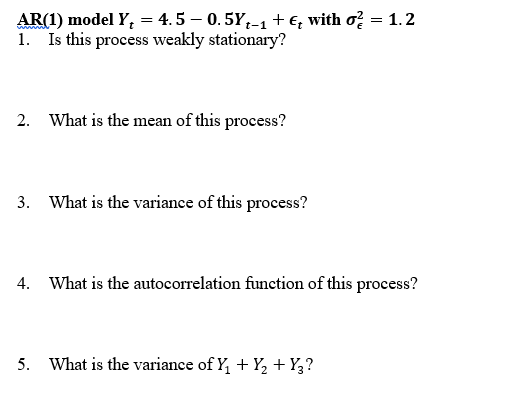

Question: AR ( 1 ) model ) 4.5 - 0.58 2 1 + E , with of = 1.2 1 . Is this process weakly stationary

AR ( 1 ) model ) 4.5 - 0.58 2 1 + E , with of = 1.2 1 . Is this process weakly stationary ? What is the mean of this process ? 3 . What is the variance of this process ? What is the autocorrelation function of this process ? 5 . What is the variance of Y , + 8 2 + Y's

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock