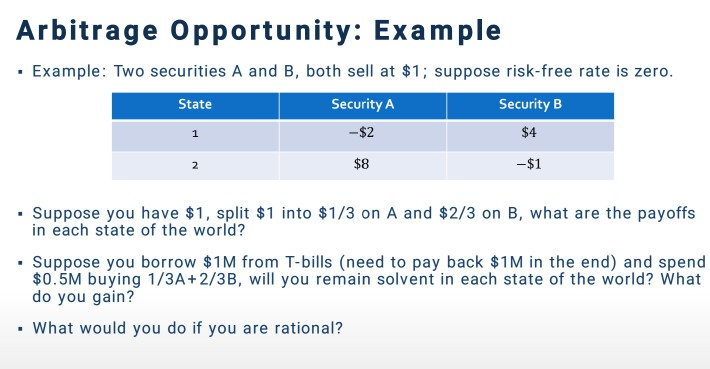

Question: Arbitrage Opportunity: Example Example: Two securities A and B, both sell at $1; suppose risk-free rate is zero. State Security B Security A -$2 1

Arbitrage Opportunity: Example Example: Two securities A and B, both sell at $1; suppose risk-free rate is zero. State Security B Security A -$2 1 $8 -$1 . Suppose you have $1, split $1 into $1/3 on A and $2/3 on B, what are the payoffs in each state of the world? Suppose you borrow $1M from T-bills (need to pay back $1M in the end) and spend $0.5M buying 1/3A +2/3B, will you remain solvent in each state of the world? What do you gain? . What would you do if you are rational

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock