Question: Assume that a three-factor APT model is appropriate. The expected return on a portfolio with zero loading on all three factors is 5 percent. You

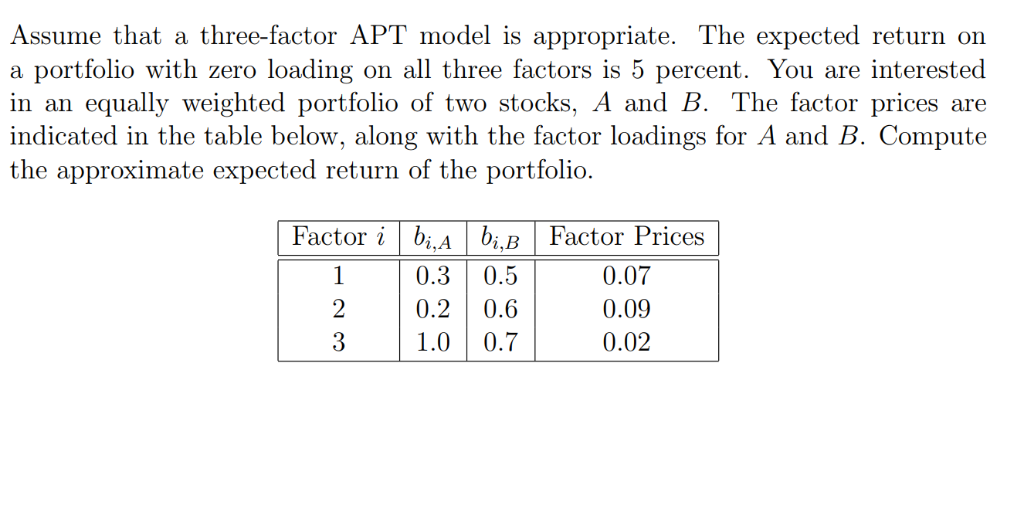

Assume that a three-factor APT model is appropriate. The expected return on a portfolio with zero loading on all three factors is 5 percent. You are interested in an equally weighted portfolio of two stocks, A and B. The factor prices are indicated in the table below, along with the factor loadings for A and B. Compute the approximate expected return of the portfolio Factor 6iA 6i.BFactor Prices 0.3 0.5 0.2 0.6 1.0 0.7 0.07 0.09 0.02

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock