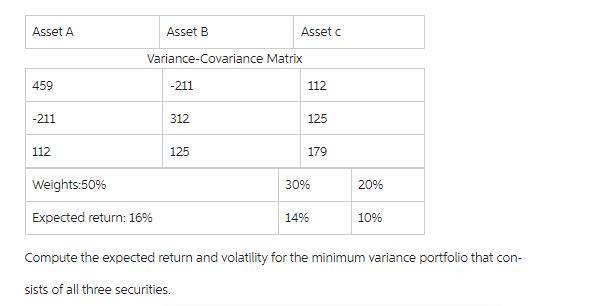

Question: Asset A 459 -211 112 Asset B Weights:50% Expected return: 16% Variance-Covariance Matrix -211 312 Asset c 125 112 125 179 30% 14% 20%

Asset A 459 -211 112 Asset B Weights:50% Expected return: 16% Variance-Covariance Matrix -211 312 Asset c 125 112 125 179 30% 14% 20% 10% Compute the expected return and volatility for the minimum variance portfolio that con- sists of all three securities.

Step by Step Solution

★★★★★

3.55 Rating (162 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

To compute the expected return and volatility for the minimum variance portfolio that consists of al... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock