Question: Assignment 3 1. There are 1,700 stocks in the Value Line index. How many covariances would have to be computed to use the Markowitz full-covariance

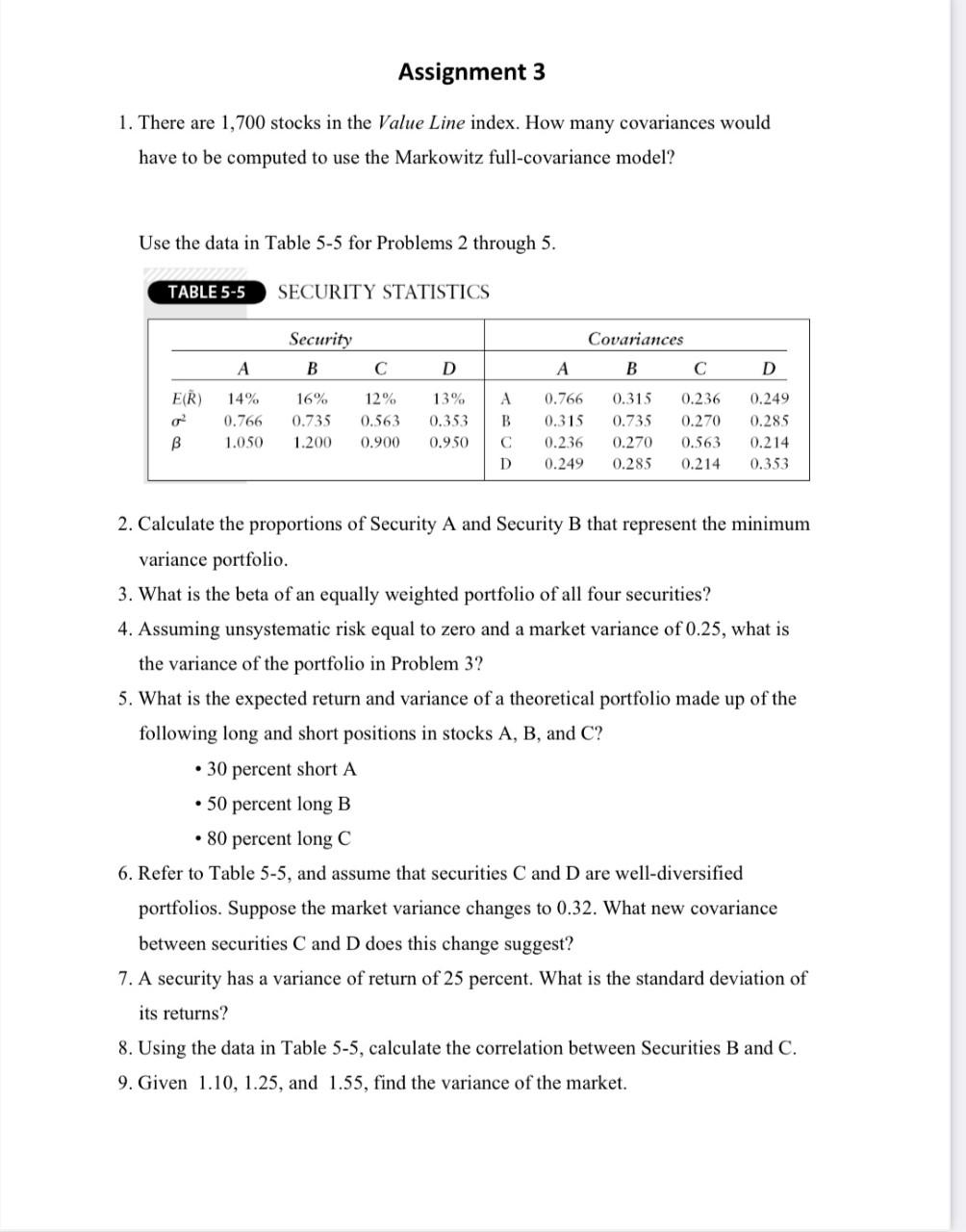

Assignment 3 1. There are 1,700 stocks in the Value Line index. How many covariances would have to be computed to use the Markowitz full-covariance model? Use the data in Table 5-5 for Problems 2 through 5. TABLE 5-5 SECURITY STATISTICS Covariances Security B A C D A B D ER) A 14% 0.766 1.050 16% 0.735 1.200 12% 0.563 0.900 13% 0.353 0.950 0.766 0.315 0.236 0.249 B D 0.315 0.735 0.270 0.285 0.236 0.270 0.563 0.214 0.249 0.285 0.214 0.353 B 2. Calculate the proportions of Security A and Security B that represent the minimum variance portfolio. 3. What is the beta of an equally weighted portfolio of all four securities? 4. Assuming unsystematic risk equal to zero and a market variance of 0.25, what is the variance of the portfolio in Problem 3? 5. What is the expected return and variance of a theoretical portfolio made up of the following long and short positions in stocks A, B, and C? 30 percent short A 50 percent long B 80 percent long C 6. Refer to Table 5-5, and assume that securities C and D are well-diversified portfolios. Suppose the market variance changes to 0.32. What new covariance between securities C and D does this change suggest? 7. A security has a variance of return of 25 percent. What is the standard deviation of a its returns? . 8. Using the data in Table 5-5, calculate the correlation between Securities B and C. 9. Given 1.10, 1.25, and 1.55, find the variance of the market

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts