foreign currency translation gain Total income 150,000 Unrealized loss on derivative contract Expensca: designated as cash flow hedge Distribution costs 1,350,000 (100,000) 50,000 Administrative expenses 1.000,000 Comprehensive income 1.600.000 Other expenses 320,000 Finance cost 200.000 2.870.000 Comprehensive income for a period includes the net Income before tax 2,130,000 income or loss for the period plus or minus the components Income tax expense 560,000 of other comprehensive income. Net income 1,550,000 Other comprehensive income to be reclassified to profit or loss: However, the comprehensive income of P1,600,000 is not Foreign currency translation gain 150.000 carried to retained earnings. Only the net income of Unrealized loss on derivative contract P1,550,000 is included in the determination of retained designated as cash flow hedge ( 100.000) 50,000 earnings unappropriated. Comprehensive income 1,600,000 The net other comprehensive income of P50,000 is carried to "reserves" or shown separately in the statement of changes Statement of retained earnings in equity. The statement of retained earnings shows the changes Single statement of comprehensive income affecting directly the retained earnings of an entity and relates the income statement to the statement of financial Another option in presenting the components of profit or position. loss and components of other comprehensive income is to The important data affecting the retained earnings that prepare a single statement of comprehensive income. should be clearly disclosed in the statement of retained Again, this single statement is the combined income earnings are: statement and statement of comprehensive income. a. Profit or loss for the period b. Prior period errors Using the preceding data, the single statement of c. Dividends declared and paid to shareholders comprehensive income following the "functional d. Effect of change in accounting policy presentation" may appear as follows: e. Appropriation of retained carnings 162 163 Illustration - all amounts are assumed Illustration - all amounts are assumed EXAMPLAR COMPANY EXAMPLAR COMPANY Statement of Retained Earnings Statement of Changes in Equity Year Ended December 31, 2016 Year Ended December 31, 2016 Retained earnings, January 1,000,000 Share Retained Correction of error resulting capital Reserves earnings from prior year underdepreciation Balances - January 1 5,000,000 2,000,000 1.080,000 Change in accounting policy from weighted ( 100,000) orrection of error resulting average to FIFO inventory valuation from priory ar underdepreciation (180,080) resulting in an increase 300,000 Change in accounting policy trem Corrected beginning balance whichted average to FIFO - credit 300,000 1,200,000 Net income for the period issuance of 10,000 ordinary shates 1,550,000 Dividenda declared during the year with P100 par at P150 per share 1,000,080 500,080 400,000) Appropriated for contingencies nuance of 5,000 preference shares 200,000) with PSD par at P100 per share 250,000 250,000 Retained earnings, December 31 2,150,000 Comprehensive income Net income 1,550,000 Statement of changes in equity Other comprehensive income 50,000 Dividenda paid during the year ( 400,080) The statement of changes in equity is a basic statement that Current appropriation for 200,000 ( 200.000) shows the movements in the elements or components of the contingencies shareholders' equity. Balances . December 21 6.250.000 3,090,000 2.150,000 The statement of retained earnings is no longer a required basic Statement of cash flows statement but it is a part of the statement of changes in equity. The statement of cash flows is a basic component of the An entity shall present a statement of changes in equity showing the following: financial statements which summarizes the operating. investing and financing activities of an entity. 1. Comprehensive income for the period. 2" For each component of equity, the effects of changes in In simple language, the statement of cash flows provides information about the cash receipts and cash payments of an accounting policies and corrections of errors. entity during a period. 3. For each component of equity, a reconciliation between the carrying amount at the beginning and end of the period, The preparation of the statement of cash flows and a more separately disclosing changes from: detailed discussion of the statement of financial position, a. Profit or loss income statement, statement of comprehensive income and statement of changes in equity are taken up exhaustively in b. Each item of other comprehensive income Financial Accounting, Volume Three. Transactions with owners in their capacity as owners showing separately contributions by and distributions to owners. 164 165 O QUESTIONS 16. Define administrative expenses.2:36 Fa Mo ull all 61 INTONE PRELIM NOTES... Q . . . expenses, gains, losses and net income or loss recognized statement. To understand the objective and usefulness of an income during the period. Information about financial performance is useful in To understand the concept of comprehensive income, profit predicting future performance and ability to generate future or loss and other comprehensive income. cash flows. To identify the components of other comprehensive income. Comprehensive income Comprehensive income is the change in equity during a period To understand the subsequent reclassification of the resulting from transactions and other events, other than components of other comprehensive income. changes resulting from transactions with owners in their capacity as owners. To know the minimum line items in the statement of comprehensive income. Accordingly, comprehensive income includes: Components of profit or loss o know the natural and functional presentation of the b. Components of other comprehensive income income statement. Profit or loss to be able to prepare and present a separate income statement and a single statement of comprehensive The term "profit or loss" is the total of income less expenses, income. excluding the components of other comprehensive income. In other words, this is the "bottom line" in the traditional income statement. An entity may use "net income" or "net loss" to describe profit or loss. 148 149 Other comprehensive income (OCD) Components of OCI that will be reclassified subsequently Other comprehensive income comprises items of income and to profit or loss include: expenses including reclassification adjustments that are not recognized in profit or loss as required or permitted by n. Unrealized gain or loss on debt investment measured Philippine Financial Reporting Standards. at fair value through other comprehensive income. The components of "other comprehensive income" include Gain or loss from translating financial statements of a the following: foreign operation. 1. Unrealized gain or loss on equity investment measured c. Unrealized gain or loss on derivative contracts designated at fair value through other comprehensive income as cash flow hedge. 2. Unrealized gain or loss on debt investment measured Components of OCI that will not be reclassified at fair value through other comprehensive income. subsequently to profit or loss include: 3. Gain or loss from translation of the financial statements a. Unrealized gain or loss on equity investment measured of a foreign operation at fair value through other comprehensive income. 4. Revaluation surplus during the year. The Application Guidance of PFRS 9, paragraph B5.7.1, 5. Unrealized gain or loss from derivative contracts provides that such unrealized gain or loss is reclassified designated as cash flow hedge to retained earnings upon disposal of the investment. 5. "Remeasurements" of defined benefit plan, including b. Revaluation surplus during the year actuarial gain or loss The realization of the revaluation surplus is through 7. Change in fair value attributable to credit risk of a retained earnings. financial liability designated at fair value through profit c. Remeasurements of defined benefit plan, including or loss. actuarial gain or loss. Presentation of other comprehensive income The remeasurements are not reclassified subsequently but are permanently excluded from profit or loss. PAS 1, paragraph 82A, provides that the statement of comprehensive income shall present line items for amounts However, the remeasurements may be transferred within of other comprehensive income during the period classified equity or retained earnings. by nature. d. Change in fair value attributable to credit risk of a The line items for amounts of OCI shall be grouped as follows: financial liability designated at fair value through profit OCI that will be reclassified subsequently to profit or or loss. loss when specific conditions are met, Such gain or loss from change in fair value attributable to credit risk of a financial liability may be transferred b. OCI that will not be reclassified subsequently to profit within equity or retained earnings. or loss. 150 151 Classifications of expenses No more extraordinary items Distribution costs constitute costs which are directly related to selling, advertising and delivery of goods to customers. PAS 1, paragraph 87, specifically mandates that an entity shall not present any items of income and expense as Distribution costs ordinarily include: extraordinary items, either on the face of the income statement or statement of comprehensive income or in the Salesmen's salaries notes. b. Salesmen's commissions C. Traveling and marketing expenses Line items 1. Advertising and publicity e. Freight out PAS 1, paragraph 82, provides that as a minimum, the income f. Depreciation of delivery equipment and store equipment statement and statement of comprehensive income shall include the following line items. Administrative expenses constitute cost of administering the business. Revenue Administrative expenses ordinarily include all operating b. Gain and loss from the derecognition of financial asset measured at amortized cost as required by PFRS 9. expenses not related to selling and cost of goods sold. Finance cost Examples include: d. Share in income or loss of associate and joint venture accounted for using the equity method a.. Doubtful accounts c. Income tax expense b. Office salaries A single amount comprising discontinued operations c. Expenses of general executives g. Profit or loss for the period d. . Expenses of general accounting and credit department h. Total other comprehensive income e. Office supplies used Comprehensive income for the period being the total of f. Certain taxes profit or loss and other comprehensive income. Contribution h. Professional fees The following items shall be disclosed on the face of the Depreciation of office building and office euipment income statement and statement of comprehensive income: j. Amortization of intangible assets Profit or loss for the period attributable to noncontrolling Other expenses are those expenses which are not directly interest and owners of the parent related to the selling and administrative function. . Total comprehensive income for the perio" Examples include: to noncontrolling interest and owners of . Loss on sale of trading investments . Loss on disposal of property, plant and equipment c. Loss on sale of noncurrent investment Casualty loss - flood, earthquake, fire 155 154 Fornet of income stateman O "Functional" income Segement PAS 1, paragraph 90, provides that an entity shall present EXAMPLAR COMPANY in analysis of expenses recognized in profit or loss using a Income StatementProblem 6-2 (IAA) Masay Company provided the following information for 2016: Salca 7,500,000 Inventories - January 1: Raw materials 200,000 Goods in process 240,000 Finished goods 360,000 Inventories . December 31: Raw materials 280.000 Goods in process 170,000 Finished goods 300,000 Purchases 3,000,000 Direct labor 950,000 Indirect labor 250,000 Superintendente 210,000 Light, heat and power 320,000 Rent - factory building 120,000 Repair and maintenance - machinery 50,000 Factory supplies used 110,000 Sales salaries 400,000 Advertising 160,000 Depreciation - store equipment 70,000 Office salaries 150,000 Depreciation - office equipment 40,000 Depreciation - machinery 60,000 Sales returns and allowances 50,000 Interest income 10,000 Gain on sale of equipment 100,000 Delivery expenses 200,000 Accounting and legal fees 150,000 Office expenses 250,000 Earthquake loss 300,000 Gain from expropriation of asset 100,000 Income tax expense 320,000 Required: n. Statement of cost of goods manufactured b. Income statement using the "cost of goods sold" method C. Income statement using the "nature of expense" method GOProblem 6-3 (IAA) Problem 6-4 (IAA) Christian Company provided the following data for the year Ronald Company prepared the following statement for ended December 31, 2016: 2016: Sales 8,000,000 Sales 7,120,000 Sales salaries 520,000 Increase in inventories 380.000 7,500,000 Advertising 120,000 Indirect labor Cost of goods sold: GO0,000 Sundry manufacturing costs 5,300,000 Delivery expense 160,000 Depreciation of factory building 280,000 Freight in 80,000 Freight on purchases 220,000 5,800.000 Depreciation - machinery 50,000 Factory taxes Gross income 1,700,000 130,000 Purchases Other income: 1,600,000 Purchase discounts 20,000 Direct labor 1,480,000 "Interest revenue 160.000 Factory supplies expense 120,000 Total 180,000 Office supplies expense 30,000 Office salaries Other expense: 800,000 Sales returns and allowances 140,000 40.000 Factory superintendente 480.000 Doubtful accounts Operating income 1,740,000 100,000 Administrative expenses 340,000 Factory maintenance 150,000 Selling expenses 200,000 Factory heat, light and power 220,000 200,000 740.000 Income tax expense 170,000 Income tax Net income 1.000,000 Inventory balances at the end of the fiscal period as compared with balances at the beginning of the fiscal period were as Inventories, January 1: Materials 1,120,000 follows: Factory supplies 660,000 Goods in process 360,000 Finished goods 200,000 decrease Finished goods 420.000 2,560,000 Goods in process 90,000 decrease Raw materials 100,000 increase Inventories, December 31:" Materials 1,560,000 Required: Factory supplies 540,000 Goods in process 320,000 Finished goods 520.000 2,940,000 Prepare an income statement for the year ended December 31, 2016 supported by a schedule of cost goods manufactured. Increase in inventories 380,000The sundry manufacturing costs include the following: Materials purchases 1,600,000 Direct labor 2,000,000 Heat, light and power GO0,000 Repairs and maintenance 100,000 Indirect labor 360,000 Other factory overhead 340,000 Factor supplies purchased 300,000 Total sundry manufacturing costs 5,300 000 Required: Prepare an income statement in good form supported by schedule of cost of goods manufactured

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!