Question: Assume security returns are generated by the single-index model. R 1 =a 1 + beta 2 R M +e 1 where R 1 is the

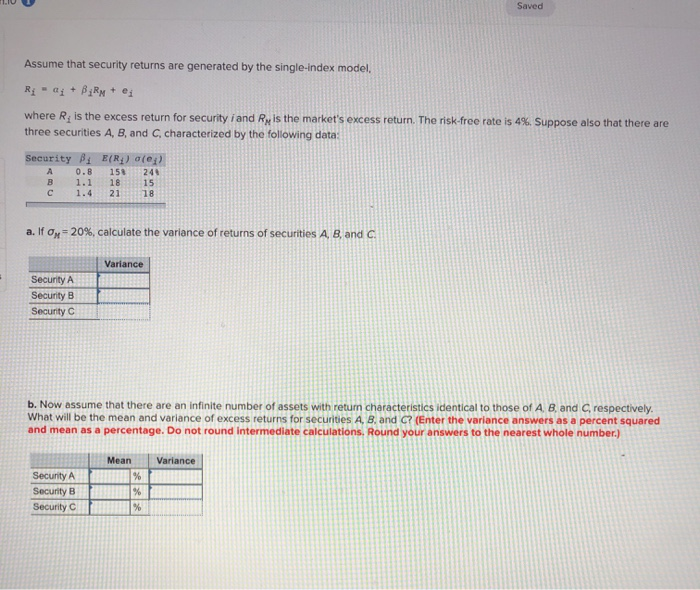

Saved Assume that security returns are generated by the single-index model R; - ei + BiRM + ej where is the excess return for security i and Ry is the market's excess return. The risk-free rate is 4%. Suppose also that there are three securities A, B, and C characterized by the following data: Security Pi E(R) Die 0.8 151 245 B 1.1 18 15 1.4 21 18 a. If Ox=20%, calculate the variance of returns of securities A, B, and C Variance Security A Security B Security C b. Now assume that there are an infinite number of assets with retur characteristics identical to those of A B, and respectively. What will be the mean and variance of excess returns for securities A Band C? (Enter the variance answers as a percent squared and mean as a percentage. Do not round Intermediate calculations. Round your answers to the nearest whole number.) Mean Variance Security A Security B Security C

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts