Question: Apparently, all the answers in the boxes are all wrong, need help on all the boxes. Yoko Iwabuchi is the controller of Kondo, Inc., an

Apparently, all the answers in the boxes are all wrong, need help on all the boxes.

Apparently, all the answers in the boxes are all wrong, need help on all the boxes.

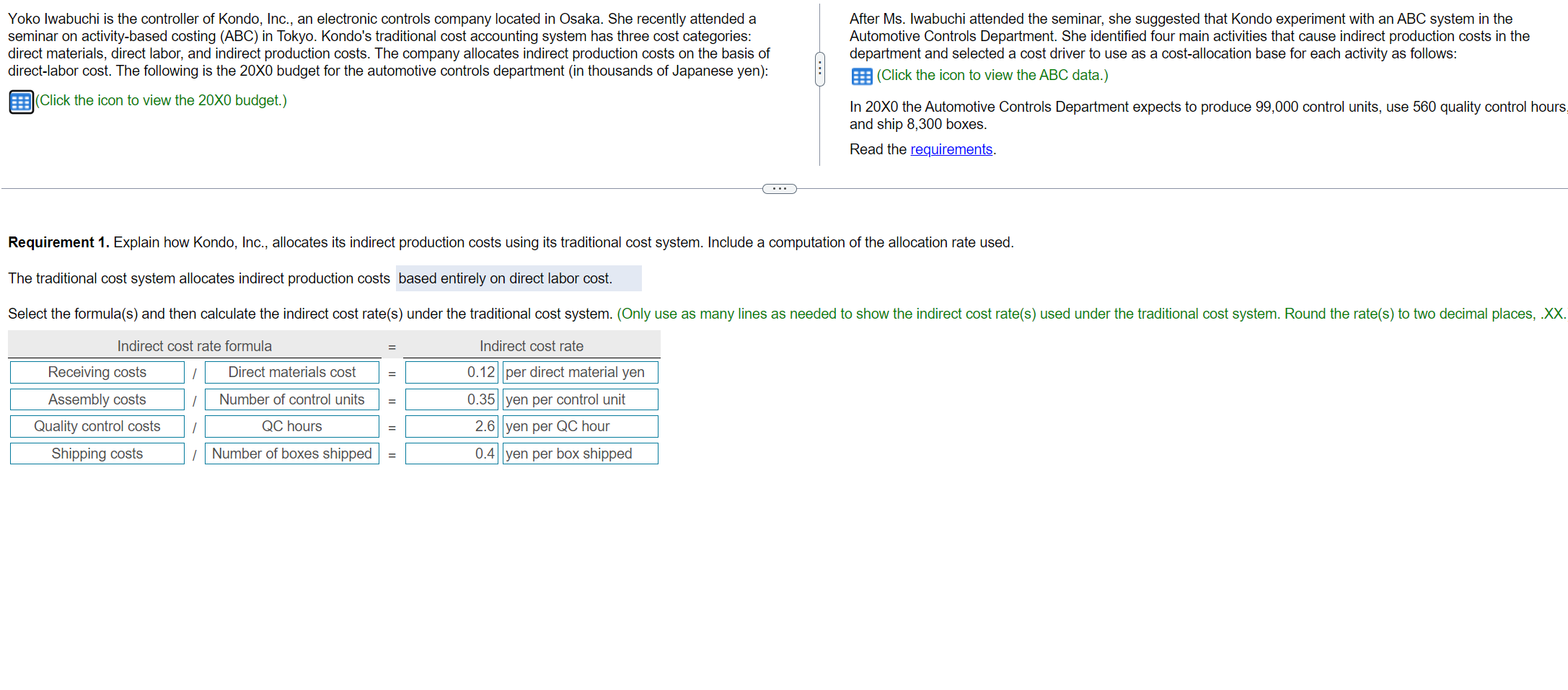

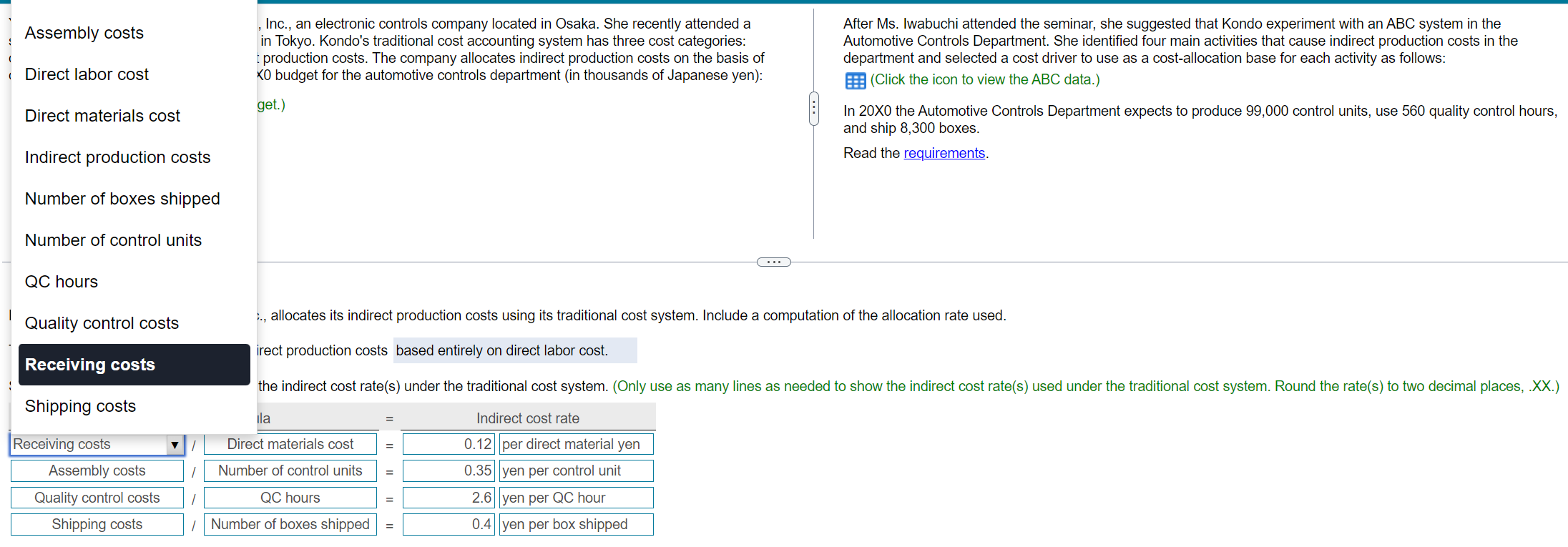

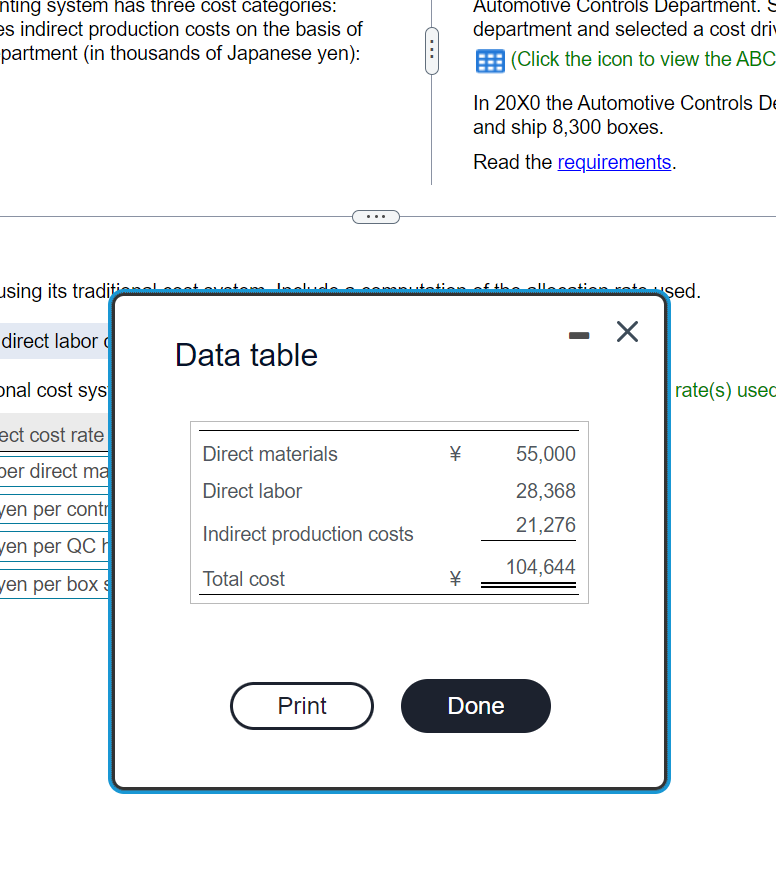

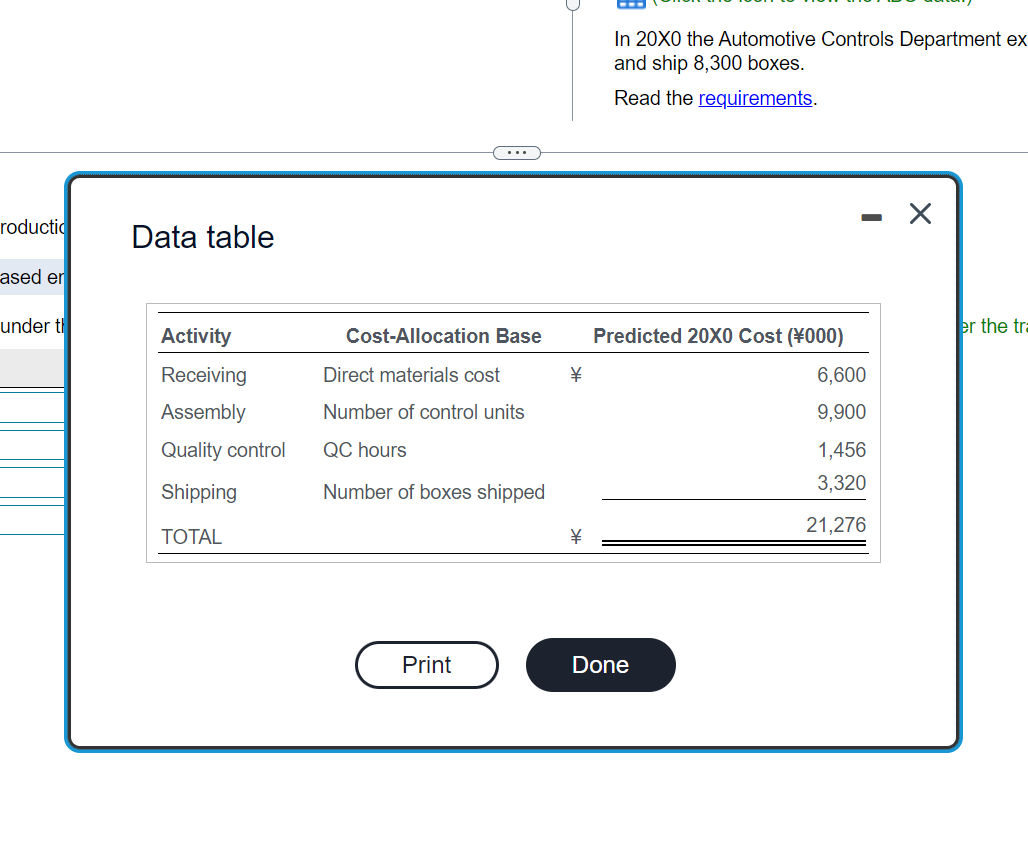

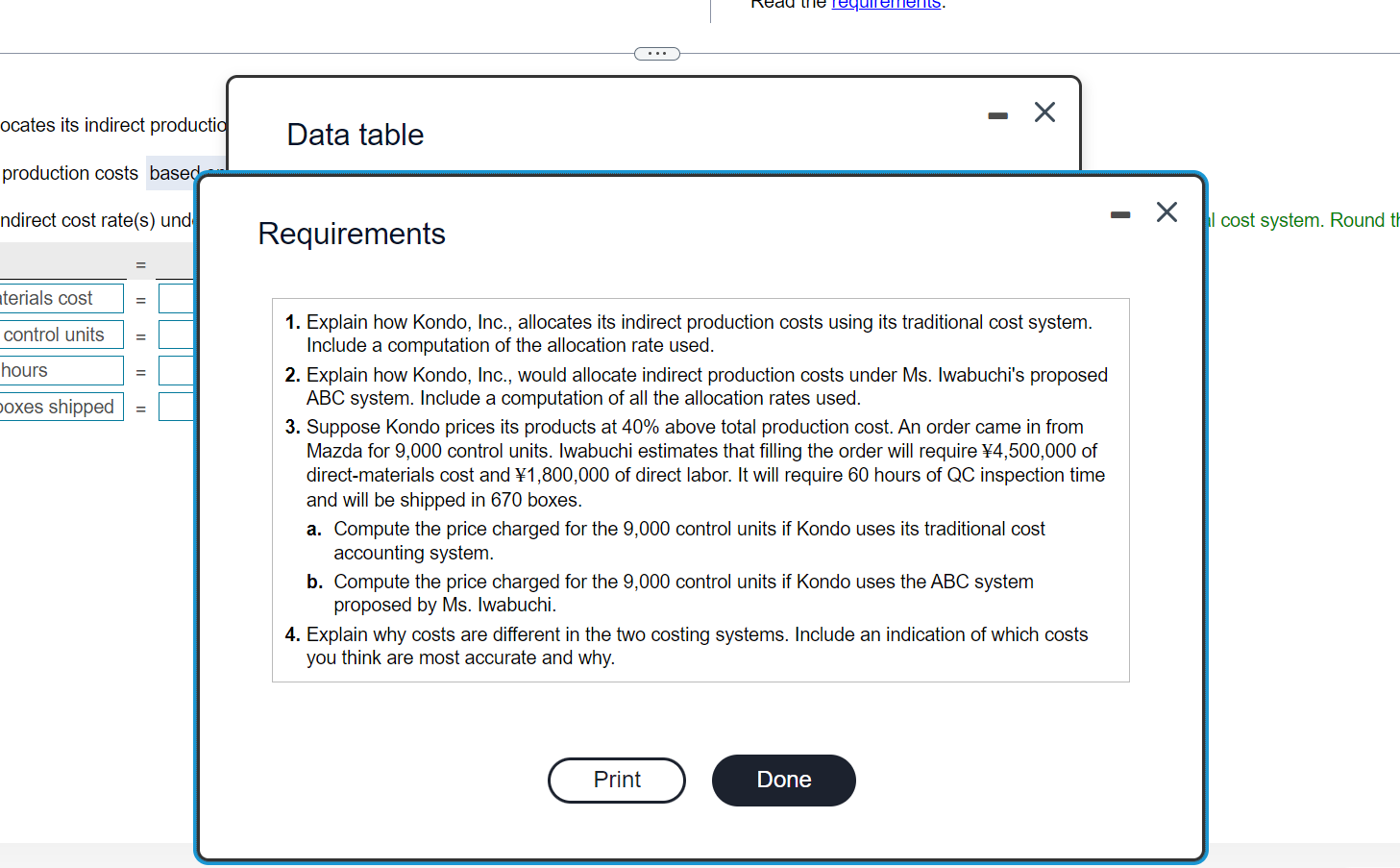

Yoko Iwabuchi is the controller of Kondo, Inc., an electronic controls company located in Osaka. She recently attended a seminar on activity-based costing (ABC) in Tokyo. Kondo's traditional cost accounting system has three cost categories: direct materials, direct labor, and indirect production costs. The company allocates indirect production costs on the basis of direct-labor cost. The following is the 20X0 budget for the automotive controls department (in thousands of Japanese yen): Click the icon to view the 20X0 budget.) After Ms. Iwabuchi attended the seminar, she suggested that Kondo experiment with an ABC system in the Automotive Controls Department. She identified four main activities that cause indirect production costs in the department and selected a cost driver to use as a cost-allocation base for each activity as follows: (Click the icon to view the ABC data.) In 20X0 the Automotive Controls Department expects to produce 99,000 control units, use 560 quality control hours, and ship 8,300 boxes. Read the requirements. Requirement 1. Explain how Kondo, Inc., allocates its indirect production costs using its traditional cost system. Include a computation of the allocation rate used. The traditional cost system allocates indirect production costs based entirely on direct labor cost. Select the formula(s) and then calculate the indirect cost rate(s) under the traditional cost system. (Only use as many lines as needed to show the indirect cost rate(s) used under the traditional cost system. Round the rate(s) to two decimal places, .XX. Indirect cost rate formula Indirect cost rate Direct materials cost Number of control units Receiving costs Assembly costs Quality control costs Shipping costs 0.12 per direct material yen 0.35 yen per control unit 2.6|yen per QC hour 0.4 yen per box shipped / QC hours = Number of boxes shipped Assembly costs , Inc., an electronic controls company located in Osaka. She recently attended a in Tokyo. Kondo's traditional cost accounting system has three cost categories: production costs. The company allocates indirect production costs on the basis of KO budget for the automotive controls department in thousands of Japanese yen): After Ms. Iwabuchi attended the seminar, she suggested that Kondo experiment with an ABC system in the Automotive Controls Department. She identified four main activities that cause indirect production costs in the department and selected a cost driver to use as a cost-allocation base for each activity as follows: (Click the icon to view the ABC data.) Direct labor cost get.) . Direct materials cost In 20X0 the Automotive Controls Department expects to produce 99,000 control units, use 560 quality control hours, and ship 8,300 boxes. Read the requirements. Indirect production costs Number of boxes shipped Number of control units QC hours -, allocates its indirect production costs using its traditional cost system. Include a computation of the allocation rate used. Quality control costs irect production costs based entirely on direct labor cost. Receiving costs the indirect cost rate(s) under the traditional cost system. (Only use as many lines as needed to show the indirect cost rate(s) used under the traditional cost system. Round the rate(s) to two decimal places, XX.) Shipping costs ila Indirect cost rate Direct materials cost 0.12 per direct material yen Receiving costs Assembly costs Quality control costs Number of control units 0.35 yen per control unit / QC hours 2.6 yen per QC hour Shipping costs Number of boxes shipped = 0.4 yen per box shipped nting system has three cost categories: es indirect production costs on the basis of partment (in thousands of Japanese yen): Automotive Controls Department. department and selected a cost dri E: (Click the icon to view the ABC In 20X0 the Automotive Controls De and ship 8,300 boxes. Read the requirements. using its traditional cost otom od mutation of the cloention to used. - direct labore - Data table onal cost sys rate(s) used ect cost rate per direct ma Direct materials 55,000 Direct labor Jen per contr Jen per QCH 28,368 21,276 Indirect production costs 104,644 en per box Total cost V Print Done In 20X0 the Automotive Controls Department ex and ship 8,300 boxes. Read the requirements. roductic Data table ased er under tt er the tr Cost-Allocation Base Predicted 20X0 Cost (\000) Direct materials cost 6,600 Activity Receiving Assembly Quality control Number of control units 9,900 QC hours 1,456 3,320 Shipping Number of boxes shipped 21,276 TOTAL Print Done Tedule Tequiemens. - ocates its indirect productia Data table production costs based ndirect cost rate(s) und -X cost system. Round th Requirements aterials cost control units hours boxes shipped 1. Explain how Kondo, Inc., allocates its indirect production costs using its traditional cost system. Include a computation of the allocation rate used. 2. Explain how Kondo, Inc., would allocate indirect production costs under Ms. Iwabuchi's proposed ABC system. Include a computation of all the allocation rates used. 3. Suppose Kondo prices its products at 40% above total production cost. An order came in from Mazda for 9,000 control units. Iwabuchi estimates that filling the order will require 4,500,000 of direct-materials cost and 1,800,000 of direct labor. It will require 60 hours of QC inspection time and will be shipped in 670 boxes. a. Compute the price charged for the 9,000 control units if Kondo uses its traditional cost accounting system. b. Compute the price charged for the 9,000 control units if Kondo uses the ABC system proposed by Ms. Iwabuchi. 4. Explain why costs are different in the two costing systems. Include an indication of which costs you think are most accurate and why. Print Done

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts