Question: Any answers will be artes immediately :) Assignment aims This assignment is designed to consolidate your learning of the key skills and knowledge needed when

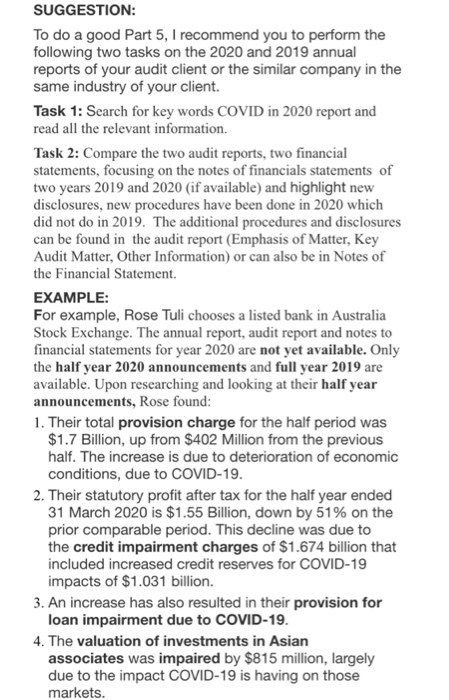

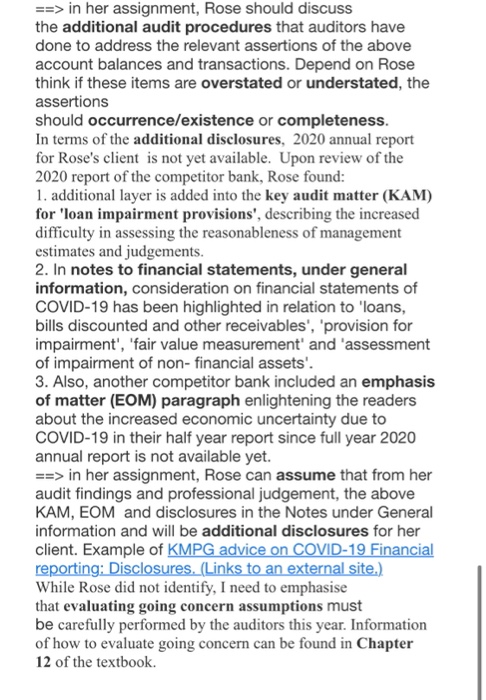

Assignment aims This assignment is designed to consolidate your learning of the key skills and knowledge needed when facing a financial report audit of a company, and how to analyse, research and pinpoint facets of the company that require auditing attention. Background For the purposes of this assignment, you are to imagine that you work as an Audit Manager for a company called Amazing Accountants. Your new audit client is a listed company in Australian Stock Exchange (Accent Group Limited). The client has asked you to perform their financial report audit for the financial year ended 31 December 2020. You will perform your audit for this client in all parts of the assignment. Part 5 Question (minimum 1,000 words) Assume that the global pandemic COVID-19 will cause a material impact to your audit client. What additional audit procedures and disclosures are required in your audit planning and audit opinion. Announcement/an example from the teacher: First, I would like to remind you of the previous Announcement gave you plenty ideas how COVID impact the businesses, what the auditors should do more as additional procedures to identify the risk and the uncertainty caused by COVID-19 to their clients. Second, you can do your google search to find relevant articles discussing the impacts of COVID-19 to different industries by professional bodies and Big Four. For example, one student, Belinda Teffany showed me how she found this interesting and useful article for her client in telecommunication industry (Links to an external site.) from browsing "KPMG COVID-19 Financial reporting resource centre" (Links to an external site, which I provided in my previous Announcement. Please make sure you cite your sources where you learn ideas from. Third, I would like to emphasize that why many businesses are struggling and receiving negative impacts such as lower revenue, higher costs/expenses, higher bad debt etc, there are also many businesses see their businesses growing during COVID-19 lockdown, thus positive impacts can be possible and should be discussed. The additional audit procedures should identify the unexpected changes or the absence of expected changes due to COVID-19. So, for example, for sales revenue, upon your professional judgement, you will need to decide if your additional procedures are to identify if sale revenue is overstated (if you expect it declines but it increases) or understated (if you expect it should be higher but it is lower than your expectation) because of COVID-19. Same procedures for all items that you believe might be impacted due to COVID-19 such as provision for doubtful debts, provision for slow-moving or stock obsolescence write-off etc. Last, I provide you an example of one student, Rose Tuli who have asked me for further guidance and I have guided her to do her assignment as follows.. STRUCTURE 1. The assignment has key words which are highlighted in bold texts Assume that the global pandemic COVID-19 will cause a material impact to your audit client. What additional audit procedures and disclosures are required in your audit planning and audit opinion. So, your assignment should be structured for the following: 1. Explain the impacts of COVID-19 to your audit client (can be either positive, negative or both) 2, Explain the additional procedures in your audit planning, the new audit procedures that you did not do in 2019 audit, but you plan to do in 2020 audit because of COVID-19. 3. Explain after performing the additional audit procedures, what additional disclosures should you include in your audit opinion and your justification (why is it necessary to have these additional disclosures), 4. Formatting: This is a report to your Audit Partner and Audit Client, so make sure you design and format it professionally. You must include all your references in RMIT Harvard style and in alphabetical order. 5. Word counts should be approximately 1000 words. Keep it within this limit. SUGGESTION: To do a good Part 5, I recommend you to perform the following two tasks on the 2020 and 2019 annual reports of your audit client or the similar company in the same industry of your client Task 1: Search for key words COVID in 2020 report and read all the relevant information. Task 2: Compare the two audit reports, two financial statements, focusing on the notes of financials statements of two years 2019 and 2020 (if available) and highlight new disclosures, new procedures have been done in 2020 which did not do in 2019. The additional procedures and disclosures can be found in the audit report (Emphasis of Matter, Key Audit Matter, Other Information) or can also be in Notes of the Financial Statement EXAMPLE: For example, Rose Tuli chooses a listed bank in Australia Stock Exchange. The annual report, audit report and notes to financial statements for year 2020 are not yet available. Only the half year 2020 announcements and full year 2019 are available. Upon researching and looking at their half year announcements, Rose found: 1. Their total provision charge for the half period was $1.7 Billion, up from $402 Million from the previous half. The increase is due to deterioration of economic conditions, due to COVID-19. 2. Their statutory profit after tax for the half year ended 31 March 2020 is $1.55 Billion, down by 51% on the prior comparable period. This decline was due to the credit impairment charges of $1.674 billion that included increased credit reserves for COVID-19 impacts of $1.031 billion. 3. An increase has also resulted in their provision for loan impairment due to COVID-19. 4. The valuation of investments in Asian associates was impaired by $815 million, largely due to the impact COVID-19 is having on those markets. ==> in her assignment, Rose should discuss the additional audit procedures that auditors have done to address the relevant assertions of the above account balances and transactions. Depend on Rose think if these items are overstated or understated, the assertions should occurrence/existence or completeness. In terms of the additional disclosures, 2020 annual report for Rose's client is not yet available. Upon review of the 2020 report of the competitor bank, Rose found: 1. additional layer is added into the key audit matter (KAM) for 'loan impairment provisions', describing the increased difficulty in assessing the reasonableness of management estimates and judgements. 2. In notes to financial statements, under general information, consideration on financial statements of COVID-19 has been highlighted in relation to 'loans, bills discounted and other receivables', 'provision for impairment', 'fair value measurement' and 'assessment of impairment of non-financial assets'. 3. Also, another competitor bank included an emphasis of matter (EOM) paragraph enlightening the readers about the increased economic uncertainty due to COVID-19 in their half year report since full year 2020 annual report is not available yet. ==> in her assignment, Rose can assume that from her audit findings and professional judgement, the above KAM, EOM and disclosures in the Notes under General information and will be additional disclosures for her client. Example of KMPG advice on COVID-19 Financial reporting: Disclosures. (Links to an external site.) While Rose did not identify, I need to emphasise that evaluating going concern assumptions must be carefully performed by the auditors this year. Information of how to evaluate going concern can be found in Chapter 12 of the textbook. Assignment aims This assignment is designed to consolidate your learning of the key skills and knowledge needed when facing a financial report audit of a company, and how to analyse, research and pinpoint facets of the company that require auditing attention. Background For the purposes of this assignment, you are to imagine that you work as an Audit Manager for a company called Amazing Accountants. Your new audit client is a listed company in Australian Stock Exchange (Accent Group Limited). The client has asked you to perform their financial report audit for the financial year ended 31 December 2020. You will perform your audit for this client in all parts of the assignment. Part 5 Question (minimum 1,000 words) Assume that the global pandemic COVID-19 will cause a material impact to your audit client. What additional audit procedures and disclosures are required in your audit planning and audit opinion. Assignment aims This assignment is designed to consolidate your learning of the key skills and knowledge needed when facing a financial report audit of a company, and how to analyse, research and pinpoint facets of the company that require auditing attention. Background For the purposes of this assignment, you are to imagine that you work as an Audit Manager for a company called Amazing Accountants. Your new audit client is a listed company in Australian Stock Exchange (Accent Group Limited). The client has asked you to perform their financial report audit for the financial year ended 31 December 2020. You will perform your audit for this client in all parts of the assignment. Part 5 Question (minimum 1,000 words) Assume that the global pandemic COVID-19 will cause a material impact to your audit client. What additional audit procedures and disclosures are required in your audit planning and audit opinion. Announcement/an example from the teacher: First, I would like to remind you of the previous Announcement gave you plenty ideas how COVID impact the businesses, what the auditors should do more as additional procedures to identify the risk and the uncertainty caused by COVID-19 to their clients. Second, you can do your google search to find relevant articles discussing the impacts of COVID-19 to different industries by professional bodies and Big Four. For example, one student, Belinda Teffany showed me how she found this interesting and useful article for her client in telecommunication industry (Links to an external site.) from browsing "KPMG COVID-19 Financial reporting resource centre" (Links to an external site, which I provided in my previous Announcement. Please make sure you cite your sources where you learn ideas from. Third, I would like to emphasize that why many businesses are struggling and receiving negative impacts such as lower revenue, higher costs/expenses, higher bad debt etc, there are also many businesses see their businesses growing during COVID-19 lockdown, thus positive impacts can be possible and should be discussed. The additional audit procedures should identify the unexpected changes or the absence of expected changes due to COVID-19. So, for example, for sales revenue, upon your professional judgement, you will need to decide if your additional procedures are to identify if sale revenue is overstated (if you expect it declines but it increases) or understated (if you expect it should be higher but it is lower than your expectation) because of COVID-19. Same procedures for all items that you believe might be impacted due to COVID-19 such as provision for doubtful debts, provision for slow-moving or stock obsolescence write-off etc. Last, I provide you an example of one student, Rose Tuli who have asked me for further guidance and I have guided her to do her assignment as follows.. STRUCTURE 1. The assignment has key words which are highlighted in bold texts Assume that the global pandemic COVID-19 will cause a material impact to your audit client. What additional audit procedures and disclosures are required in your audit planning and audit opinion. So, your assignment should be structured for the following: 1. Explain the impacts of COVID-19 to your audit client (can be either positive, negative or both) 2, Explain the additional procedures in your audit planning, the new audit procedures that you did not do in 2019 audit, but you plan to do in 2020 audit because of COVID-19. 3. Explain after performing the additional audit procedures, what additional disclosures should you include in your audit opinion and your justification (why is it necessary to have these additional disclosures), 4. Formatting: This is a report to your Audit Partner and Audit Client, so make sure you design and format it professionally. You must include all your references in RMIT Harvard style and in alphabetical order. 5. Word counts should be approximately 1000 words. Keep it within this limit. SUGGESTION: To do a good Part 5, I recommend you to perform the following two tasks on the 2020 and 2019 annual reports of your audit client or the similar company in the same industry of your client Task 1: Search for key words COVID in 2020 report and read all the relevant information. Task 2: Compare the two audit reports, two financial statements, focusing on the notes of financials statements of two years 2019 and 2020 (if available) and highlight new disclosures, new procedures have been done in 2020 which did not do in 2019. The additional procedures and disclosures can be found in the audit report (Emphasis of Matter, Key Audit Matter, Other Information) or can also be in Notes of the Financial Statement EXAMPLE: For example, Rose Tuli chooses a listed bank in Australia Stock Exchange. The annual report, audit report and notes to financial statements for year 2020 are not yet available. Only the half year 2020 announcements and full year 2019 are available. Upon researching and looking at their half year announcements, Rose found: 1. Their total provision charge for the half period was $1.7 Billion, up from $402 Million from the previous half. The increase is due to deterioration of economic conditions, due to COVID-19. 2. Their statutory profit after tax for the half year ended 31 March 2020 is $1.55 Billion, down by 51% on the prior comparable period. This decline was due to the credit impairment charges of $1.674 billion that included increased credit reserves for COVID-19 impacts of $1.031 billion. 3. An increase has also resulted in their provision for loan impairment due to COVID-19. 4. The valuation of investments in Asian associates was impaired by $815 million, largely due to the impact COVID-19 is having on those markets. ==> in her assignment, Rose should discuss the additional audit procedures that auditors have done to address the relevant assertions of the above account balances and transactions. Depend on Rose think if these items are overstated or understated, the assertions should occurrence/existence or completeness. In terms of the additional disclosures, 2020 annual report for Rose's client is not yet available. Upon review of the 2020 report of the competitor bank, Rose found: 1. additional layer is added into the key audit matter (KAM) for 'loan impairment provisions', describing the increased difficulty in assessing the reasonableness of management estimates and judgements. 2. In notes to financial statements, under general information, consideration on financial statements of COVID-19 has been highlighted in relation to 'loans, bills discounted and other receivables', 'provision for impairment', 'fair value measurement' and 'assessment of impairment of non-financial assets'. 3. Also, another competitor bank included an emphasis of matter (EOM) paragraph enlightening the readers about the increased economic uncertainty due to COVID-19 in their half year report since full year 2020 annual report is not available yet. ==> in her assignment, Rose can assume that from her audit findings and professional judgement, the above KAM, EOM and disclosures in the Notes under General information and will be additional disclosures for her client. Example of KMPG advice on COVID-19 Financial reporting: Disclosures. (Links to an external site.) While Rose did not identify, I need to emphasise that evaluating going concern assumptions must be carefully performed by the auditors this year. Information of how to evaluate going concern can be found in Chapter 12 of the textbook. Assignment aims This assignment is designed to consolidate your learning of the key skills and knowledge needed when facing a financial report audit of a company, and how to analyse, research and pinpoint facets of the company that require auditing attention. Background For the purposes of this assignment, you are to imagine that you work as an Audit Manager for a company called Amazing Accountants. Your new audit client is a listed company in Australian Stock Exchange (Accent Group Limited). The client has asked you to perform their financial report audit for the financial year ended 31 December 2020. You will perform your audit for this client in all parts of the assignment. Part 5 Question (minimum 1,000 words) Assume that the global pandemic COVID-19 will cause a material impact to your audit client. What additional audit procedures and disclosures are required in your audit planning and audit opinion

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts