Question: ANY CODE NEEDS TO BE IN R PLEASE Question 3 Portfolio Management Suppose we have N stocks whose future prices follow a simple binomial model.

ANY CODE NEEDS TO BE IN R PLEASE

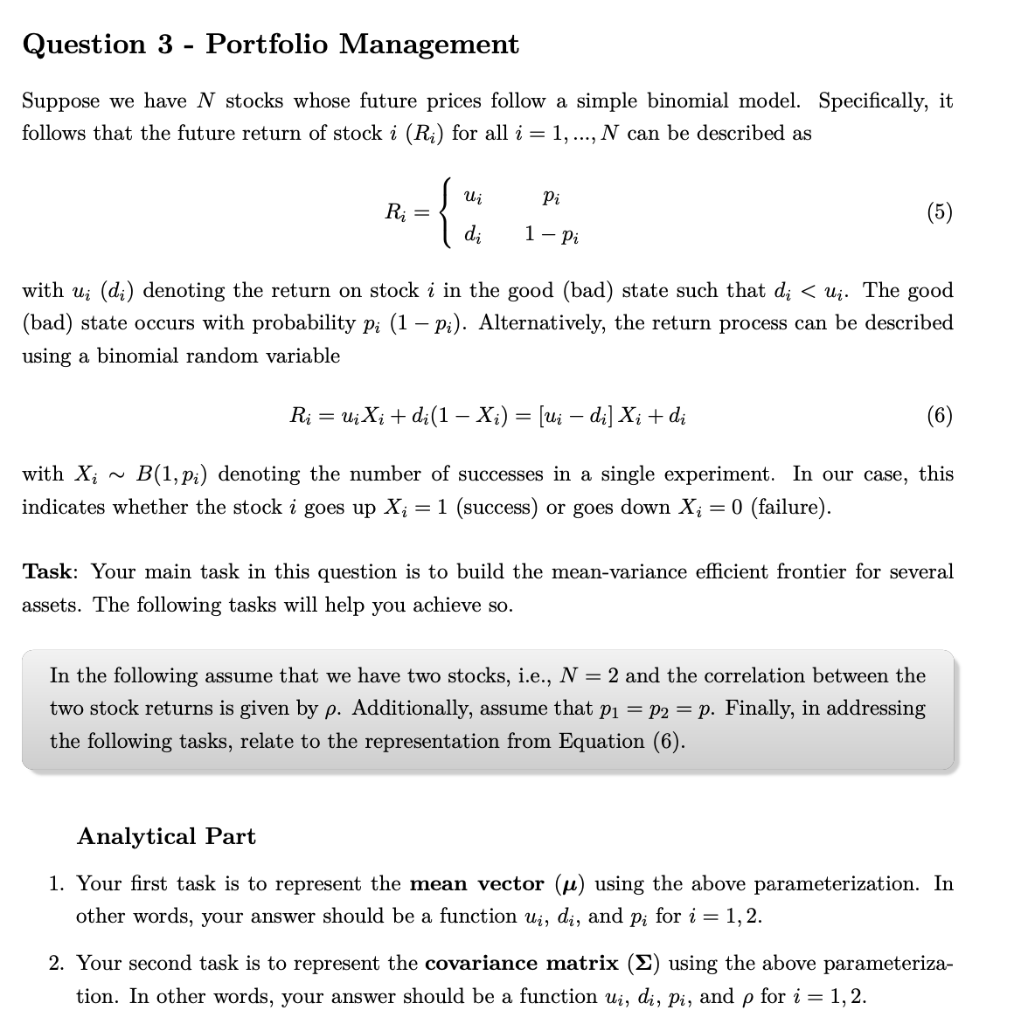

Question 3 Portfolio Management Suppose we have N stocks whose future prices follow a simple binomial model. Specifically, it follows that the future return of stock i (Ri) for all i = 1, ..., N can be described as 9 ui Pi Ri { (5) di 1- Pi with w; (di) denoting the return on stock i in the good (bad) state such that di

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock