Question: Assume Carlton enters into a three - year fixed - for - fixed swap agreement to receive Swiss Franc and pay U . S .

Assume Carlton enters into a threeyear fixedforfixed swap

agreement to receive Swiss Franc and pay US dollars annually,

on a notional amount of $ The spot exchange rate at

the time of the swap is SF$ Assume that one year into the

swap agreement, Carlton decides it wishes to unwind the swap

agreement and settle it in dollars. Assuming that a twoyear

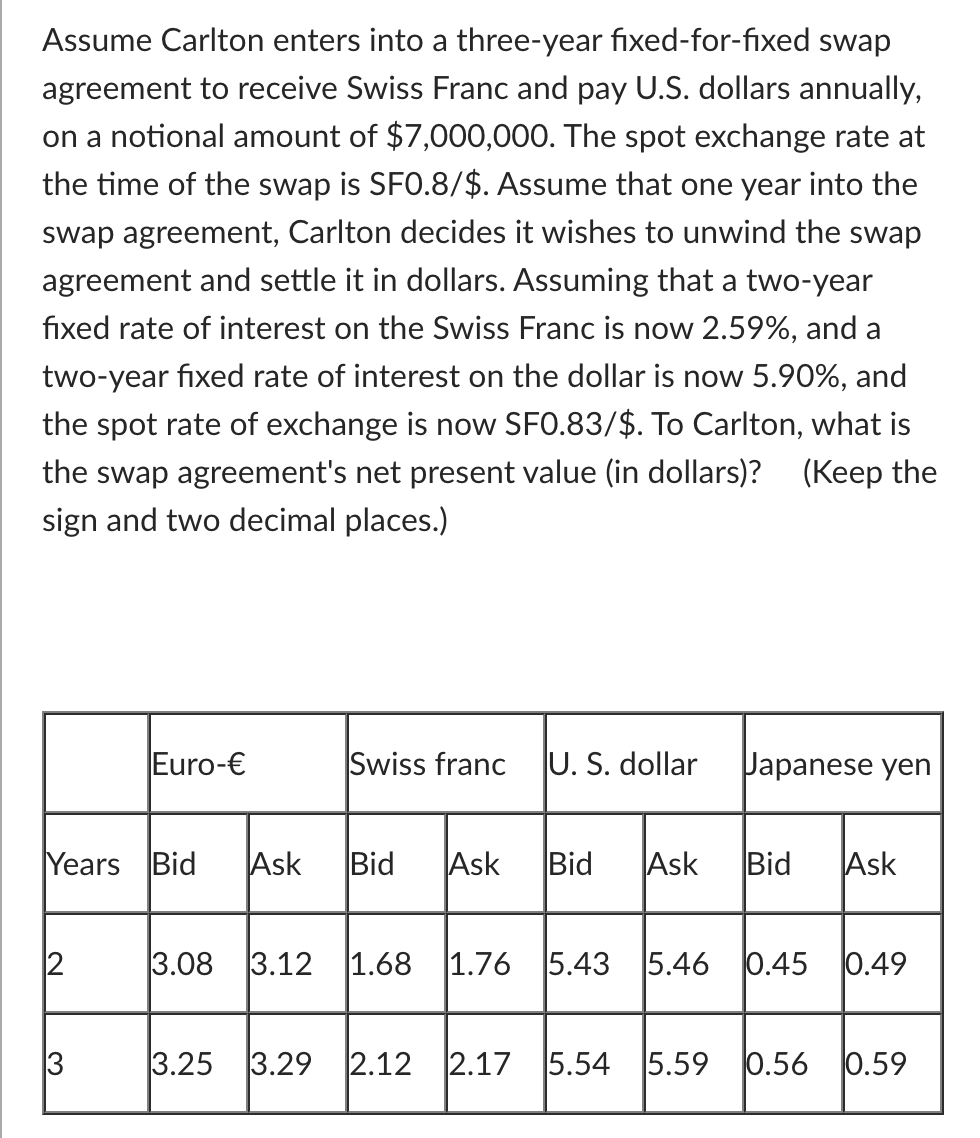

fixed rate of interest on the Swiss Franc is now and a

twoyear fixed rate of interest on the dollar is now and

the spot rate of exchange is now SF$ To Carlton, what is

the swap agreement's net present value in dollarsKeep the

sign and two decimal places.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock