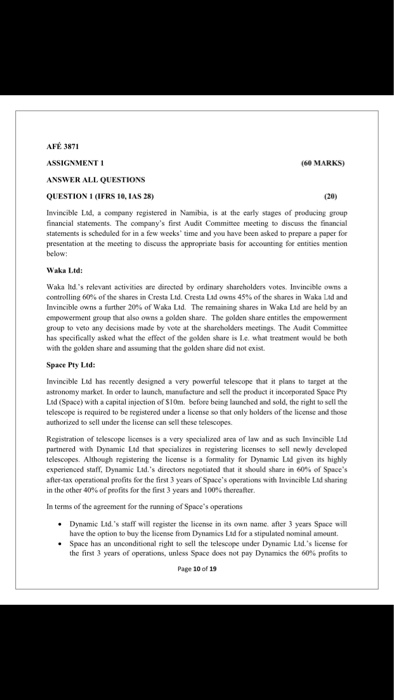

Question: ARE 1871 ASSIGNMENTI MARKS) ANSWER ALL QUESTIONS QUESTION I CIFRS 10, LAS 25) (20) Invincible Lada copy registered in his is at the early stages

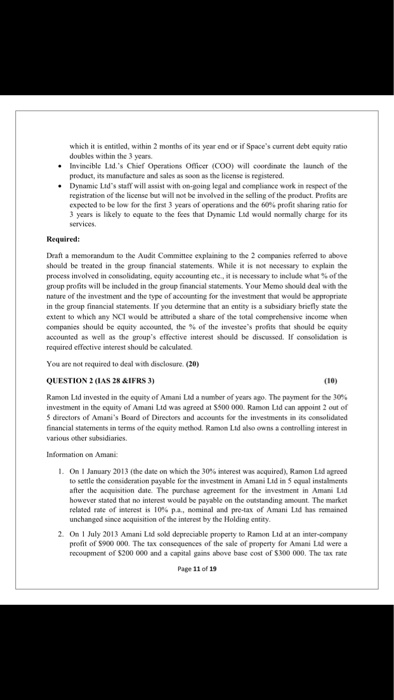

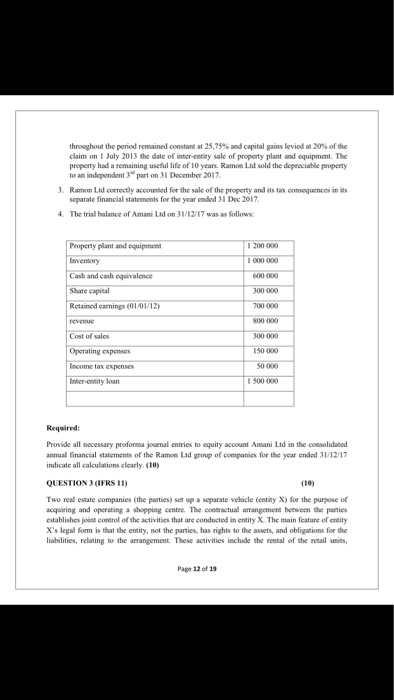

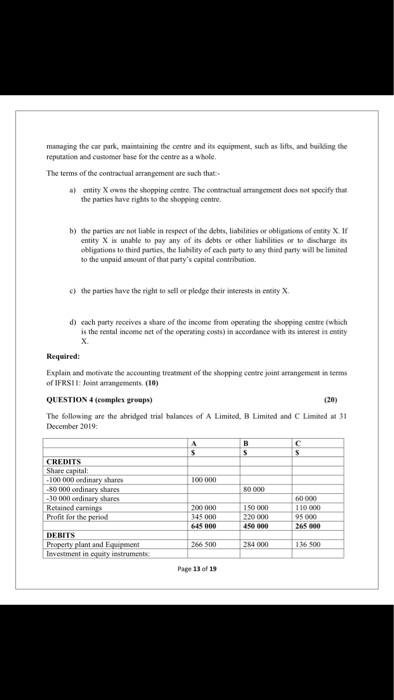

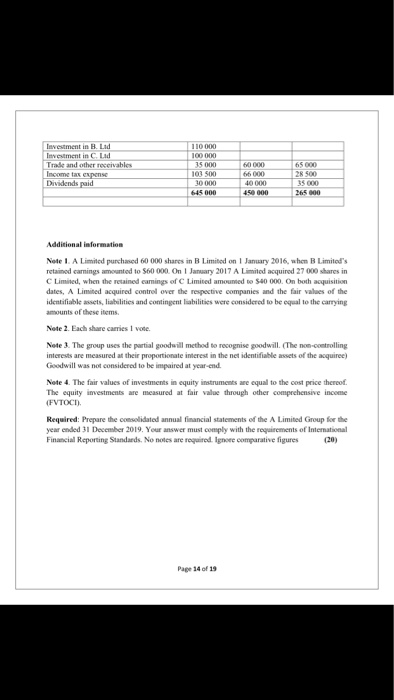

ARE 1871 ASSIGNMENTI MARKS) ANSWER ALL QUESTIONS QUESTION I CIFRS 10, LAS 25) (20) Invincible Lada copy registered in his is at the early stages of producing group financial statements. The company's first Audit Committee meeting to discuss the financial statements is scheduled for in a few weeks time and you have been asked to prepare a perfor presentation at the meeting to discuss the appropriate basis for conting for entities mention hellow Waka Laid: Wala Ind's relevant activities are directed by ordinary shareholders votes Invincible una controlling of the shares in Cresta Lad Crest Lans 45% of the shares in Wakaland Invincible owns a further 20% of Waka Lad. The remaining shares in Waka Lad we held by an cmpowerment group that also owns a golden share. The poden she entities the empowerment group to voto any decisions made by one at the shareholders meetings. The Audit Committee has specifically asked what the effect of the golden share is de what treatment would be both with the golden share and suming that the golden share did not exist Spare PyLad: Invincible d has recently designed a very powerful telescope that it plans to target at the astronomy marketIn order to launch ma ture and sell the product it incorporated Space Ply LdSpace with a capital injection of S10m. before being launched sold the right to sell the Telescope is required to be registered under a license so that only holders of the license and these authorized to sell under the license can sell these telescopes Registration of telescope license is a very specialised area of law and such Invincible Led partnered with Dynamic Led that specializes in registering licenses to sell newly developed Telescopes. Although registering the license is a formality for Dynamic UN given its highly experienced stall. Dynamic Lad's director a ted that it would shares of Space's afera e profits for the first 3 years of Space's operation with Invincible sharing in the other profits for the first years and 100 thereafter sensor the agreement for the n ing of Space's operaties Dynamic Lad staff will register the license in its n ame after 3 years Space will have the option by the licero D o ra stipulated Space has conditional right to sell the telescope under Dynamic L i me for the first years of ro les Space does not pay D iether Page 1 of 1 which is titled with this w i f Space's debti doubles within the 3 years micile Chief Open Officer (COD) l e thed of the products manufacture and sales as soon as the license is registered Dynamic staff will with poing legal and compliance w i pect of the registration of the license but will not be involved in the selling of the product. Prise expected to below for the first years of operis and the profitaring for 3 years is likely to u se the fees that Dynamic Edwudmally charge for its Required: Draft a memorandum to the Audit Committee explaining to the 2 panies referred to whose should be treated in the group financial statements. While it is not necessary to explain the process involved in consolidating equity counting is necessary to include what of the group profits will be included in the group financial statements. Your Meme should deal with the nature of the investment and the type of accounting for the investment that would be appropriate in the group financial statements. If you determine that an entity is a subsidiary briefly state the extent to which an NCI would be attributed a share of the total comprehensive income when companies should be equity accounted the or the investee's profits that should be equity accounted as well as the group's effective interest should be discussed. I m idation required effective interest should the calculated You are not required to deal with disclosure (20) (10) R QUESTION 2 (IAS 28 &IFRS 3) en Lid invested in the equity of Amani Na umber of The payment for the to investment in the equity of Amani Lid was agreed at 5500 000 Ramon Lld can appoint out of S directors of Amani's Beard of Directors and cons for the investments in its consolidated financial statements in rms of the equity method Ram L a w n interest in various other subsidiaries Information Aman 1 On 1 January 2013 (the date on which the 30 interest was acquired. Ramon L ared to see the consideration payable for the investment in Am o ualisten after the squisition date. The purchase agrement for the vestment in Am d however stated that no interest w e pay on the outstanding out the market drie oft 10% pa p er of Aman harmained unchanged since acquisition of the interest by the Holding my 2 O 1 July 2013 Amani Lad sold depreciable property to Ramon Lda profit of S 00 The of the sale of paperty for Amt 200 000 a capital gains above the cost of The were Throughout the period remained constatat 25.75% and capitalis levied w h e claim 1 July 2013 the date of e ntity sale of property plant and equipment. The property had a remi s e of 10 years Ram sold the deceaparty to an independent part 31 December 2017 Ramon La correctly acid for the sale of the property and its ac c ess separate financial statements for the year ended 31 Dec 2017 4. The trial balance of Amani Lad on 31/12/17 was as follows Property plant and equipment 1 200 000 Cash and cash equivalence Share capital Retained earnings (01/01/12) 1 000 000 500 000 300 000 700 000 800 000 300 000 150 000 Cost of sales Operating expenses Income tax expenses Intermity loan 1 500 000 Required: Provide all necessary proforma jumal entries to quity cont Amani Led in the consolidated annual financial statements of the Ramon Lad group of companies for the year ended 31/12/17 indicate all calculations clearly (10) QUESTION (IFRS ID 10 Two real estate companies the presset up a separate vehicle ty X) for the purpose of qigand i ng a shopping centre. The contractual m e here the parties establishes of the activities that are conducted in city X Them e X's legal form is that the city of the pure has the sand for the es relating the w oment These activities include the most of the metal et sch u ing the maging the cuking the credits and hase for the cosa whole The terms of the contractual ampement are such that a) city Xown the shopping centre. The contractual arrangement does not specify that the parties have to the shopping centre b) the parties are not liable in respect of the debts, liabilities or obligations of entity X. entity X is unable to pay any of its debts or other abilities to discharges chigations to third parties, the ability of each party to any third party will be limited to the unpaid amount of that party's capital contribution c) the parties have the right to sell or pledge their interests in entity X d) each party recives a share of the income from operating the shopping centre (which is the rental income net of the operating costs) in accordance with its interest in city Required: Explain and motivate the accounting treatment of the shopping centre joint arrangement in terms of IFRSIT:Jo ngens (10) QUESTION 4 (complex groups) The following are the abridged trial balances of A Limited, B Limited and C Limited 31 December 2019: CREDITS Share capital - 100 000 dinary shares 30 000 shares aninary shares Redwing Pro for the ad J DEBITS h ty and Equipment Page 13 of 19 Additional information Note A Limited purchased 60 000 shares in Limited on January 2016, when Limited retained camningsmusted to On Jury 2017 A mited squired 27 000 hores in C Limited, when the retained camnings of Limited amoumed to 500 000. On both quisiti dates, A Limited acquired control over the respective companies and the fair values of the identifiable assets, liabilities and contingent liabilities were considered to be equal to the carrying amounts of these items Note 2. Each share carries 1 vote. Note 3 The group uses the partial goodwill method to recognise poodwill. The controlling interests are measured at their proportionale interest in the net identifiable sets of the acquiree) Codwill was not considered to be impaired at year-end. Note 4. The fair values of investments in equity instruments are equal to the cost price thereof The equity investments are measured at fair value through other comprehensive income FVTOCH. Required: Prepare the consolidated annual financial statements of the A Limited Group for the year ended 31 December 2019. You wer must comply with the requirements of International Financial Reporting Standards. No notes are required. Ignore comparative figures Page 14 of 19 ARE 1871 ASSIGNMENTI MARKS) ANSWER ALL QUESTIONS QUESTION I CIFRS 10, LAS 25) (20) Invincible Lada copy registered in his is at the early stages of producing group financial statements. The company's first Audit Committee meeting to discuss the financial statements is scheduled for in a few weeks time and you have been asked to prepare a perfor presentation at the meeting to discuss the appropriate basis for conting for entities mention hellow Waka Laid: Wala Ind's relevant activities are directed by ordinary shareholders votes Invincible una controlling of the shares in Cresta Lad Crest Lans 45% of the shares in Wakaland Invincible owns a further 20% of Waka Lad. The remaining shares in Waka Lad we held by an cmpowerment group that also owns a golden share. The poden she entities the empowerment group to voto any decisions made by one at the shareholders meetings. The Audit Committee has specifically asked what the effect of the golden share is de what treatment would be both with the golden share and suming that the golden share did not exist Spare PyLad: Invincible d has recently designed a very powerful telescope that it plans to target at the astronomy marketIn order to launch ma ture and sell the product it incorporated Space Ply LdSpace with a capital injection of S10m. before being launched sold the right to sell the Telescope is required to be registered under a license so that only holders of the license and these authorized to sell under the license can sell these telescopes Registration of telescope license is a very specialised area of law and such Invincible Led partnered with Dynamic Led that specializes in registering licenses to sell newly developed Telescopes. Although registering the license is a formality for Dynamic UN given its highly experienced stall. Dynamic Lad's director a ted that it would shares of Space's afera e profits for the first 3 years of Space's operation with Invincible sharing in the other profits for the first years and 100 thereafter sensor the agreement for the n ing of Space's operaties Dynamic Lad staff will register the license in its n ame after 3 years Space will have the option by the licero D o ra stipulated Space has conditional right to sell the telescope under Dynamic L i me for the first years of ro les Space does not pay D iether Page 1 of 1 which is titled with this w i f Space's debti doubles within the 3 years micile Chief Open Officer (COD) l e thed of the products manufacture and sales as soon as the license is registered Dynamic staff will with poing legal and compliance w i pect of the registration of the license but will not be involved in the selling of the product. Prise expected to below for the first years of operis and the profitaring for 3 years is likely to u se the fees that Dynamic Edwudmally charge for its Required: Draft a memorandum to the Audit Committee explaining to the 2 panies referred to whose should be treated in the group financial statements. While it is not necessary to explain the process involved in consolidating equity counting is necessary to include what of the group profits will be included in the group financial statements. Your Meme should deal with the nature of the investment and the type of accounting for the investment that would be appropriate in the group financial statements. If you determine that an entity is a subsidiary briefly state the extent to which an NCI would be attributed a share of the total comprehensive income when companies should be equity accounted the or the investee's profits that should be equity accounted as well as the group's effective interest should be discussed. I m idation required effective interest should the calculated You are not required to deal with disclosure (20) (10) R QUESTION 2 (IAS 28 &IFRS 3) en Lid invested in the equity of Amani Na umber of The payment for the to investment in the equity of Amani Lid was agreed at 5500 000 Ramon Lld can appoint out of S directors of Amani's Beard of Directors and cons for the investments in its consolidated financial statements in rms of the equity method Ram L a w n interest in various other subsidiaries Information Aman 1 On 1 January 2013 (the date on which the 30 interest was acquired. Ramon L ared to see the consideration payable for the investment in Am o ualisten after the squisition date. The purchase agrement for the vestment in Am d however stated that no interest w e pay on the outstanding out the market drie oft 10% pa p er of Aman harmained unchanged since acquisition of the interest by the Holding my 2 O 1 July 2013 Amani Lad sold depreciable property to Ramon Lda profit of S 00 The of the sale of paperty for Amt 200 000 a capital gains above the cost of The were Throughout the period remained constatat 25.75% and capitalis levied w h e claim 1 July 2013 the date of e ntity sale of property plant and equipment. The property had a remi s e of 10 years Ram sold the deceaparty to an independent part 31 December 2017 Ramon La correctly acid for the sale of the property and its ac c ess separate financial statements for the year ended 31 Dec 2017 4. The trial balance of Amani Lad on 31/12/17 was as follows Property plant and equipment 1 200 000 Cash and cash equivalence Share capital Retained earnings (01/01/12) 1 000 000 500 000 300 000 700 000 800 000 300 000 150 000 Cost of sales Operating expenses Income tax expenses Intermity loan 1 500 000 Required: Provide all necessary proforma jumal entries to quity cont Amani Led in the consolidated annual financial statements of the Ramon Lad group of companies for the year ended 31/12/17 indicate all calculations clearly (10) QUESTION (IFRS ID 10 Two real estate companies the presset up a separate vehicle ty X) for the purpose of qigand i ng a shopping centre. The contractual m e here the parties establishes of the activities that are conducted in city X Them e X's legal form is that the city of the pure has the sand for the es relating the w oment These activities include the most of the metal et sch u ing the maging the cuking the credits and hase for the cosa whole The terms of the contractual ampement are such that a) city Xown the shopping centre. The contractual arrangement does not specify that the parties have to the shopping centre b) the parties are not liable in respect of the debts, liabilities or obligations of entity X. entity X is unable to pay any of its debts or other abilities to discharges chigations to third parties, the ability of each party to any third party will be limited to the unpaid amount of that party's capital contribution c) the parties have the right to sell or pledge their interests in entity X d) each party recives a share of the income from operating the shopping centre (which is the rental income net of the operating costs) in accordance with its interest in city Required: Explain and motivate the accounting treatment of the shopping centre joint arrangement in terms of IFRSIT:Jo ngens (10) QUESTION 4 (complex groups) The following are the abridged trial balances of A Limited, B Limited and C Limited 31 December 2019: CREDITS Share capital - 100 000 dinary shares 30 000 shares aninary shares Redwing Pro for the ad J DEBITS h ty and Equipment Page 13 of 19 Additional information Note A Limited purchased 60 000 shares in Limited on January 2016, when Limited retained camningsmusted to On Jury 2017 A mited squired 27 000 hores in C Limited, when the retained camnings of Limited amoumed to 500 000. On both quisiti dates, A Limited acquired control over the respective companies and the fair values of the identifiable assets, liabilities and contingent liabilities were considered to be equal to the carrying amounts of these items Note 2. Each share carries 1 vote. Note 3 The group uses the partial goodwill method to recognise poodwill. The controlling interests are measured at their proportionale interest in the net identifiable sets of the acquiree) Codwill was not considered to be impaired at year-end. Note 4. The fair values of investments in equity instruments are equal to the cost price thereof The equity investments are measured at fair value through other comprehensive income FVTOCH. Required: Prepare the consolidated annual financial statements of the A Limited Group for the year ended 31 December 2019. You wer must comply with the requirements of International Financial Reporting Standards. No notes are required. Ignore comparative figures Page 14 of 19

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts