Question: Assume 0.90 for correlation coefficient. You have access to two risky assets, Stock A and Stock B. Their information is summarized as follows 7 Stock

Assume 0.90 for correlation coefficient.

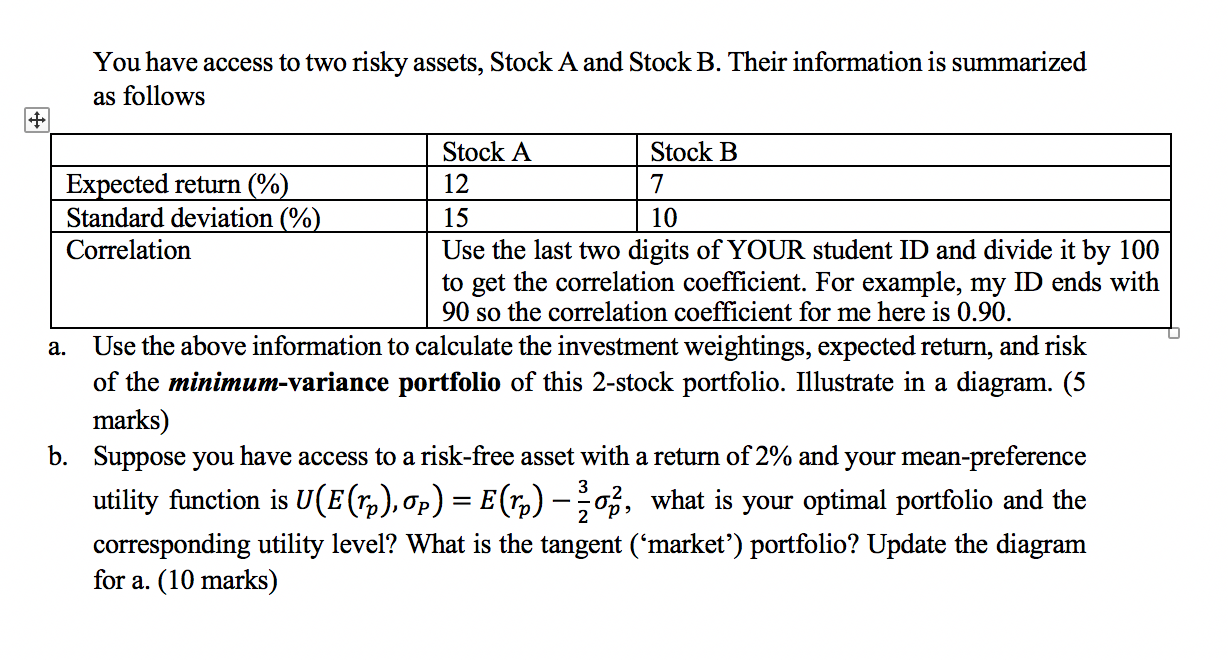

You have access to two risky assets, Stock A and Stock B. Their information is summarized as follows 7 Stock A Stock B Expected return (%) 12 Standard deviation (%) 15 10 Correlation Use the last two digits of YOUR student ID and divide it by 100 to get the correlation coefficient. For example, my ID ends with 90 so the correlation coefficient for me here is 0.90. a. Use the above information to calculate the investment weightings, expected return, and risk of the minimum-variance portfolio of this 2-stock portfolio. Illustrate in a diagram. (5 marks) Suppose you have access to a risk-free asset with a return of 2% and your mean-preference utility function is U(E(Tp), op) = E(M)-, what is your optimal portfolio and the corresponding utility level? What is the tangent (market') portfolio? Update the diagram for a. (10 marks) You have access to two risky assets, Stock A and Stock B. Their information is summarized as follows 7 Stock A Stock B Expected return (%) 12 Standard deviation (%) 15 10 Correlation Use the last two digits of YOUR student ID and divide it by 100 to get the correlation coefficient. For example, my ID ends with 90 so the correlation coefficient for me here is 0.90. a. Use the above information to calculate the investment weightings, expected return, and risk of the minimum-variance portfolio of this 2-stock portfolio. Illustrate in a diagram. (5 marks) Suppose you have access to a risk-free asset with a return of 2% and your mean-preference utility function is U(E(Tp), op) = E(M)-, what is your optimal portfolio and the corresponding utility level? What is the tangent (market') portfolio? Update the diagram for a. (10 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts