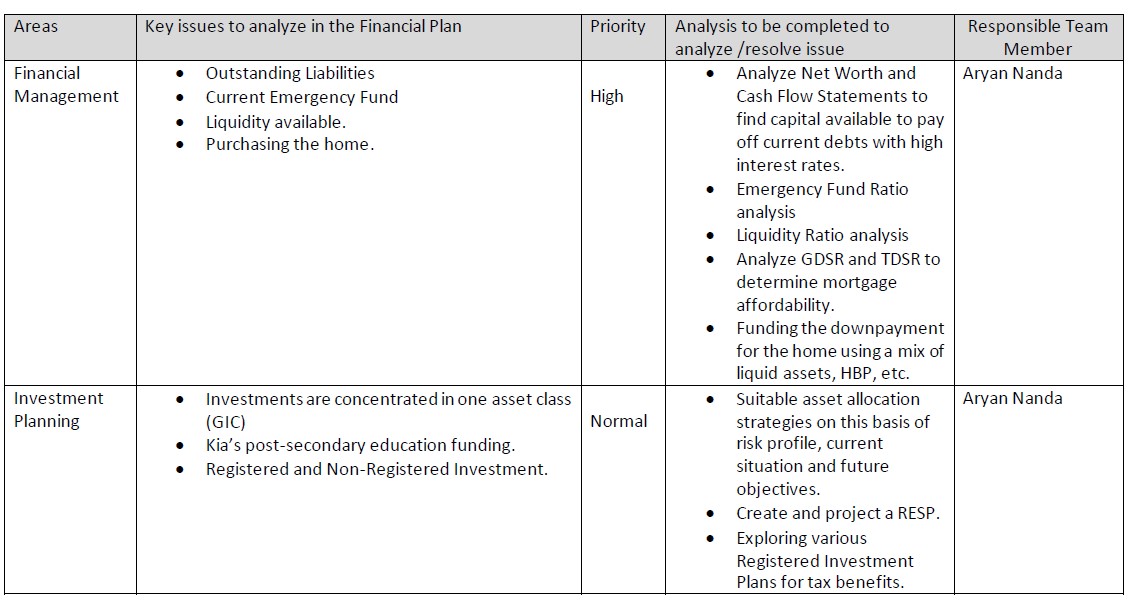

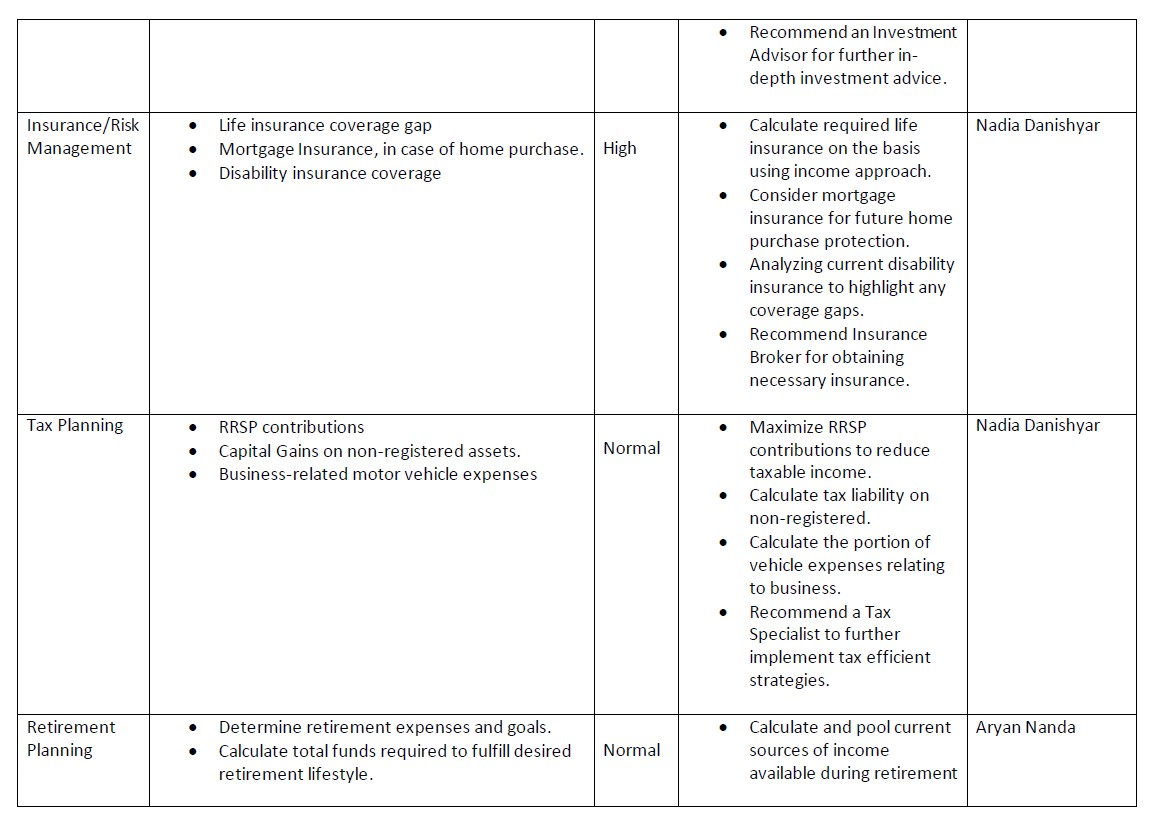

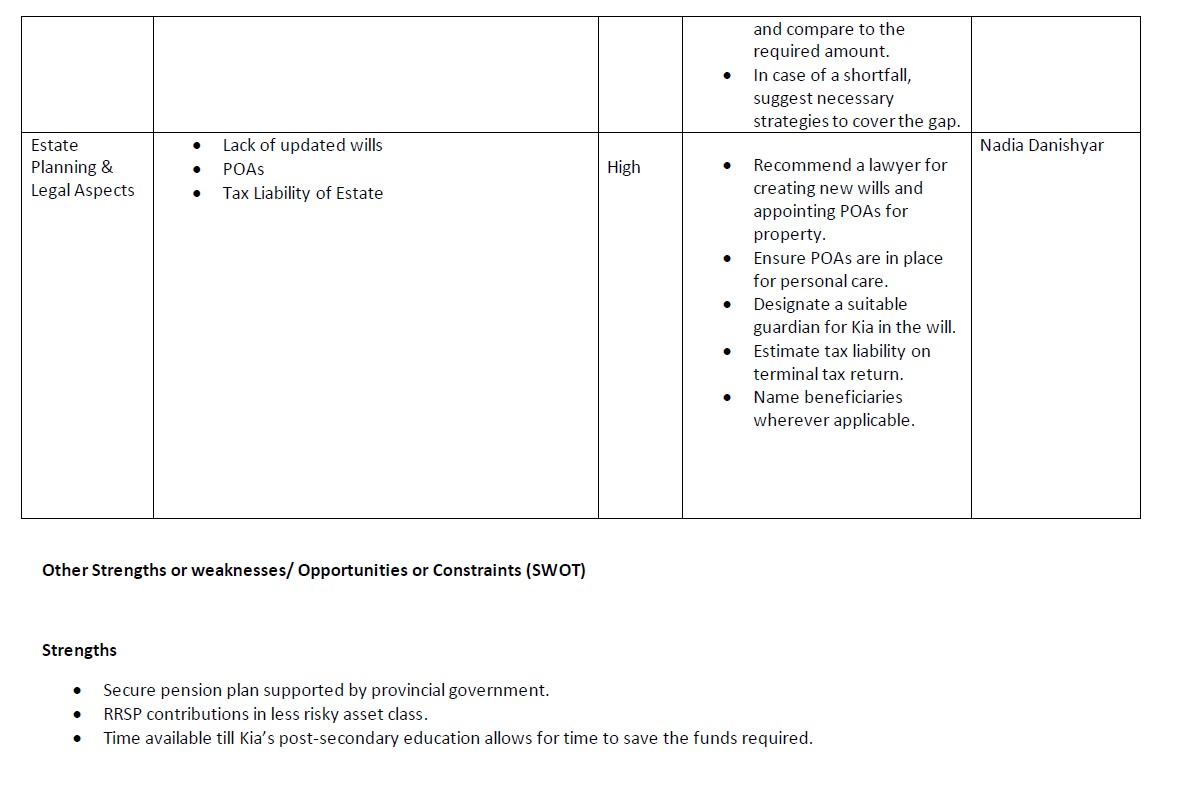

Question: Areas Key issues to analyze in the Financial Plan Priority Analysis to be completed to Responsible Team analyze /resolve issue Member Financial Outstanding Liabilities Analyze

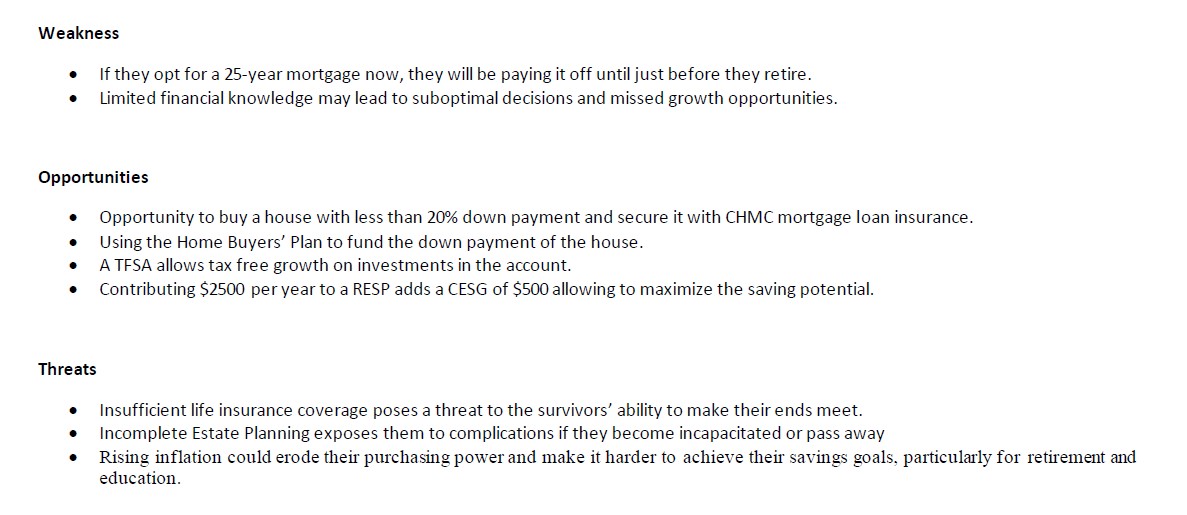

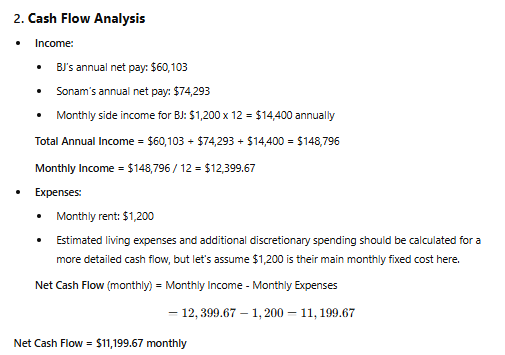

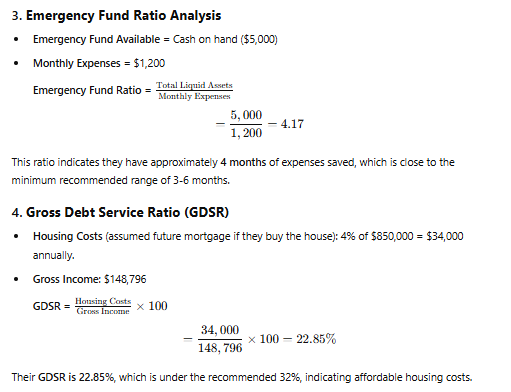

Areas Key issues to analyze in the Financial Plan Priority Analysis to be completed to Responsible Team analyze /resolve issue Member Financial Outstanding Liabilities Analyze Net Worth and Aryan Nanda Management Current Emergency Fund High Cash Flow Statements to Liquidity available. find capital available to pay Purchasing the home. off current debts with high interest rates. Emergency Fund Ratio analysis Liquidity Ratio analysis Analyze GDSR and TDSR to determine mortgage affordability. Funding the downpayment for the home using a mix of liquid assets, HBP, etc. Investment . Investments are concentrated in one asset class Suitable asset allocation Aryan Nanda Planning (GIC) Normal strategies on this basis of Kia's post-secondary education funding. risk profile, current Registered and Non-Registered Investment. situation and future objectives. Create and project a RESP. Exploring various Registered Investment Plans for tax benefits.Recommend an Investment Advisor for further in- depth investment advice. Insurance/Risk Management Life insurance coverage gap Mortgage Insurance, in case of home purchase. Disability insurance coverage High Calculate required life insurance on the hasis using income approach. Consider mortgage insurance for future home purchase protection. Analyzing current disability insurance to highlight any coverage gaps. Recommend Insurance Broker for obtaining necessary insurance. Nadia Danishyar Tax Planning RRSP contributions Capital Gains on non-registered assets. Business-related motor vehicle expenses Normal Maximize RRSP contributions to reduce taxable income. Calculate tax liability on non-registered. Calculate the portion of vehicle expenses relating to business. Recommend a Tax Specialist to further implement tax efficient strategies. Nadia Danishyar Retirement Planning Determine retirement expenses and goals. Calculate total funds required to fulfill desired retirement lifestyle. Normal Calculate and pool current sources of income available during retirement Aryan Nanda and compare to the required amount. In case of a shortfall, suggest necessary strategies to coverthe gap. Estate Planning & Legal Aspects Lack of updated wills POAs Tax Liahility of Estate High Recommend a lawyer for creating new wills and appointing POAs for property. Ensure POAs are in place for personal care. Designate a suitable guardian for Kia in the will. Estimate tax liability on terminal tax return. Name beneficiaries wherever applicable. Nadia Danishyar Other Strengths or weaknesses/ Opportunities or Constraints (SWOT) Strengths e Secure pension plan supported by provincial government. e RRSP contributions in less risky asset class. e Time available till Kia's post-secondary education allows for time to save the funds required. Weakness e |fthey opt for a 25-year mortgage now, they will be paying it off until just before they retire. limited financial knowledge may lead to suboptimal decisions and missed growth opportunities. Opportunities Opportunity to buy a house with less than 20% down payment and secure it with CHMC mortgage loan insurance. e Using the Home Buyers' Plan to fund the down payment of the house. ATFSA allows tax free growth on investments in the account. e Contributing $2500 per year to a RESP adds a CESG of $500 allowing to maximize the saving potential. Threats e Insufficient life insurance coverage poses a threat to the survivors' ability to make their ends meet. * Incomplete Estate Planning exposes them to complications if they become incapacitated or pass away Rising inflation could erode their purchasing power and make it harder to achieve their savings goals, particularly for retirement and education. Advanced Financial Planning Comprehensive Financial Plan Fall 2024 Advanced Financial Planning Comprehensive Financial Plan Fall 2024 BJ and Sonam Kurant Both BJ and Sonam are members of the teacher's defined benefit pension plan and have health, dental and disability benefits through their employer. The pension plan appears to be in good position and well supported by the provincial government. Background You met BJ and Sonam Kurant through a mutual friend. They are a young couple and have never worked with a financial planner before. They believe they're too young for a financial plan; frankly, they Financial position have relatively little in the way of assets right now, so they didn't think a financial planner would see them. But they agreed to meet with you. Today is September 30, 2024. Real estate Last year, BJ and Sonam had their first child, Kia. Now that they are parents, their friend recommended BJ and Sonam would like to buy a home in the new development across from the school. The model that they get their finances in order. Up to now, they have relied upon informal financial advice from that they like is priced at $850,000. Although less expensive models are available, they really like the friends and family, even though none of them have experience in financial planning. Their first question floor plan of this model, and the pie shaped lot which has a bigger backyard for Kia. They are not sure if to you is how you are paid and what fees they can expect. You explain to them that you charge a flat fee they will qualify for a mortgage. Although they anticipate getting raises every year, they anticipate it will for a financial plan that includes all steps of the financial planning process. You will assist the client with be tight. They would like your advice on this matter. referrals to other professionals where warranted, e.g. lawyers, accountants, to help implement the recommendations in the financial plan. They would also like to know more about the Home Buyer's Plan and how they may be able to use their RRSP toward their dream of home ownership. They say that they have cash on hand, about $5,000, and Personal Information: did not know whether they should put it into their RRSP or use it as part of a down payment. Education Savings BJ (age 36) and Sonam (age 32) are both elementary teachers at a small middle school in Erin, Ontario. Soon after Kia was born, BJ and Sonam opened a high interest savings account with Tangerine, an online Sonam just finished her graduate degree in Fine Arts and they both started their jobs this September. bank, and have been depositing small amounts from time to time - mostly money that was given to Kia sonam teaches art history and BJ is the head of the math department. They have been married for two as gifts from relatives. The balance has grown to $4,728 . They would like to invest the funds in years, both are in excellent health and enjoy a healthy lifestyle. something that will yield higher returns over the long run. Currently, they are living in a 2-bedroom 2"d floor apartment in a house on the outskirts of town. They BJ's Registered Investments say that they only pay $1,200/month in rent including all utilities. They are very happy with this arrangement since a comparable apartment located near the school would be at least $850 more per BJ opened an RRSP Daily Interest Savings plan at the local credit union two years ago. He said that he month. As faculty, they can eat in the school cafeteria for a fraction of the price charged in a restaurant was uncertain what investments to make so he simply has it in an interest-bearing account where he is in town. earning 2.65% interest. He tells you that he just added $2,500 to the account last week and it has a Both BJ and Sonam come from relatively large families. Because of this, they have been (and still are) current value of $6,300. reluctant to ask their parents for financial assistance. BJ's Non-Registered Investments Employment Information BJ has non-registered money invested in a 5-year GIC which he purchased in 2020. He is earning 4.69% rate of interest on that $3,500 investment. Details of BJ and Sonam's Employment Sonam's Registered Investments 3 earns $85,000 per year. After all source deductions (taxes, CPP, El, Union dues, LTD premiums) his Sonam also banks at the local credit union and has purchased GICs with her RRSP contributions: net annual pay is $60,103. Sonam, with her graduate degree is now compensated through a higher pay $3,000 GIC, 2.2% rate of interest grid, so she earns $104,000 per year. After all source deductions, her net annual pay is $74,293. Once $4,500 GIC, 2.5% rate of interest the maximum CPP and El premiums are deducted (by late June for BJ, late May for Sonam) their take home salaries will increase by the amount of those deductions. Both are paid bi-monthly. Last year, BJ Both mature this month. also started to supplement his income by tutoring students three nights per week. He earns $1,200 per Sonam's Non-Registered Investments month from this extra work for 12 months a year. Sonam has an interest in fine art and purchased a painting several years ago by a well-known artist at an estate sale when she was visiting friends. She paid $470 for the painting and believes that it is worthAdvanced Financial Planning Comprehensive Financial Plan Fall 2024 Advanced Financial Planning Comprehensive Financial Plan Fall 2024 approximately $20,000 today. While she is very attached to the work of art, she is willing to sell it, if Goals and Objectives necessary, to make her dreams come true. Liabilities Besides home ownership, BJ and Sonam say that they want to ensure that Kia has enough money to go to university. Since they work in education, they know that the cost of tuition will increase over the next BJ has a student loan with an outstanding balance of $4,800 on which he is paying 5.75%% interest. He is two decades. They believe that they will need $120,000 for Kia's post secondary education. They would like to have this amount saved by the time she finishes high school. also carrying a $2,230 balance on his Visa card and pays 239% interest (annual rate) on any outstanding balances. BJ and Sonam say that their focus on education has meant they have given little thought about their BJ and Sonam have leased a conservative sedan that costs them $380 per month. Currently, the mileage retirement. They hope that their pension plans will serve them well and provide them with a good on the vehicle is very low, averaging 18,000 km per year. They figure that 25%% of the car's usage relates retirement lifestyle to BJ's business. Sonam has no outstanding debts and pays off her credit card every month. Assumptions: Insurance They have a combined average tax rate of 27%; and an MTR of 30% Inflation 3.29 Both BJ and Sonam have group life insurance through their employer for two times their annual salaries. Life expectancy age 92 They also have long term disability (LTD) benefits (609% income replacement) for which they pay the Current Mortgage Rates: premiums. Their employer also provides health and dental insurance coverage. But since Kia was born, 1-year fixed rate of 6.24% they have been worried that they do not have enough life insurance, should either of them die 2-year fixed rate of 5.34% prematurely. If one spouse were to die, they believe that the survivor would require additional income 3-year fixed rate of 4.19% equal to at least 60% of their current combined gross income for the next 35 years. They would prefer o 5-year fixed rate of 3.99%% that the mortgage on their home be completely paid off should one of them die. 3-year variable rate of 5.05% o 5-year closed variable rate of 4.70%% They want to know if they should take mortgage life insurance (when they do buy their house) and how Fixed-rate Loan Rates Canada Mortgage and Housing Corporation (CMHC) insurance can help them. 3-year fixed rate of 7% 5-year fixed rate of 6.25% Pension Plan - Defined Benefit Risk Profile o Non-contributory o 2% x best 5-year average earnings x service BJ and Sonam agree that they are both conservative investors, although they are prepared to accept o Current salaries will increase each year with inflation to retirement some risk for a higher rate of return. They do not like the rate of return they are getting now but ultimately fear loss of capital in the stock market. They have heard so many horror stories. Liquidity is a primary concern for them as they want to be able to access savings quickly should they get the chance to make an offer on their dream home. They are watching the sales and know that there is only a few of their selected model left. Wills and Power of Attorney Shortly after Kia was born, BJ and Sonam purchased a will planning package online. They filled out the forms on their computer and printed off the wills in a standard format. Their friends from school witnessed the document. They failed to name a guardian for Kia because they could not decide who would be best. Sonam's sister, Muskan, is their estate trustee and attorney under their POAs for both BJ and Sonam.1. Net Worth Calculation Assets: Cash on hand: $5,000 Education savings (Tangerine account): $4,728 BJ's Registered Investment: $6,300 BJ's Non-Registered Investment: $3,500 (5-year GIC) Sonam's Registered Investments: GIG: $3,000 at 2.2% interest GIG: $4,500 at 2.5% interest . Sonam's Non-Registered Investment: Painting valued at $20,000 Liabilities: BJ's student loan: $4,800 at 5.75% interest Credit card debt: $2,230 at 23% interest Net Worth: Net Worth - Total Assets - Total Liabilities - (5, 000 + 4, 728 + 6, 300 + 3, 500 + 3, 000 + 4, 500 + 20, 000) - (4, 800 + 2, 230) - 47, 028 - 7, 030 - 39, 998 Net Worth = $39,9982. Cash Flow Analysis . Income: BJ's annual net pay: $60,103 . Sonam's annual net pay: $74,293 Monthly side income for BJ: $1,200 x 12 = $14,400 annually Total Annual Income = $60,103 + $74,293 + $14,400 = $148,796 Monthly Income = $148,796 / 12 = $12 399.67 Expenses: Monthly rent: $1,200 Estimated living expenses and additional discretionary spending should be calculated for a more detailed cash flow, but let's assume $1,200 is their main monthly fixed cost here. Net Cash Flow (monthly) = Monthly Income - Monthly Expenses - 12, 399.67 - 1, 200 - 11, 199.67 Net Cash Flow = $11,199.67 monthly3. Emergency Fund Ratio Analysis . Emergency Fund Available = Cash on hand ($5,000) Monthly Expenses = $1,200 Emergency Fund Ratio = Total Liquid Assets Monthly Expenses 5, 000 - 4.17 1, 200 This ratio indicates they have approximately 4 months of expenses saved, which is dose to the minimum recommended range of 3-6 months. 4. Gross Debt Service Ratio (GDSR) . Housing Costs (assumed future mortgage if they buy the house): 4% of $850,000 = $34,000 annually. Gross Income: $148,796 GDSR = Housing Costs Gross Income x 100 34, 000 x 100 - 22.85% 148, 796 Their GDSR is 22.85% which is under the recommended 32%, indicating affordable housing costs

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!