Question: answer wuestions a,b,c please answer everything on this paper with full explantions and answer please answer a, b and c dont leave any out 1)

answer wuestions a,b,c

please answer everything on this paper with full explantions and answer please answer a, b and c dont leave any out

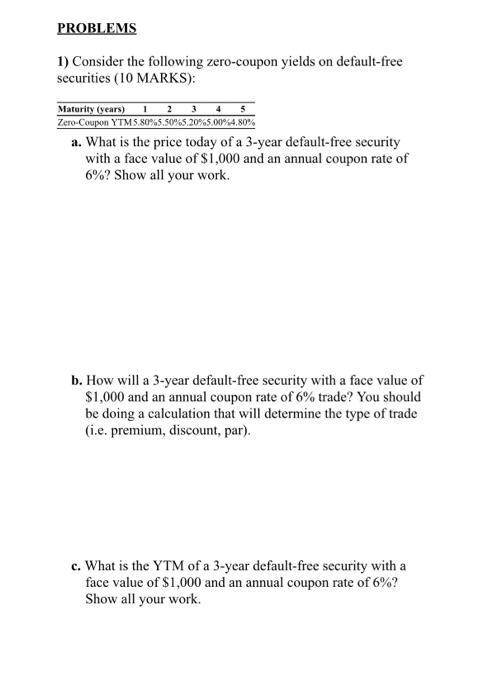

1) Consider the following zero-coupon yields on default-free securities (10 MARKS): a. What is the price today of a 3-year default-free security with a face value of $1,000 and an annual coupon rate of 6% ? Show all your work. b. How will a 3 -year default-free security with a face value of $1,000 and an annual coupon rate of 6% trade? You should be doing a calculation that will determine the type of trade (i.e. premium, discount, par). c. What is the YTM of a 3-year default-free security with a face value of $1,000 and an annual coupon rate of 6% ? Show all your work

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock