Assume that the current date is 31 December 2020 Windy plc (Windy) manufactures and erects wind...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

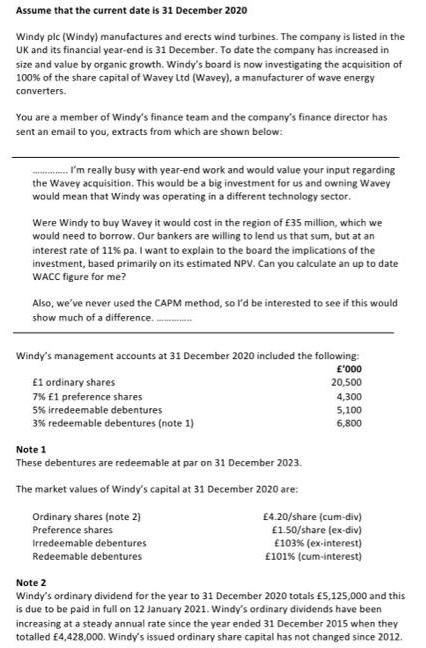

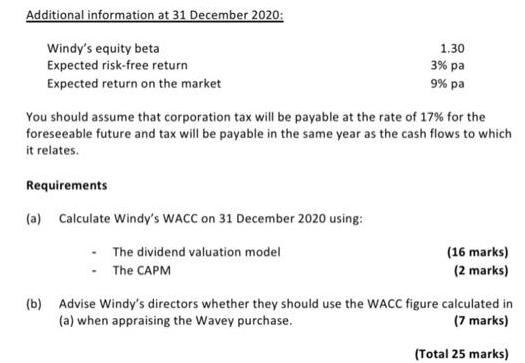

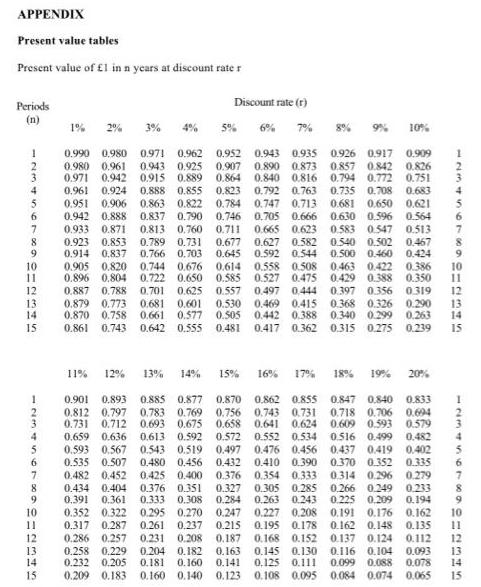

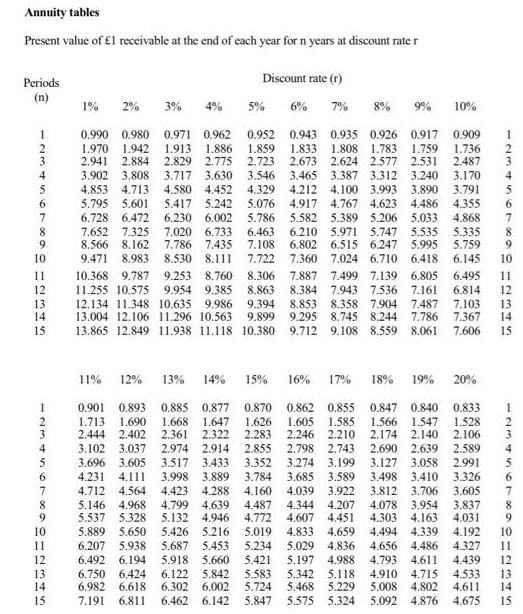

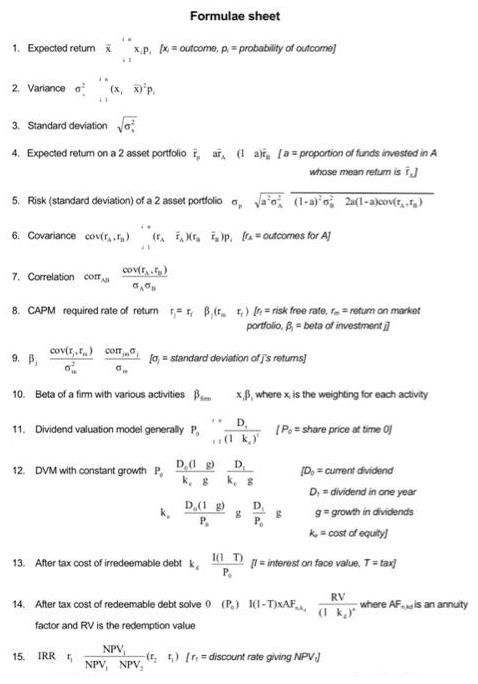

Assume that the current date is 31 December 2020 Windy plc (Windy) manufactures and erects wind turbines. The company is listed in the UK and its financial year-end is 31 December. To date the company has increased in size and value by organic growth. Windy's board is now investigating the acquisition of 100% of the share capital of Wavey Ltd (Wavey), a manufacturer of wave energy converters. You are a member of Windy's finance team and the company's finance director has sent an email to you, extracts from which are shown below: ..I'm really busy with year-end work and would value your input regarding the Wavey acquisition. This would be a big investment for us and owning Wavey would mean that Windy was operating in a different technology sector. Were Windy to buy Wavey it would cost in the region of £35 million, which we would need to borrow. Our bankers are willing to lend us that sum, but at an interest rate of 11% pa. I want to explain to the board the implications of the investment, based primarily on its estimated NPV. Can you calculate an up to date WACC figure for me? Also, we've never used the CAPM method, so I'd be interested to see if this would show much of a difference... Windy's management accounts at 31 December 2020 included the following: £'000 20,500 4,300 5,100 6,800 £1 ordinary shares 7% £1 preference shares 5% irredeemable debentures 3% redeemable debentures (note 1) Note 1 These debentures are redeemable at par on 31 December 2023. The market values of Windy's capital at 31 December 2020 are: Ordinary shares (note 2) Preference shares Irredeemable debentures Redeemable debentures £4.20/share (cum-div) £1.50/share (ex-div) £103% (ex-interest) £101% (cum-interest) Note 2 Windy's ordinary dividend for the year to 31 December 2020 totals £5,125,000 and this is due to be paid in full on 12 January 2021. Windy's ordinary dividends have been increasing at a steady annual rate since the year ended 31 December 2015 when they totalled £4,428,000. Windy's issued ordinary share capital has not changed since 2012. Additional information at 31 December 2020: Windy's equity beta Expected risk-free return Expected return on the market You should assume that corporation tax will be payable at the rate of 17% for the foreseeable future and tax will be payable in the same year as the cash flows to which it relates. Requirements 1.30 3% pa 9% pa (a) Calculate Windy's WACC on 31 December 2020 using: The dividend valuation model The CAPM (16 marks) (2 marks) (b) Advise Windy's directors whether they should use the WACC figure calculated in (a) when appraising the Wavey purchase. (7 marks) (Total 25 marks) APPENDIX Present value tables Present value of £1 in n years at discount rate r Periods 123456TDID3HS 7 8 9 10 11 1 2345678 9 10 11 12 13 14 15 1% 2% 5% 0.990 0,980 0.971 0.962 0.952 0.943 0.935 0.980 0.961 0.943 0.925 0.907 0.890 0.873 0.971 0.942 0.915 0.889 0.864 0.840 0.816 0.961 0.924 0.888 0.855 0.823 0.951 0.906 3% 0.942 0.888 0.933 0.871 0.923 0.853 0.914 0.837 0.905 0.820 0.896 0.804 0.887 0.788 0.879 0.773 0.870 0.758 0.861 0.743 Discount rate (r) 10% 0.909 0.926 0.917 0.857 0.842 0.826 0.794 0.772 0.751 0.792 0.763 0.735 0.708 0.683 0.863 0.822 0.784 0.747 0.713 0.681 0.650 0.621 0.837 0.790 0.705 0.666 0.630 0.596 0.564 0.746 0.711 0.665 0.813 0.760 0.623 0.583 0.547 0.513 0.627 0.582 0.540 0.502 0.467 0.592 0.544 0.500 0.460 0.424 0.463 0.422 0.386 10 0.429 0.388 0.350 11 0.789 0.731 0.677 0.766 0.703 0.645 0.744 0.676 0.614 0.558 0.508 0.722 0.650 0.585 0.527 0.475 0.701 0.625 0.557 0.681 0.601 0.530 0.661 0.577 0.505 0.642 0.555 0.481 0.444 0.397 0.356 0.319 12 0.290 13 14 0.315 0.275 0.239 15 15% 0.497 0.469 0.415 0.368 0.326 0.442 0.417 0.362 0.388 0.340 0.299 0.263 19% 11% 12% 13% 16% 17% 0.885 0.877 0.870 0.862 0.855 0.847 0.840 0.833 0.743 0,731 0.718 0.706 0.694 0.783 0.769 0.756 0.693 0.675 0.658 0.641 0.624 0.613 0.592 0.572 0.552 0.534 0.609 0.593 0.579 0.516 0.499 0.482 0.437 0.419 0.402 0.370 0.352 0.335 0.543 0.519 0.497 0.476 0.456 0.480 0.456 0.432 0.410 0.390 0.425 0.400 0.376 0.354 0.333 0.314 0.296 0.279 7 0.901 0.893 0.812 0.797 0.731 0.712 0.659 0.636 0.593 0.567 0.535 0.507 0.482 0.452 0.434 0.404 0.376 0.351 0.327 0.305 0.285 0.391 0.361 0.333 0.308 0.284 0.263 0.243 0.352 0.322 0.295 0.270 0.247 0.227 0.208 0.317 0.287 0.261 0.237 0.215 0.195 0.286 0.257 0.231 0.208 0.187 0.168 0.258 0.229 0.204 0.182 0.163 0.145 0.130 0.232 0.205 0.181 0.160 0.141 0.125 0.111 0.209 0.183 0.266 0.249 0.233 0.225 0.209 0.194 0.160 0.140 0.123 INSTSTODIA345 20% 0.108 0.095 0.084 0.074 8 12345678 9 0.191 0.176 0.162 10 0.178 0.162 0.148 0.135 11 0.152 0.137 0.124 0.112 0.116 0.104 0.093 0.099 0.088 0.078 0.065 D12345 Annuity tables Present value of £l receivable at the end of each year for n years at discount rate r Periods: (n) 1 2 3 8% 9% 10% 0.990 0.980 0.971 0.962 1.970 1.942 1.913 1.886 0.952 0.943 0.935 0.926 0.917 0.909 1.859 1.833 1.808 1.783 1.759 1.736 2.941 2.884 2.829 2.775 2.723 2.673 2.624 2.577 2.531 2.487 3.546 3.465 3.387 3.312 3.240 3.170 4.580 4.452 4.329 3.902 3.808 3.717 3.630 4.853 4.713 5.795 5.601 6.728 6.472 7.652 7.325 5.417 5.242 5.076 6.230 6.002 5.786 4.212 4.100 3.993 3.890 3.791 4.917 4.767 4.623 4.486 4.355 5.582 5.389 5.206 5.033 4.868 7.020 6.733 6.463 6.210 5.971 5.747 5.535 5.335 8.566 6.802 6.515 6.247 5.995 5.759 8.162 7.786 7.435 7.108 8.983 8.530 8.111 7.722 8.306 7.360 10 9.471 11 10.368 9.787 9.253 8.760 12 11.255 10.575 9.954 9.385 8.863 8.384 13 12.134 11.348 10.635 9.986 9.394 8.853 14 13.004 12.106 11.296 10.563 9.899 13.865 12.849 11.938 11.118 10.380 15 4567 8 90 H23H5 1 23456rxgnª345 7 8 10 11 12 13 14 15 1% 2% 12% 0.901 0.893 1.713 1.690 2.444 2.402 3.102 3.037 3.696 3.605 4.231 4.111 11% 3% 4% 4.712 4.564 5.146 4.968 5.537 5.328 Discount rate (r) 7% 5.889 5.650 6.207 5.938 6.492 6.194 5% 13% 14% 0.885 0.877 1.668 1.647 2.361 2.322 2.974 2.914 2.855 3.517 3.433 3.352 3.998 3.889 3.784 4.423 4.288 4.160 4.799 4.639 4.487 4.344 4.772 4.607 5.132 4.946 5.019 5.426 5.216 5.687 5.453 5.234 5.918 5.660 6.122 5.842 5.583 5.421 6.750 6.424 6.982 6.618 6.302 6.002 5.724 7.191 6.811 6.462 6.142 5.847 8.358 9.295 8.745 15% 0.870 0.833 1.626 1.528 2.283 2.246 2.210 2.798 2.743 2.174 2.140 2.106 2.690 2.639 2.589 3.127 3.058 2.991 3.274 3.199 3.685 3.589 3.498 3.410 3.326 4.039 3.922 3.812 3.706 3.605 16% 17% 18% 19% 0.862 0.855 0.847 0.840 1.605 1.585 1.566 1.547 7.024 6.710 6.418 6.145 10 7.887 7.499 7.139 6.805 6.495 11 7.943 7.536 7.161 6.814 12 7.904 7.487 7.103 13 8.244 7.786 7.367 14 9.712 9.108 8.559 8.061 7.606 15 12345or∞a012 20% 4.207 4.078 3.954 3.837 4.451 4.303 4.163 4.031 6 5.342 5.118 5.468 5.229 5.575 5.324 7 8 9 123456rxagILMAS 7 8 9 4.833 4.659 4.494 4.339 4.192 10 5.029 4.836 4.656 4.486 4.327 11 5.197 4.988 4.793 4.611 4.439 12 4.910 4.715 4.533 5.008 4.802 4.611 14 5.092 4.876 4.675 15 1. Expected return x 2. Variance 3. Standard deviation √ 4. Expected return on a 2 asset portfolio , ar, (1 a) [a=proportion of funds invested in A whose mean return is i IN 5. Risk (standard deviation) of a 2 asset portfolio a, √a' (1-a) 2a(1-a)cov(r,.₂) 7. Correlation com Formulae sheet in x.p. [x = outcome, p = probability of outcome] 41 6. Covariance cov(r.) 9. B, (x, x)³p. T. cov(r.) com 15. 8. CAPM required rate of return = B( ) [= risk free rate, return on market portfolio, B = beta of investment i [a, = standard deviation of j's returns] (FFM ₂)p. [= outcomes for A] #1 cov(r...) IRR 5₁ ܘܢܘ 10. Beta of a firm with various activities ... 11. Dividend valuation model generally P 12. DVM with constant growth P 13. After tax cost of irredeemable debt k D. (1 g) k, g IN D, (1 k D.(1 g) P₁ x3, where x is the weighting for each activity [P, =share price at time 01 1(1 T) P₁ [D, = current dividend D,= dividend in one year g=growth in dividends k. = cost of equity] [1=interest on face value. T=tax] RV 14. After tax cost of redeemable debt solve 0 (P₁) (1-T)XAF. (1 kg) where AF is an annuity factor and RV is the redemption value NPV₁ NPV, NPV, 8 (₂5) [r₁=discount rate giving NPV) Assume that the current date is 31 December 2020 Windy plc (Windy) manufactures and erects wind turbines. The company is listed in the UK and its financial year-end is 31 December. To date the company has increased in size and value by organic growth. Windy's board is now investigating the acquisition of 100% of the share capital of Wavey Ltd (Wavey), a manufacturer of wave energy converters. You are a member of Windy's finance team and the company's finance director has sent an email to you, extracts from which are shown below: ..I'm really busy with year-end work and would value your input regarding the Wavey acquisition. This would be a big investment for us and owning Wavey would mean that Windy was operating in a different technology sector. Were Windy to buy Wavey it would cost in the region of £35 million, which we would need to borrow. Our bankers are willing to lend us that sum, but at an interest rate of 11% pa. I want to explain to the board the implications of the investment, based primarily on its estimated NPV. Can you calculate an up to date WACC figure for me? Also, we've never used the CAPM method, so I'd be interested to see if this would show much of a difference... Windy's management accounts at 31 December 2020 included the following: £'000 20,500 4,300 5,100 6,800 £1 ordinary shares 7% £1 preference shares 5% irredeemable debentures 3% redeemable debentures (note 1) Note 1 These debentures are redeemable at par on 31 December 2023. The market values of Windy's capital at 31 December 2020 are: Ordinary shares (note 2) Preference shares Irredeemable debentures Redeemable debentures £4.20/share (cum-div) £1.50/share (ex-div) £103% (ex-interest) £101% (cum-interest) Note 2 Windy's ordinary dividend for the year to 31 December 2020 totals £5,125,000 and this is due to be paid in full on 12 January 2021. Windy's ordinary dividends have been increasing at a steady annual rate since the year ended 31 December 2015 when they totalled £4,428,000. Windy's issued ordinary share capital has not changed since 2012. Additional information at 31 December 2020: Windy's equity beta Expected risk-free return Expected return on the market You should assume that corporation tax will be payable at the rate of 17% for the foreseeable future and tax will be payable in the same year as the cash flows to which it relates. Requirements 1.30 3% pa 9% pa (a) Calculate Windy's WACC on 31 December 2020 using: The dividend valuation model The CAPM (16 marks) (2 marks) (b) Advise Windy's directors whether they should use the WACC figure calculated in (a) when appraising the Wavey purchase. (7 marks) (Total 25 marks) APPENDIX Present value tables Present value of £1 in n years at discount rate r Periods 123456TDID3HS 7 8 9 10 11 1 2345678 9 10 11 12 13 14 15 1% 2% 5% 0.990 0,980 0.971 0.962 0.952 0.943 0.935 0.980 0.961 0.943 0.925 0.907 0.890 0.873 0.971 0.942 0.915 0.889 0.864 0.840 0.816 0.961 0.924 0.888 0.855 0.823 0.951 0.906 3% 0.942 0.888 0.933 0.871 0.923 0.853 0.914 0.837 0.905 0.820 0.896 0.804 0.887 0.788 0.879 0.773 0.870 0.758 0.861 0.743 Discount rate (r) 10% 0.909 0.926 0.917 0.857 0.842 0.826 0.794 0.772 0.751 0.792 0.763 0.735 0.708 0.683 0.863 0.822 0.784 0.747 0.713 0.681 0.650 0.621 0.837 0.790 0.705 0.666 0.630 0.596 0.564 0.746 0.711 0.665 0.813 0.760 0.623 0.583 0.547 0.513 0.627 0.582 0.540 0.502 0.467 0.592 0.544 0.500 0.460 0.424 0.463 0.422 0.386 10 0.429 0.388 0.350 11 0.789 0.731 0.677 0.766 0.703 0.645 0.744 0.676 0.614 0.558 0.508 0.722 0.650 0.585 0.527 0.475 0.701 0.625 0.557 0.681 0.601 0.530 0.661 0.577 0.505 0.642 0.555 0.481 0.444 0.397 0.356 0.319 12 0.290 13 14 0.315 0.275 0.239 15 15% 0.497 0.469 0.415 0.368 0.326 0.442 0.417 0.362 0.388 0.340 0.299 0.263 19% 11% 12% 13% 16% 17% 0.885 0.877 0.870 0.862 0.855 0.847 0.840 0.833 0.743 0,731 0.718 0.706 0.694 0.783 0.769 0.756 0.693 0.675 0.658 0.641 0.624 0.613 0.592 0.572 0.552 0.534 0.609 0.593 0.579 0.516 0.499 0.482 0.437 0.419 0.402 0.370 0.352 0.335 0.543 0.519 0.497 0.476 0.456 0.480 0.456 0.432 0.410 0.390 0.425 0.400 0.376 0.354 0.333 0.314 0.296 0.279 7 0.901 0.893 0.812 0.797 0.731 0.712 0.659 0.636 0.593 0.567 0.535 0.507 0.482 0.452 0.434 0.404 0.376 0.351 0.327 0.305 0.285 0.391 0.361 0.333 0.308 0.284 0.263 0.243 0.352 0.322 0.295 0.270 0.247 0.227 0.208 0.317 0.287 0.261 0.237 0.215 0.195 0.286 0.257 0.231 0.208 0.187 0.168 0.258 0.229 0.204 0.182 0.163 0.145 0.130 0.232 0.205 0.181 0.160 0.141 0.125 0.111 0.209 0.183 0.266 0.249 0.233 0.225 0.209 0.194 0.160 0.140 0.123 INSTSTODIA345 20% 0.108 0.095 0.084 0.074 8 12345678 9 0.191 0.176 0.162 10 0.178 0.162 0.148 0.135 11 0.152 0.137 0.124 0.112 0.116 0.104 0.093 0.099 0.088 0.078 0.065 D12345 Annuity tables Present value of £l receivable at the end of each year for n years at discount rate r Periods: (n) 1 2 3 8% 9% 10% 0.990 0.980 0.971 0.962 1.970 1.942 1.913 1.886 0.952 0.943 0.935 0.926 0.917 0.909 1.859 1.833 1.808 1.783 1.759 1.736 2.941 2.884 2.829 2.775 2.723 2.673 2.624 2.577 2.531 2.487 3.546 3.465 3.387 3.312 3.240 3.170 4.580 4.452 4.329 3.902 3.808 3.717 3.630 4.853 4.713 5.795 5.601 6.728 6.472 7.652 7.325 5.417 5.242 5.076 6.230 6.002 5.786 4.212 4.100 3.993 3.890 3.791 4.917 4.767 4.623 4.486 4.355 5.582 5.389 5.206 5.033 4.868 7.020 6.733 6.463 6.210 5.971 5.747 5.535 5.335 8.566 6.802 6.515 6.247 5.995 5.759 8.162 7.786 7.435 7.108 8.983 8.530 8.111 7.722 8.306 7.360 10 9.471 11 10.368 9.787 9.253 8.760 12 11.255 10.575 9.954 9.385 8.863 8.384 13 12.134 11.348 10.635 9.986 9.394 8.853 14 13.004 12.106 11.296 10.563 9.899 13.865 12.849 11.938 11.118 10.380 15 4567 8 90 H23H5 1 23456rxgnª345 7 8 10 11 12 13 14 15 1% 2% 12% 0.901 0.893 1.713 1.690 2.444 2.402 3.102 3.037 3.696 3.605 4.231 4.111 11% 3% 4% 4.712 4.564 5.146 4.968 5.537 5.328 Discount rate (r) 7% 5.889 5.650 6.207 5.938 6.492 6.194 5% 13% 14% 0.885 0.877 1.668 1.647 2.361 2.322 2.974 2.914 2.855 3.517 3.433 3.352 3.998 3.889 3.784 4.423 4.288 4.160 4.799 4.639 4.487 4.344 4.772 4.607 5.132 4.946 5.019 5.426 5.216 5.687 5.453 5.234 5.918 5.660 6.122 5.842 5.583 5.421 6.750 6.424 6.982 6.618 6.302 6.002 5.724 7.191 6.811 6.462 6.142 5.847 8.358 9.295 8.745 15% 0.870 0.833 1.626 1.528 2.283 2.246 2.210 2.798 2.743 2.174 2.140 2.106 2.690 2.639 2.589 3.127 3.058 2.991 3.274 3.199 3.685 3.589 3.498 3.410 3.326 4.039 3.922 3.812 3.706 3.605 16% 17% 18% 19% 0.862 0.855 0.847 0.840 1.605 1.585 1.566 1.547 7.024 6.710 6.418 6.145 10 7.887 7.499 7.139 6.805 6.495 11 7.943 7.536 7.161 6.814 12 7.904 7.487 7.103 13 8.244 7.786 7.367 14 9.712 9.108 8.559 8.061 7.606 15 12345or∞a012 20% 4.207 4.078 3.954 3.837 4.451 4.303 4.163 4.031 6 5.342 5.118 5.468 5.229 5.575 5.324 7 8 9 123456rxagILMAS 7 8 9 4.833 4.659 4.494 4.339 4.192 10 5.029 4.836 4.656 4.486 4.327 11 5.197 4.988 4.793 4.611 4.439 12 4.910 4.715 4.533 5.008 4.802 4.611 14 5.092 4.876 4.675 15 1. Expected return x 2. Variance 3. Standard deviation √ 4. Expected return on a 2 asset portfolio , ar, (1 a) [a=proportion of funds invested in A whose mean return is i IN 5. Risk (standard deviation) of a 2 asset portfolio a, √a' (1-a) 2a(1-a)cov(r,.₂) 7. Correlation com Formulae sheet in x.p. [x = outcome, p = probability of outcome] 41 6. Covariance cov(r.) 9. B, (x, x)³p. T. cov(r.) com 15. 8. CAPM required rate of return = B( ) [= risk free rate, return on market portfolio, B = beta of investment i [a, = standard deviation of j's returns] (FFM ₂)p. [= outcomes for A] #1 cov(r...) IRR 5₁ ܘܢܘ 10. Beta of a firm with various activities ... 11. Dividend valuation model generally P 12. DVM with constant growth P 13. After tax cost of irredeemable debt k D. (1 g) k, g IN D, (1 k D.(1 g) P₁ x3, where x is the weighting for each activity [P, =share price at time 01 1(1 T) P₁ [D, = current dividend D,= dividend in one year g=growth in dividends k. = cost of equity] [1=interest on face value. T=tax] RV 14. After tax cost of redeemable debt solve 0 (P₁) (1-T)XAF. (1 kg) where AF is an annuity factor and RV is the redemption value NPV₁ NPV, NPV, 8 (₂5) [r₁=discount rate giving NPV)

Expert Answer:

Answer rating: 100% (QA)

The answer is below provided step by step manner a Dividend valuation model D0 1gkeg Po D0 14114 420 ... View the full answer

Posted Date:

Students also viewed these business communication questions

-

Assume that the current spot rates are as follows: Years from Today Spot Rate 1.....................................8% 2.......................................9...

-

Assume that the current stock price is $50 per share, that call options can be purchased with an exercise price of $60 per share that bank loans can be obtained for a 10 percent nominal rate and that...

-

Assume that the current price of a stock is $100. A call option (#1) on that stock with an exercise price of $97 costs $7. A call option (#2) on the stock with the same expiration and an exercise...

-

1. Which type contains a single character enclosed within single quotes? A. Character B. Numeric C. Floating point 2. The modulus operator uses, B. - B. < A. + 3. Every variable should be separated...

-

A manager of an industrial plant asserts that workers on average do not complete a job using Method A in the same amount of time as they would using Method B. Seven workers are randomly selected....

-

Figure gives the potential energy U of a magnetic dipole in an external magnetic field B, as a function of angle between the directions of B and the dipole moment. The vertical axis scale is set by...

-

Refer to the data given for the Pruitt Company in Problem P12-3A. Required a. Compute the change in cash that occurred in 2019. b. Prepare a statement of cash flows using the direct method. Use one...

-

Sherry Rudd recently inherited a trust fund from a distant relative. On January 2, the bank managing the trust fund notified Rudd that she has the option of receiving a lump-sum check for $200,000 or...

-

11. (12 points) Profit on Option You have purchased a call option contract on Dash common stock. The option has an exercise price of $32.00 and Dash's stock currently trades at $30.00. The option...

-

Palisade Creek Co. is a merchandising business. The account balances for Palisade Creek Co. as of May 1, 2014 (unless otherwise indicated), are as follows: During May, the last month of the fiscal...

-

Find fourth derivative of the following function.5 y = 3x - 4x + 7x + 10 O 10 1 O O O 7x

-

A steel mono-pile needs to be constructed to hold a monitoring station. The monitoring station should be 20 feet above the still water level, SWL, of 55 feet. The superstructure including the...

-

Explain the advantages and disadvantages inherent in each of the four business forms with regard to contract creation, negotiation, and approval of contracts.

-

1) What is Philosophy? Do you have a personal philosophy in life? If so, what is your personal philosophy? 2) Differentiate ethics from morality. 3) Why is ethics called a normative science?...

-

At gunpoint, a convenience shop was robbed in the middle of the day. The culprit was seen on the store's security camera, and a composite sketch was created from the footage. The owner of the...

-

Assume Ganado enters into a swap agreement to receive euros and pay Japanese yen, on a notional principal of 5,000,000. The spot exchange rate at the time of the swap is 104/. (When you answer the...

-

When are inside directors beneficial to the functioning of the board of directors? What are the three primary roles played by boards? How do boards carry out these roles? What is the difference...

-

Find the intercepts and then graph the line. (a) 2x - 3y = 6 (b) 10 - 5x = 2y

-

Donald Winn and Judy Reed agreed to liquidate their partnership on June 30 of the current year. On that date, after financial statements were prepared and closing entries were posted, the general...

-

Theresa Doran and Roy Eden are partners in a business called D & E Sales. The partnership's work sheet for the year ended December 31 of the current year is provided in the Working Papers. ...

-

Brian Hughes and Wendy Perez formed a partnership five years ago. The partnership has been very successful and is growing rapidly. The partners are evaluating future actions for the next five years....

Study smarter with the SolutionInn App