Question: Assets A, B, and C are the only assets available with the following charac- teristics: Asset Expected Return Standard deviation 0.1 0.1 B 0.15 0.18

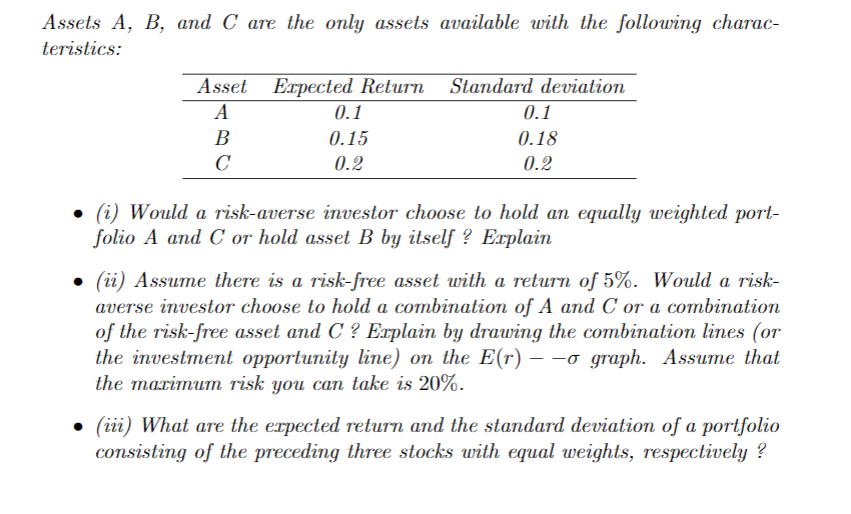

Assets A, B, and C are the only assets available with the following charac- teristics: Asset Expected Return Standard deviation 0.1 0.1 B 0.15 0.18 0.2 0.2 . (i) Would a risk-averse investor choose to hold an equally weighted port- folio A and C or hold asset B by itself ? Explain (ii) Assume there is a risk-free asset with a return of 5%. Would a risk- averse investor choose to hold a combination of A and C or a combination of the risk-free asset and C ? Explain by drawing the combination lines (or the investment opportunity line) on the E(r) - -o graph. Assume that the marimum risk you can take is 20%. (iii) What are the expected return and the standard deviation of a portfolio consisting of the preceding three stocks with equal weights, respectively ? Assets A, B, and C are the only assets available with the following charac- teristics: Asset Expected Return Standard deviation 0.1 0.1 B 0.15 0.18 0.2 0.2 . (i) Would a risk-averse investor choose to hold an equally weighted port- folio A and C or hold asset B by itself ? Explain (ii) Assume there is a risk-free asset with a return of 5%. Would a risk- averse investor choose to hold a combination of A and C or a combination of the risk-free asset and C ? Explain by drawing the combination lines (or the investment opportunity line) on the E(r) - -o graph. Assume that the marimum risk you can take is 20%. (iii) What are the expected return and the standard deviation of a portfolio consisting of the preceding three stocks with equal weights, respectively

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts