Question: Assignment # 3 - Home Financing Project Objective The purpose of this assignment is to familiarize students with the process of budgeting for the purchase

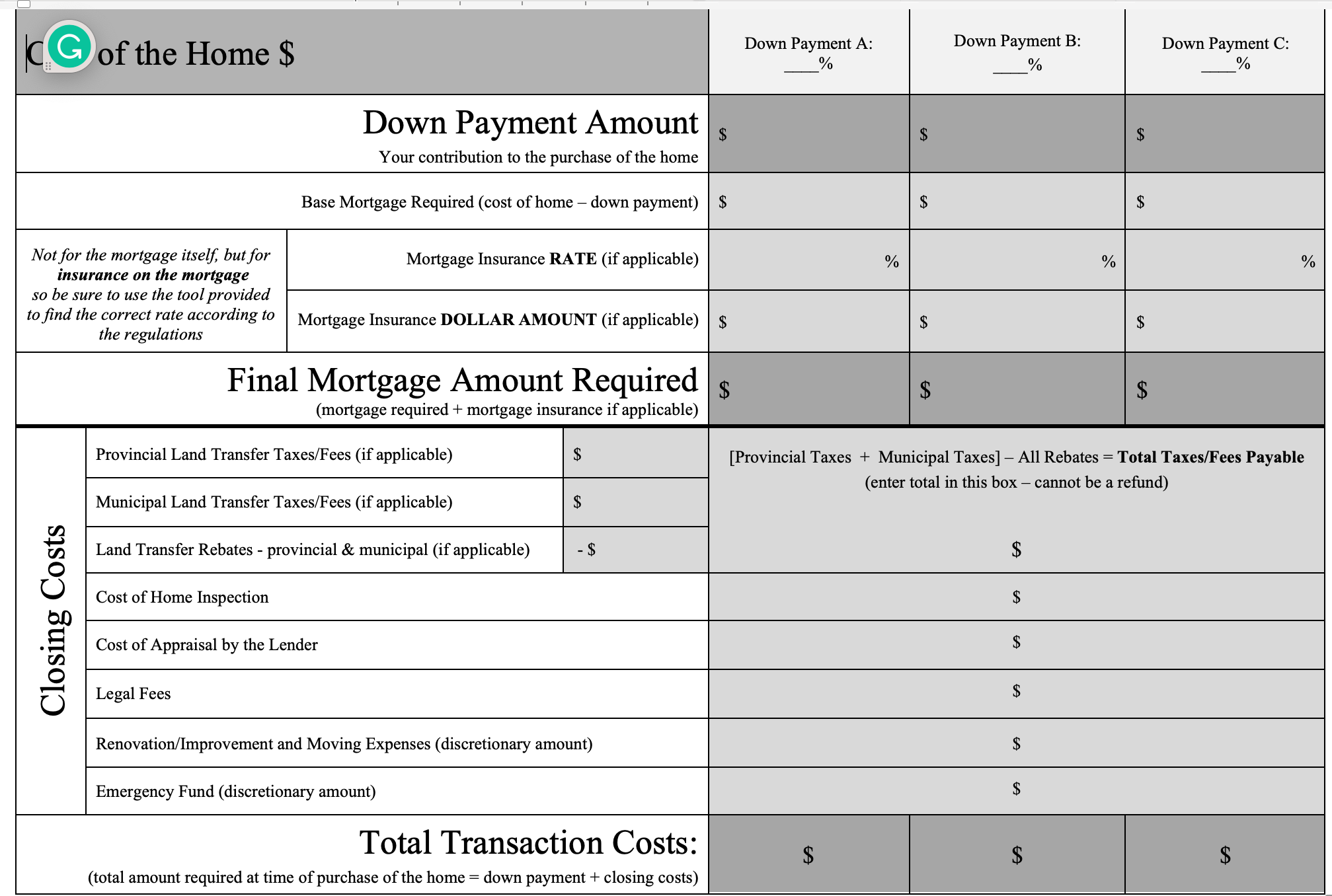

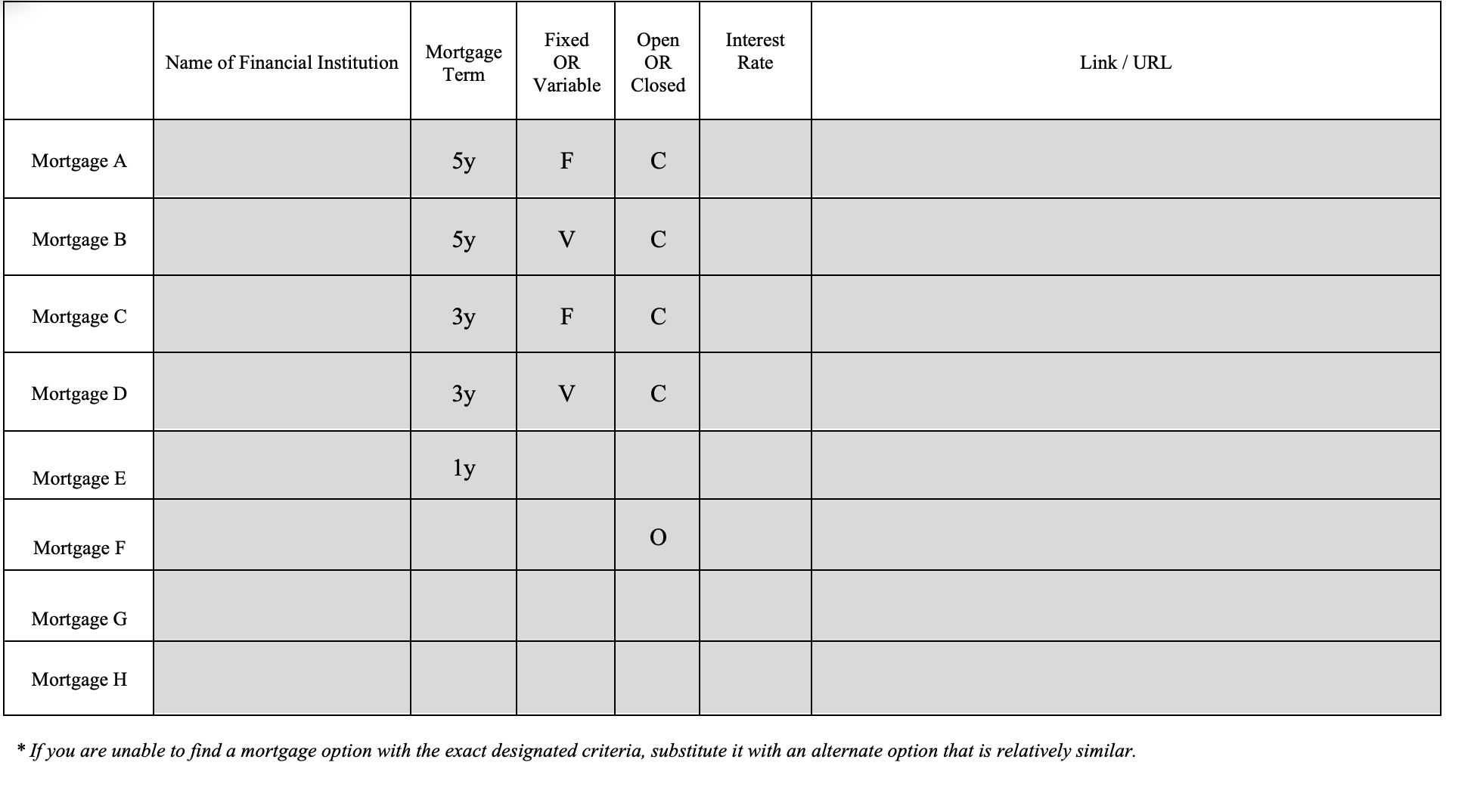

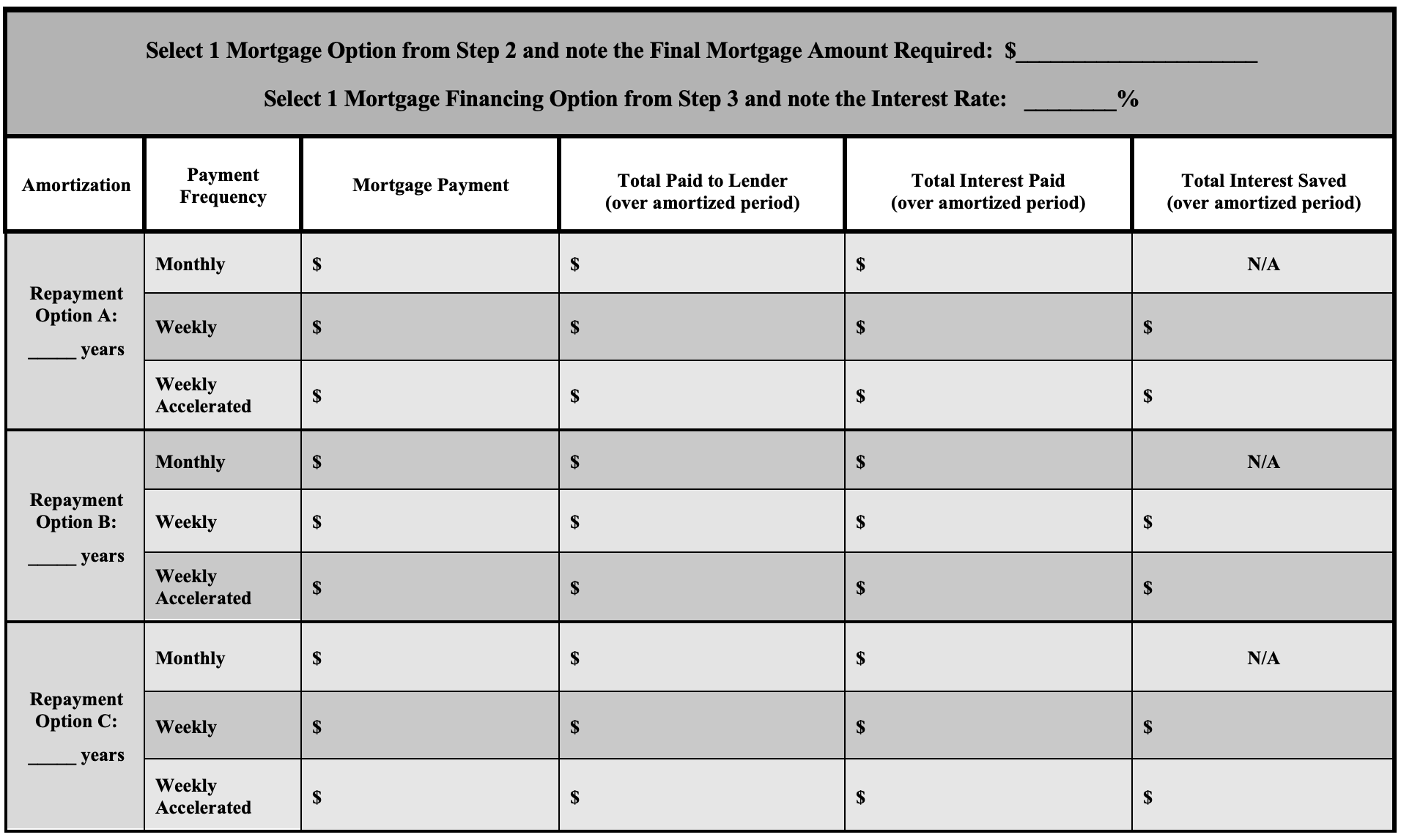

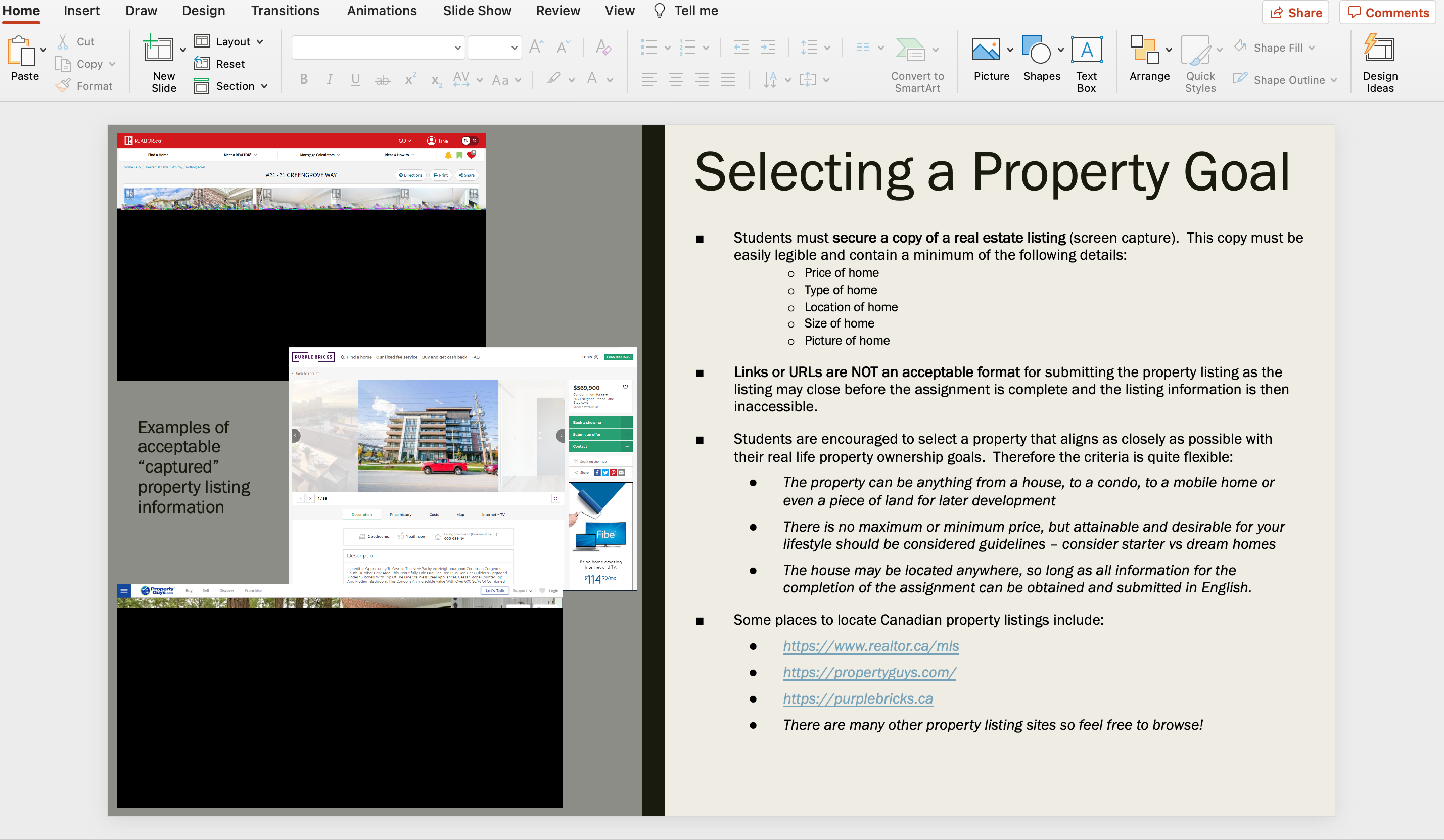

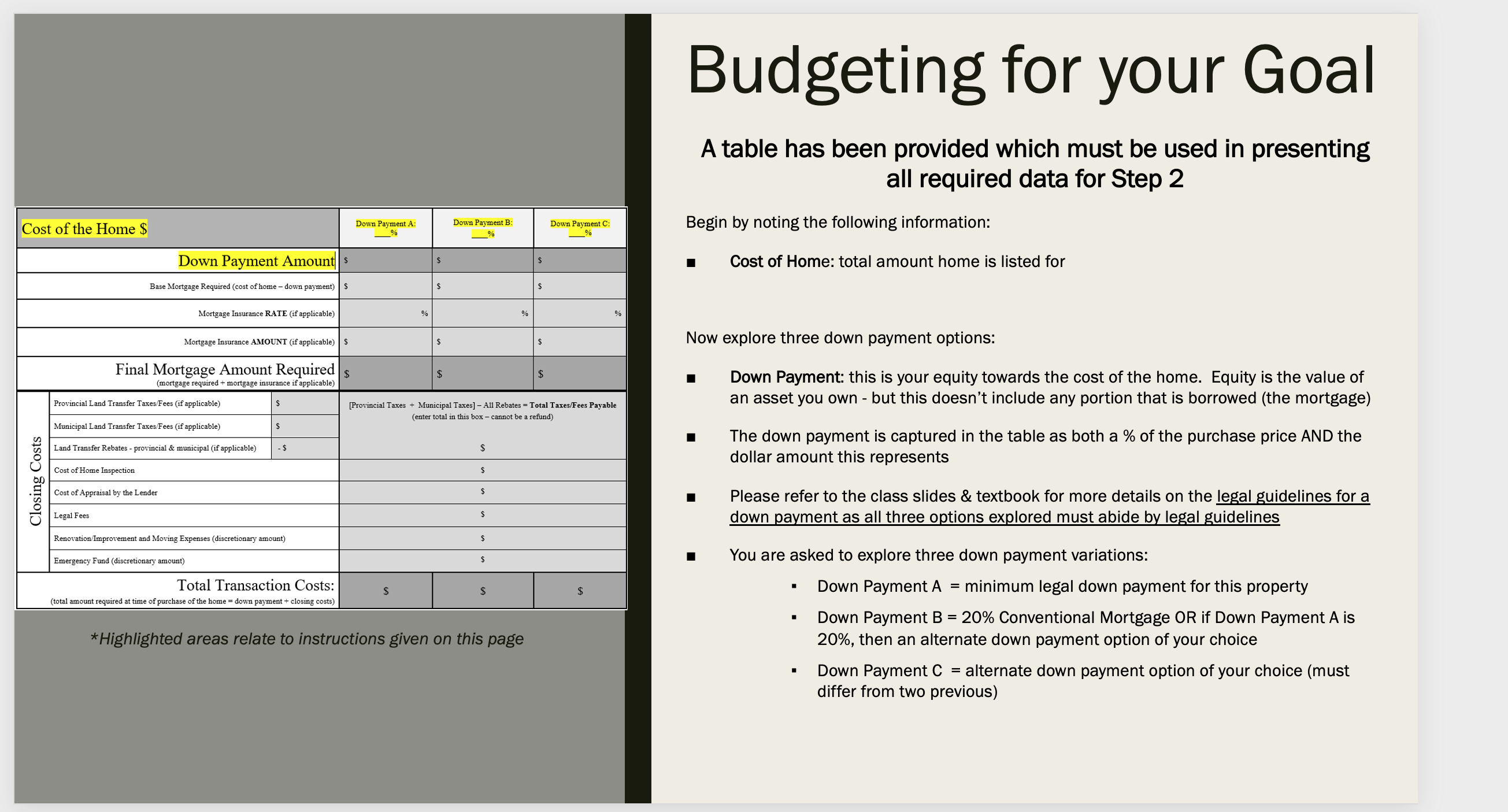

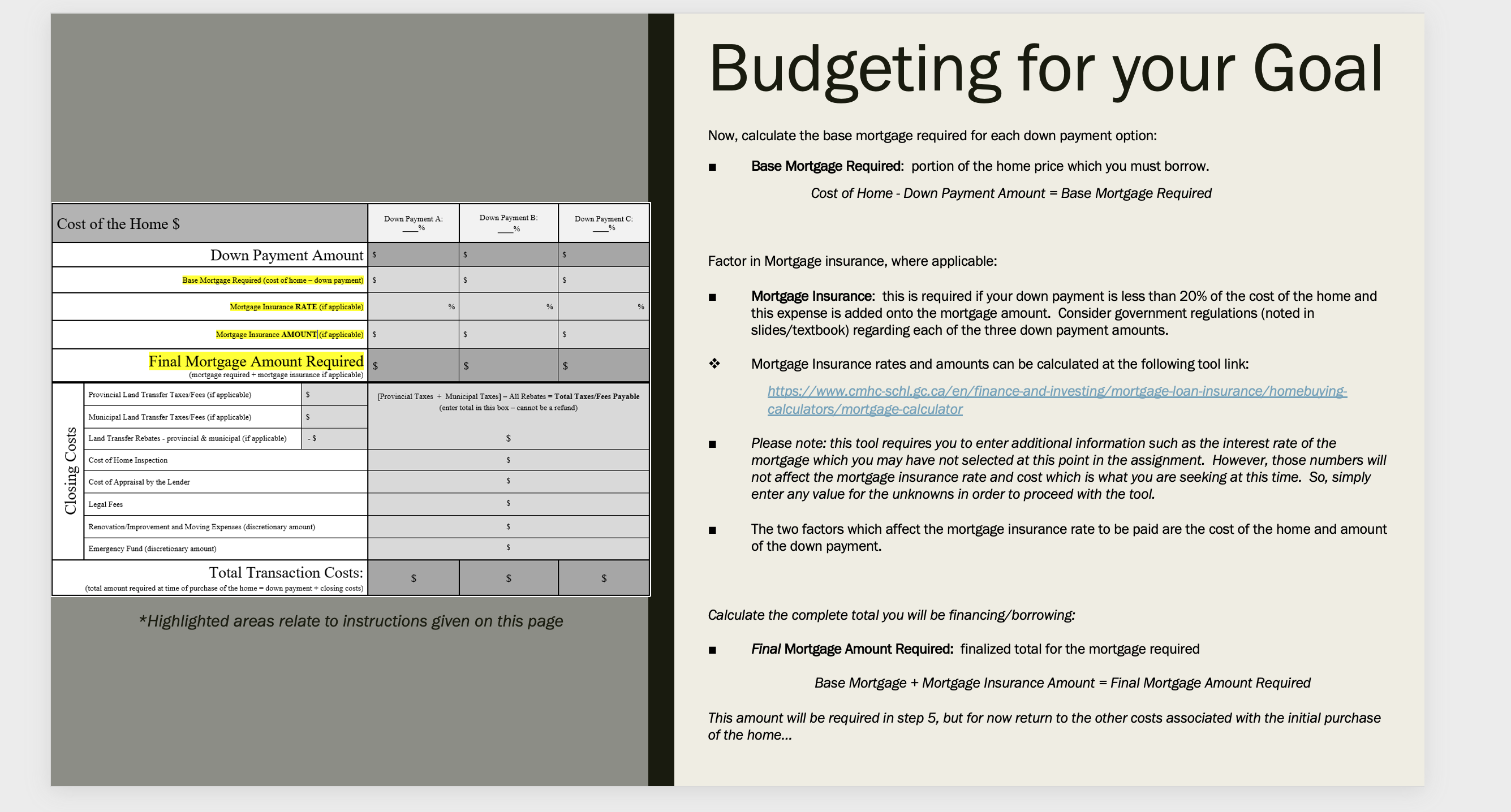

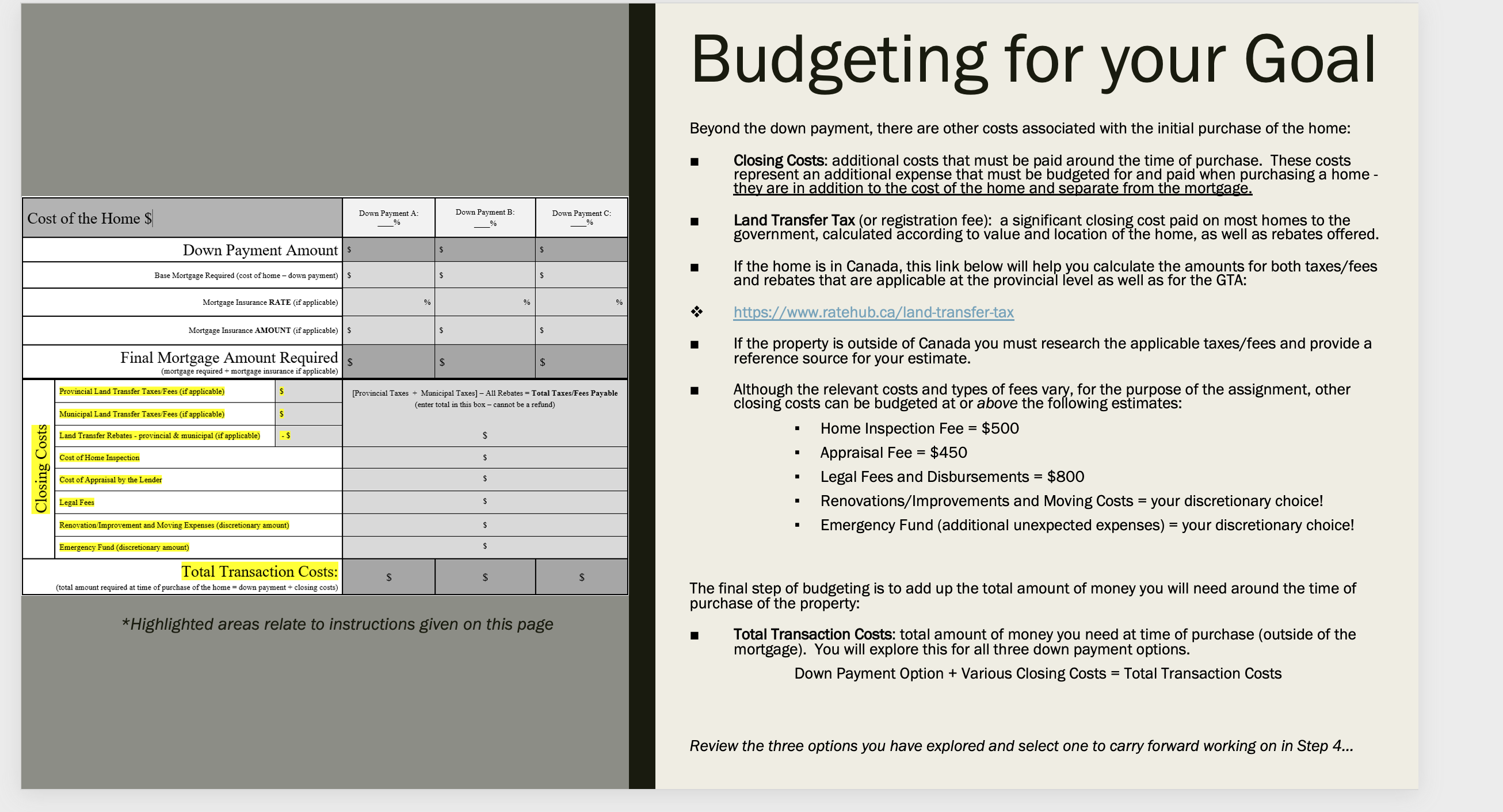

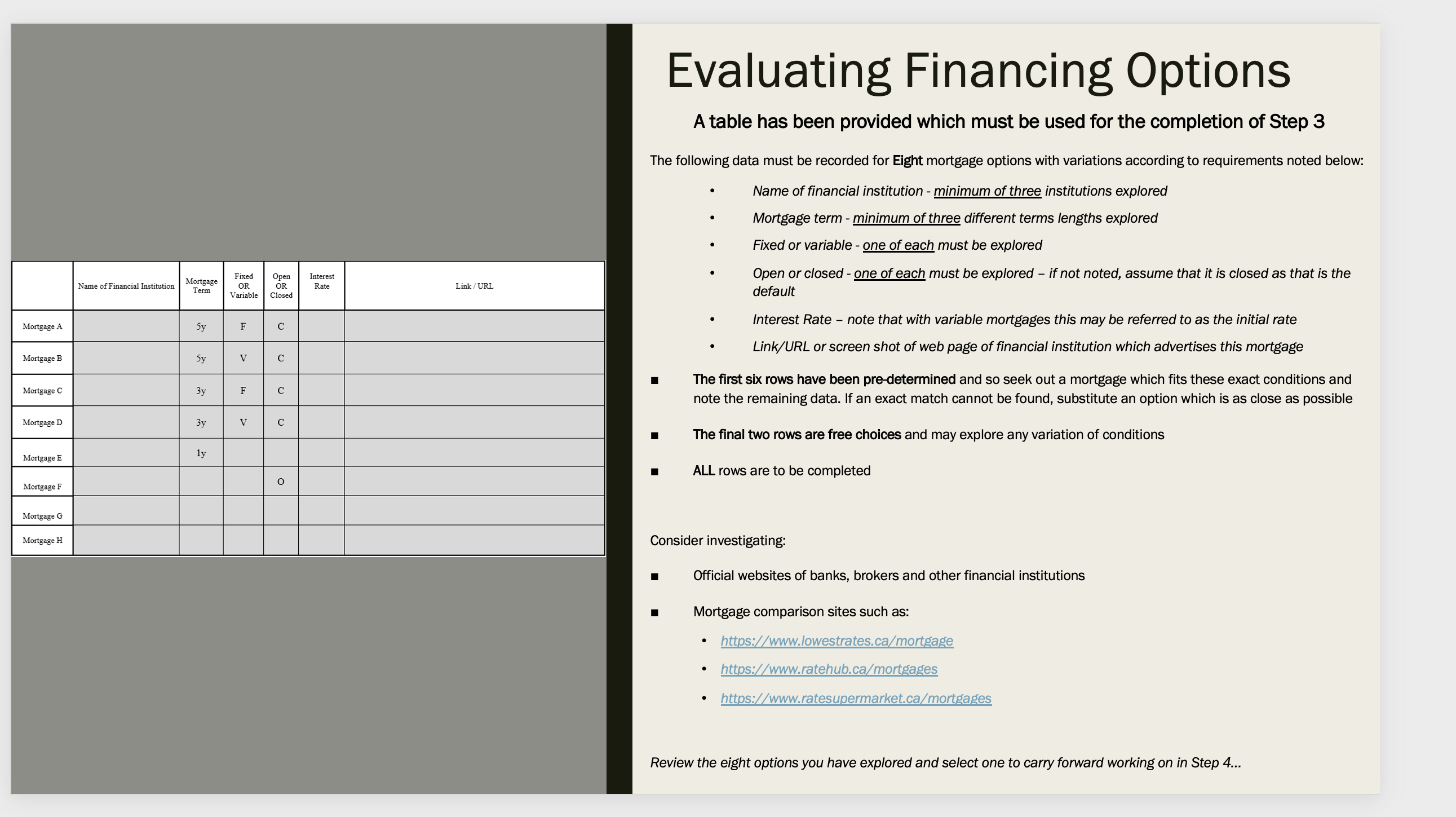

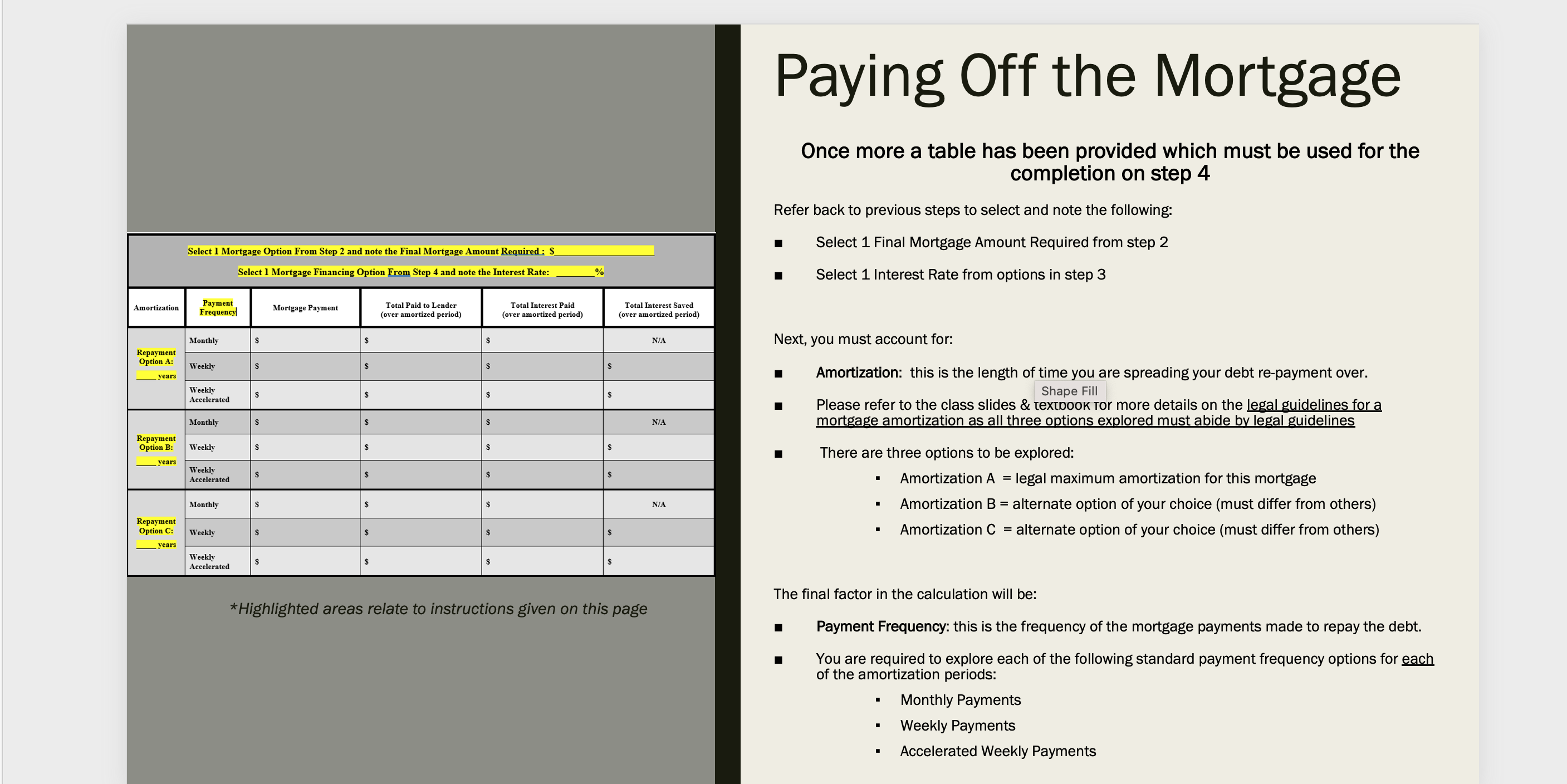

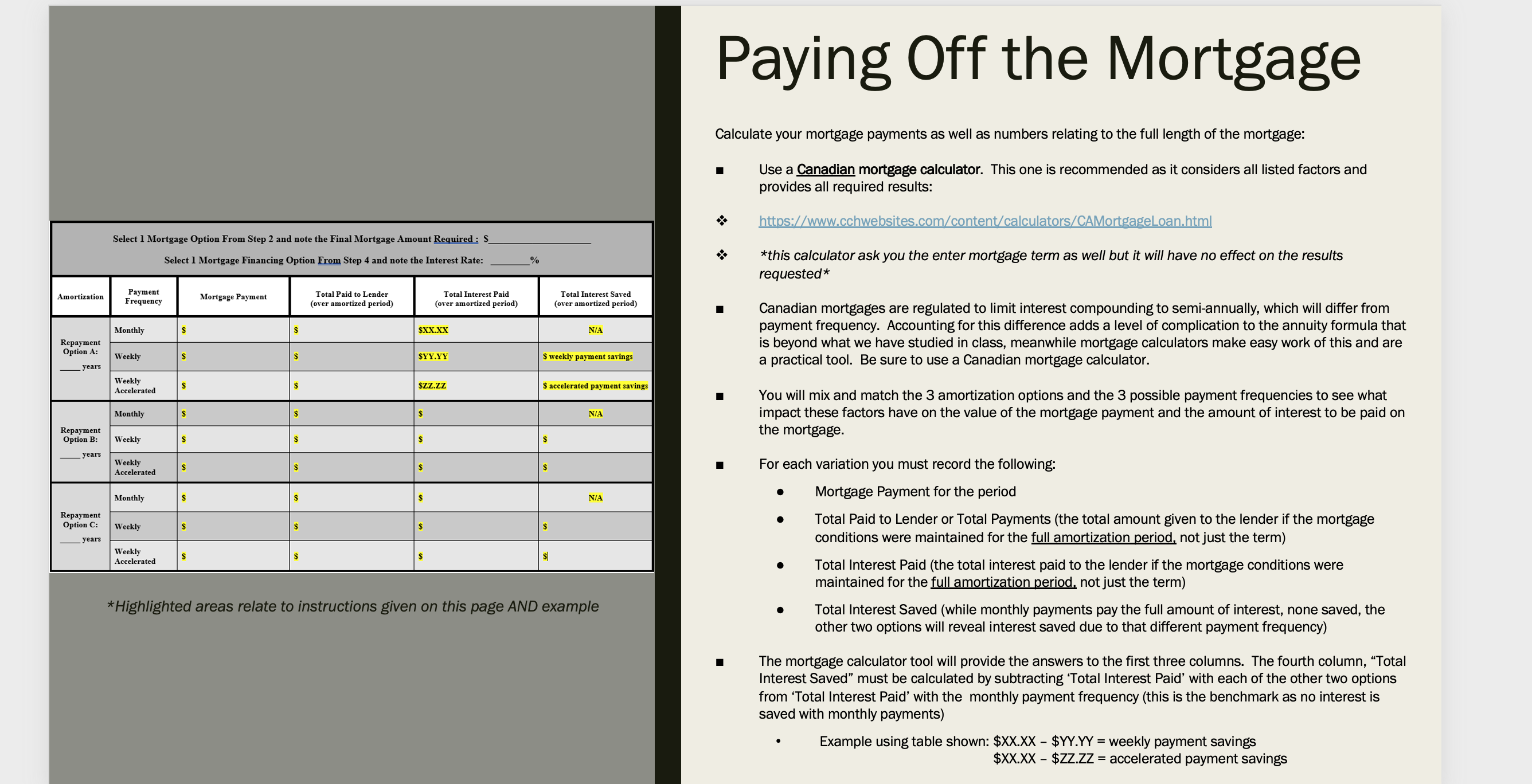

Assignment # 3 - Home Financing Project Objective The purpose of this assignment is to familiarize students with the process of budgeting for the purchase and financing of a home, or another significant financed purchase, as well as building awareness of key factors not to be overlooked throughout this process. Overview This assignment is comprised of four parts: 1. Selecting a Property Goal: Students must select, and secure a copy of, a current property listing which is representative of a real estate investment goal they may wish to pursue. 2. Budgeting for your Goal: Students must perform several calculations to determine the total transaction costs, including both the down payment and closing costs, that will be required in order to purchase the home they have selected. Variations on these calculations will explore the effects of making financial planning adjustments 3. Evaluating Financing Options: Students must examine the advertised mortgage options available through various financial institutions, considering several financing contract factors, in order to finance the remaining cost of the home. Various financing options will help expose the impacts of different mortgage factors 4. Paying Off the Mortgage: Finally, applying data collected, previous decisions made and incorporating some additional considerations, students must calculate the corresponding monthly mortgage payments by using an online mortgage calculator. Variations on these calculations will explore the effects of making financial planning adjustments.Down Payment B: % Down Payment A: % Down Payment C: % Down Payment Amount Your contribution to the purchase of the home Base Mortgage Required (cost of home down payment) Not for the mortgage itself but for insurance on the mortgage so be sure to use the tool provided tami the correct rate according to the regulations Mortgage Insurance RATE (if applicable) Mortgage Insurance DOLLAR AMOUNT (if applicable) Final Mortgage Amount Required (mortgage required + mortgage insurance if applicable) Provincial Land Transfer Taxes/Fees (if applicable) Municipal Land Transfer Taxes/Fees (if applicable) U.) '53 Land Transfer Rebates - provincial & municipal (if applicable) 0 0 Cost of Home Inspection OD .E Cost of Appraisal by the Lender O a Legal Fees Renovation/Improvement and Moving Expenses (discretionary amount) Emergency Fund (discretionary amount) Total Transaction Costs: (total amount required at time of purchase of the home = down payment + closing costs) Fixed Open Interest Name of Financial Institution Mngag OR OR Rate Link / URL Variable Closed Term Mortgage A Mortgage B Mortgage C Mortgage D Mortgage E Mortgage F Mortgage G Mortgage H " If you are unable tand a mortgage option with the exact designated criteria, substitute it with an alternate option that is relatively similar. Select 1 Mortgage Option from Step 2 and note the Final Mortgage Amount Required: $ Select 1 Mortgage Financing Option from Step 3 and note the Interest Rate: % Amortization Payment Mortgage Payment Total Paid to Lender Total Interest Paid Frequency Total Interest Saved (over amortized period) (over amortized period) (over amortized period) Monthly S S S N/A Repayment Option A: Weekly S $ S $ years Weekly S Accelerated $ S $ Monthly S N/A Repayment Option B: Weekly S S $ $ years Weekly Accelerated $ $ $ Monthly $ N/A Repayment Option C: Weekly S $ $ years Weekly Accelerated $ $ $ $Home Insert Draw Design Transitions Animations Slide Show Review View ? Tell me LE Share Comments & Cut Layout v AA AD " OVA Shape Fill [A Copy 27 Reset Paste New Convert to Picture Shapes Text Arrange Format B I U ab x x2 AV " Aav D Av Quick Shape Outline v Design slide Section v SmartArt Box Styles Ideas [E REALTOR.co CAD kania FR Find a Home Meet a REALTOR Mortgage Calculators Ideas & How to #21-21 GREENGROVE WAY @ Directions A Print $ Share Selecting a Property Goal Students must secure a copy of a real estate listing (screen capture). This copy must be easily legible and contain a minimum of the following details: o Price of home o Type of home o Location of home o Size of home Picture of home PURPLE BRICKS Q Find a home Our fixed fee service Buy and get cash back FAQ LOON Fess-959-9760 Back to results Links or URLs are NOT an acceptable format for submitting the property listing as the $569,900 O listing may close before the assignment is complete and the listing information is then inaccessible. Examples of Back a showing acceptable Contact Students are encouraged to select a property that aligns as closely as possible with "captured" their real life property ownership goals. Therefore the criteria is quite flexible: property listing The property can be anything from a house, to a condo, to a mobile home or 1/ 35 information even a piece of land for later development Description Price history Costs Map Internet - TV There is no maximum or minimum price, but attainable and desirable for your 2bedrooms @ 1bathroom ( 600 693 6:" Fibe lifestyle should be considered guidelines - consider starter vs dream homes Description south Humber rath eres this venus fully Laid out one Bed tus Der Has murders upgraded Internet und TV. The house may be located anywhere, so long as all information for the lu Modern watson this conde is An tisdale value will over woo sets of combined $11490/ mo. = exoparty By Sel Let's Talk Support ~ Login completion of the assignment can be obtained and submitted in English. Some places to locate Canadian property listings include: https://www.realtor.ca/mls . https://propertyguys.com/ . https://purplebricks.ca There are many other property listing sites so feel free to browse!STEP 2: BUDGETING FOR YOUR GOAL Students must perform several calculations to determine the total transaction costs, including both the down payment and closing costs, that will be required in order to purchase the home they have selected Variations on these calculations will explore the effects of making financial planning adjustments Budgeting for your Goal A table has been provided which must be used in presenting all required data for Step 2 Cost of the Home $ Down Payment A: Down Payment B: Down Payment C: Begin by noting the following information: % % % Down Payment Amount| s Cost of Home: total amount home is listed for Base Mortgage Required (cost of home - down payment) Mortgage Insurance RATE (if applicable) % Mortgage Insurance AMOUNT (if applicable) Now explore three down payment options: Final Mortgage Amount Required $ $ $ (mortgage required + mortgage insurance if applicable) Down Payment: this is your equity towards the cost of the home. Equity is the value of Provincial Land Transfer Taxes/Fees (if applicable [Provincial Taxes + Municipal Taxes] - All Rebates = Total Taxes/Fees Payable an asset you own - but this doesn't include any portion that is borrowed (the mortgage) (enter total in this box - cannot be a refund) Municipal Land Transfer Taxes/Fees (if applicable) The down payment is captured in the table as both a % of the purchase price AND the Land Transfer Rebates - provincial & municipal (if applicable) $ dollar amount this represents Cost of Home Inspection Closing Costs Cost of Appraisal by the Lender S Please refer to the class slides & textbook for more details on the legal guidelines for a Legal Fees down payment as all three options explored must abide by legal guidelines Renovation/Improvement and Moving Expenses (discretionary amount) $ Emergency Fund (discretionary amount) S You are asked to explore three down payment variations: Total Transaction Costs: S $ Down Payment A = minimum legal down payment for this property (total amount required at time of purchase of the home = down payment + closing costs) Down Payment B = 20% Conventional Mortgage OR if Down Payment A is *Highlighted areas relate to instructions given on this page 20%, then an alternate down payment option of your choice Down Payment C = alternate down payment option of your choice (must differ from two previous)Budgeting for your Goal Now, calculate the base mortgage required for each down payment option: Base Mortgage Required: portion of the home price which you must borrow. Cost of Home - Down Payment Amount = Base Mortgage Required Cost of the Home $ Down Payment A: Down Payment B: Down Payment C: Down Payment Amount s S Factor in Mortgage insurance, where applicable: Base Mortgage Required (cost of home - down payment) S Mortgage Insurance: this is required if your down payment is less than 20% of the cost of the home and Mortgage Insurance RATE (if applicable) % this expense is added onto the mortgage amount. Consider government regulations (noted in Mortgage Insurance AMOUNT| (if applicable) |$ S slides/textbook) regarding each of the three down payment amounts. Final Mortgage Amount Required S Mortgage Insurance rates and amounts can be calculated at the following tool link: (mortgage required + mortgage insurance if applicable) Provincial Land Transfer Taxes/Fees (if applicable) [Provincial Taxes + Municipal Taxes] - All Rebates = Total Taxes/Fees Payable https://www.cmhc-schl.gc.ca/en/finance and-investing/mortgage-loan-insurance/homebuying. (enter total in this box - cannot be a refund) Municipal Land Transfer Taxes/Fees (if applicable) calculators/mortgage calculator Land Transfer Rebates - provincial & municipal (if applicable) - S S Please note: this tool requires you to enter additional information such as the interest rate of the Cost of Home Inspection mortgage which you may have not selected at this point in the assignment. However, those numbers will Closing Costs Cost of Appraisal by the Lender S not affect the mortgage insurance rate and cost which is what you are seeking at this time. So, simply enter any value for the unknowns in order to proceed with the tool. Legal Fees Renovation/Improvement and Moving Expenses (discretionary amount) The two factors which affect the mortgage insurance rate to be paid are the cost of the home and amount Emergency Fund (discretionary amount) of the down payment. Total Transaction Costs: (total amount required at time of purchase of the home = down payment + closing costs) *Highlighted areas relate to instructions given on this page Calculate the complete total you will be financing/borrowing: Final Mortgage Amount Required: finalized total for the mortgage required Base Mortgage + Mortgage Insurance Amount = Final Mortgage Amount Required This amount will be required in step 5, but for now return to the other costs associated with the initial purchase of the home...Budgeting for your Goal Beyond the down payment, there are other costs associated with the initial purchase of the home: Closing Costs: additional costs that must be paid around the time of purchase. These costs represent an additional expense that must be budgeted for and paid when purchasing a home - they are in addition to the cost of the home and separate from the mortgage Cost of the Home $ Down Payment A: Down Payment B: Down Payment C: % Land Transfer Tax (or registration fee): a significant closing cost paid on most homes to the government, calculated according to value and location of the home, as well as rebates offered. Down Payment Amount | s S S Base Mortgage Required (cost of home - down payment) S If the home is in Canada, this link below will help you calculate the amounts for both taxes/fees and rebates that are applicable at the provincial level as well as for the GTA: Mortgage Insurance RATE (if applicable % https://www.ratehub.ca/land-transfer-tax Mortgage Insurance AMOUNT (if applicable) If the property is outside of Canada you must research the applicable taxes/fees and provide a Final Mortgage Amount Required reference source for your estimate. (mortgage required + mortgage insurance if applicable) Provincial Land Transfer Taxes/Fees (if applicable) S [Provincial Taxes + Municipal Taxes] - All Rebates = Total Taxes/Fees Payable Although the relevant costs and types of fees vary, for the purpose of the assignment, other (enter total in this box - cannot be a refund) closing costs can be budgeted at or above the following estimates: Municipal Land Transfer Taxes/Fees (if applicable) S Land Transfer Rebates - provincial & municipal (if applicable) -S Home Inspection Fee = $500 Cost of Home Inspection Appraisal Fee = $450 Closing Costs Cost of Appraisal by the Lender Legal Fees and Disbursements = $800 Legal Fees Renovations/Improvements and Moving Costs = your discretionary choice! Renovation/Improvement and Moving Expenses (discretionary amount) Emergency Fund (additional unexpected expenses) = your discretionary choice! Emergency Fund (discretionary amount Total Transaction Costs: ( total amount required at time of purchase of the home = down payment + closing costs) The final step of budgeting is to add up the total amount of money you will need around the time of purchase of the property: *Highlighted areas relate to instructions given on this page Total Transaction Costs: total amount of money you need at time of purchase (outside of the mortgage). You will explore this for all three down payment options. Down Payment Option + Various Closing Costs = Total Transaction Costs Review the three options you have explored and select one to carry forward working on in Step 4...STEP 3: EVALUATING FINANCING OPTIONS Students must examine the advertised mortgage options available through various financial institutions, considering several financing contract factors, in order to finance the remaining cost of the home Various financing options will help expose the impacts of different mortgage factors Evaluating Financing Options A table has been provided which must be used for the completion of Step 3 The following data must be recorded for Elm mortgage options with variations according to requirements noted below: - Name of nancial institution - minimum of three institutions explored - Mortgage term - minimum of three different terms lengths explored - Fixed or variable - one of each must be explored - Open or closed - one of each must be explored - if not noted, assume that it is closed as that is the default - interest Rate - note that with variable mortgages this may be referred to as the initial rate - Link/URL or screen shot of web page of nancial institution which advertises this mortgage I The rst six rams have been predetermined and so seek out a mortgage which ts these exact conditions and note the remaining data. lfan exact match cannot be found, substitute an option which is as close as possible I The nal two rows are free choices and may explore any variation of conditions I ALL rows are to be completed Consider investigating I Official websites of banks. brokers and other nancial institutions I Mortgage comparison sites such as: - htt s: www.lowestrates.c mo a e - htt s: www.ratehub.ca mo 6 es - h s: www.mtesu rmarket.ca mo 3 es Review the eight options you have explored and select one to carry forward working on in Step 4... STEP 4: PAYING OFF THE MORTGAGE Finally, applying data collected, previous decisions made and incorporating some additional considerations, students must calculate the corresponding monthly mortgage payments by using an online mortgage calculator Variations on these calculations will explore the effects of making financial planning adjustments Paying Off the Mortgage Once more a table has been provided which must be used for the completion on step 4 Refer back to previous steps to select and note the following: Select 1 Mortgage Option From Step 2 and note the Final Mortgage Amount Required : S Select 1 Final Mortgage Amount Required from step 2 Select 1 Mortgage Financing Option From Step 4 and note the Interest Rate: Select 1 Interest Rate from options in step 3 Amortization Payment Mortgage Payment Total Paid to Lender Total Interest Paid Total Interest Saved Frequency (over amortized period) (over amortized period) (over amortized period) Monthly NIA Next, you must account for: Repayment Option A: Weekly years Amortization: this is the length of time you are spreading your debt re-payment over. Weekly Shape Fill Accelerated Please refer to the class slides & textbook for more details on the legal guidelines for a Monthly NIA mortgage amortization as all three options explored must abide by legal guidelines Repayment Option B: Weekly S There are three options to be explored: years Weekly Accelerated Amortization A = legal maximum amortization for this mortgage Monthly N/A Amortization B = alternate option of your choice (must differ from others) Repayment Option C: Weekly Amortization C = alternate option of your choice (must differ from others) years Weekly Accelerated The final factor in the calculation will be: * Highlighted areas relate to instructions given on this page Payment Frequency: this is the frequency of the mortgage payments made to repay the debt. You are required to explore each of the following standard payment frequency options for each of the amortization periods: Monthly Payments Weekly Payments Accelerated Weekly PaymentsPaying Off the Mortgage Calculate your mortgage payments as well as numbers relating to the full length of the mortgage: Use a Canadian mortgage calculator. This one is recommended as it considers all listed factors and provides all required results: https://www.cchwebsites.com/content/calculators/CAMortgageLoan.html Select 1 Mortgage Option From Step 2 and note the Final Mortgage Amount Required : $_ Select 1 Mortgage Financing Option From Step 4 and note the Interest Rate: % X *this calculator ask you the enter mortgage term as well but it will have no effect on the results requested* Amortization Payment Mortgage Payment Total Paid to Lender Total Interest Paid Total Interest Saved Frequency (over amortized period) (over amortized period) (over amortized period) Canadian mortgages are regulated to limit interest compounding to semi-annually, which will differ from Monthly $XX.XX N/A payment frequency. Accounting for this difference adds a level of complication to the annuity formula that Repayment Option A: is beyond what we have studied in class, meanwhile mortgage calculators make easy work of this and are Weekly SYY . YY weekly payment savings _years a practical tool. Be sure to use a Canadian mortgage calculator. Weekly Accelerated SZZ.ZZ accelerated payment savings You will mix and match the 3 amortization options and the 3 possible payment frequencies to see what Monthly S S NIA impact these factors have on the value of the mortgage payment and the amount of interest to be paid on Repaymen the mortgage. Option B: Weekly S S years Weekly Accelerated S S For each variation you must record the following: Monthly N/A Mortgage Payment for the period Repayment Option C: Weekly S Total Paid to Lender or Total Payments (the total amount given to the lender if the mortgage _years conditions were maintained for the full amortization period. not just the term) Weekly Accelerated Total Interest Paid (the total interest paid to the lender if the mortgage conditions were maintained for the full amortization period. not just the term) *Highlighted areas relate to instructions given on this page AND example Total Interest Saved (while monthly payments pay the full amount of interest, none saved, the other two options will reveal interest saved due to that different payment frequency) The mortgage calculator tool will provide the answers to the first three columns. The fourth column, "Total Interest Saved" must be calculated by subtracting 'Total Interest Paid' with each of the other two options from 'Total Interest Paid' with the monthly payment frequency (this is the benchmark as no interest is saved with monthly payments) Example using table shown: $XX.XX - $YY.YY = weekly payment savings $XX.XX - $ZZ.ZZ = accelerated payment savings

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!