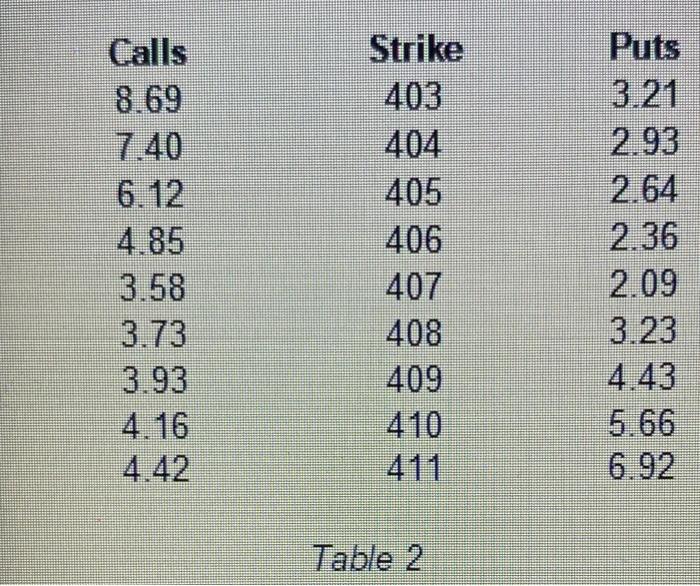

Question: Assume interest rates are 2% per year continuously compounded. Compute the Black & Scholes implied volatilities for all March call options in Table 2. Plot

Assume interest rates are 2% per year continuously compounded. Compute the Black & Scholes implied volatilities for all March call options in Table 2. Plot the implied volatilities on the y-axis and the strikes on the x-axis. comment on the graph

Table 2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock