Question: As shown above, answer question 11 with all steps shown. What are the prices of a call option and a put option wi with the

As shown above, answer question 11 with all steps shown.

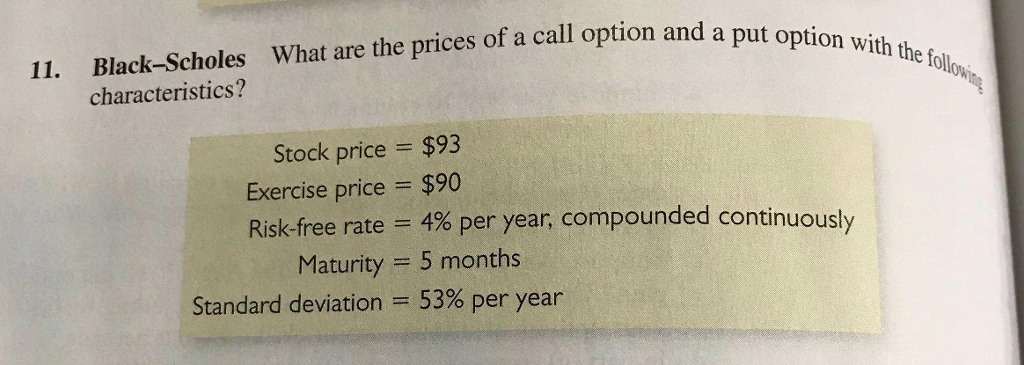

What are the prices of a call option and a put option wi with the fo 11. Black-Scholes characteristics? Stock price = $93 Exercise price = $90 Risk-free rate 4% per year, compounded continuously Maturity = 5 months Standard deviation = 53% per year

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock