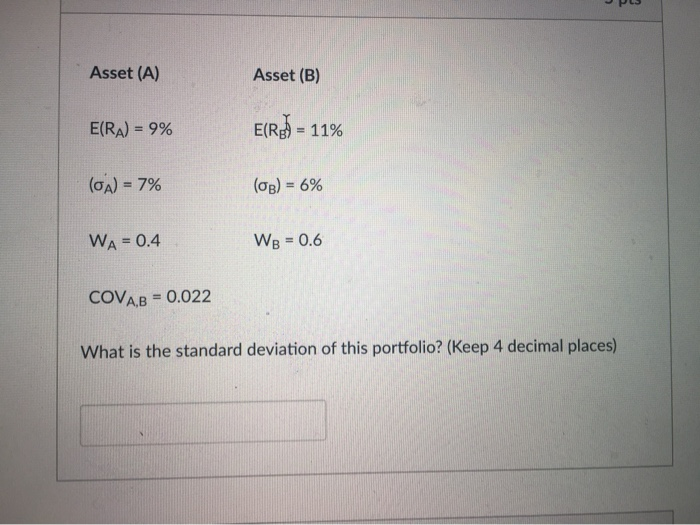

Question: Asset (A) Asset (B) E(RA) = 9% E(R) = 11% (CA) = 7% (OB) = 6% WA = 0.4 WB = 0.6 COVA,B = 0.022

Asset (A) Asset (B) E(RA) = 9% E(R) = 11% (CA) = 7% (OB) = 6% WA = 0.4 WB = 0.6 COVA,B = 0.022 What is the standard deviation of this portfolio? (Keep 4 decimal places)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock