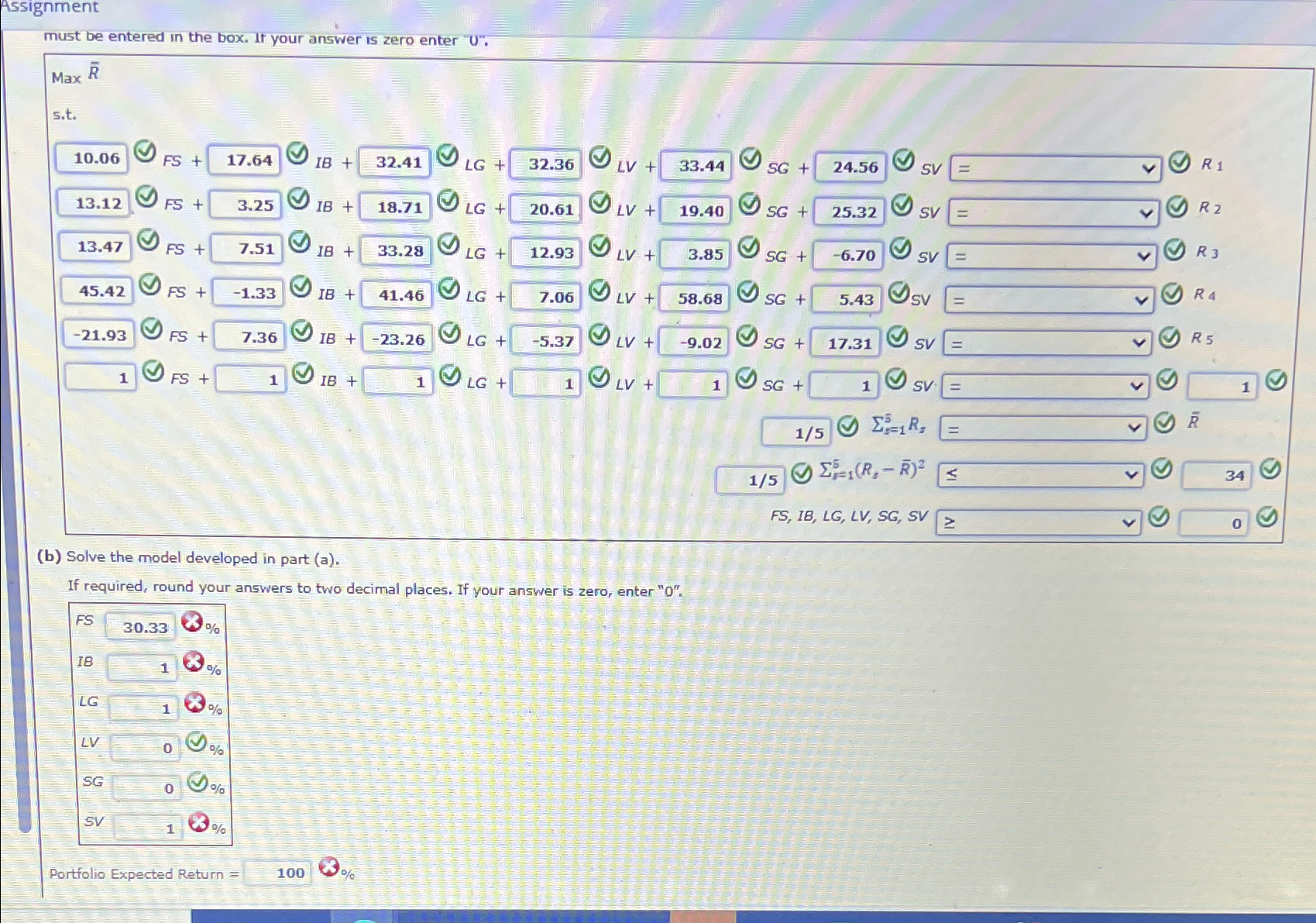

Question: Assignment must be entered in the box. If your answer is zero enter U. Max R s.t. 10.06 FS + 17.64 S IB +

Assignment must be entered in the box. If your answer is zero enter "U". Max R s.t. 10.06 FS + 17.64 S IB + 32.41 > LG + 32.36 LV + 33.44 S SG + 24.56 SV R 1 R2 13.12 FS + 3.25 IB + 18.71 13.47 FS + 7.51 IB + 33.28 45.42 FS + -1.33 IB + 41.46 LG+ 20.61 LV + 19.40 LG + 12.93 LV + > > SG + 25.32 SV = R 3 3.85 SG + -6.70 SV = R4 > LG + 7.06 LV + 58.68 SG + 5.43 sv = R5 -21.93 S FS + 7.36 > IB +-23.26 LG + -5.37 LV + -9.02 SG + 17.31 SV = 1 FS + 1 IB + 1 LG + 1 LV + 1 SG + 1 SV == (b) Solve the model developed in part (a). If required, round your answers to two decimal places. If your answer is zero, enter "0". FS 30.33 % IB 1 % LG 1 % LV 0 % SG 0 % SV 1 % Portfolio Expected Return 100 % 1/5 1/5 , 1 (RR) A 34 FS, IB, LG, LV, SG, SV > 0 S

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts