Question: Assume that the current exchange rate is $0.90/ using the following table of information. Suppose that oil forward prices for 1 year, 2 years, and

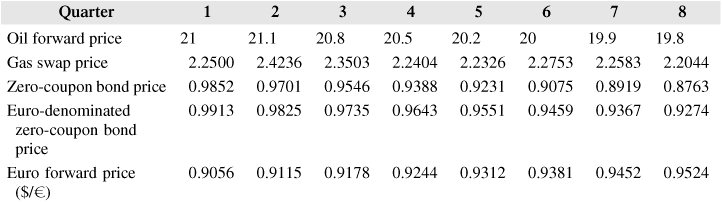

Assume that the current exchange rate is $0.90/ using the following table of information.

- Suppose that oil forward prices for 1 year, 2 years, and 3 years are $20, $21, and $22. The 1-year effective annual interest rate is 6.0%, the 2-year interest is 6.5% and 3-year interest is 7%, what is the 3-year SWAP price?

- Supposing the effective quarterly interest rate is 1.5%, what are the per-barrel swap prices for 4-quarter and 8-quarter oil swaps? (Use oil forward prices in table) What is the total cost of prepaid 4- and 8-quarter swaps?

- Using the information about zero-coupon bond prices and oil forward prices in table, construct the set of swap prices for oil for 1 through 8 quarters.

- Using the information in table, what is the swap price of a 4-quarter oil swap with the first settlement occurring in the third quarter?

4 5 6 7 8 Quarter 1 2 Oil forward price 21 21.1 Gas swap price 2.2500 2.4236 Zero-coupon bond price 0.9852 0.9701 Euro-denominated 0.9913 0.9825 zero-coupon bond price Euro forward price 0.9056 0.9115 ($/) 3 20.8 2.3503 0.9546 0.9735 20.5 2.2404 0.9388 0.9643 20.2 2.2326 0.9231 0.9551 20 2.2753 0.9075 0.9459 19.9 2.2583 0.8919 0.9367 19.8 2.2044 0.8763 0.9274 0.9178 0.9244 0.9312 0.9381 0.9452 0.9524 4 5 6 7 8 Quarter 1 2 Oil forward price 21 21.1 Gas swap price 2.2500 2.4236 Zero-coupon bond price 0.9852 0.9701 Euro-denominated 0.9913 0.9825 zero-coupon bond price Euro forward price 0.9056 0.9115 ($/) 3 20.8 2.3503 0.9546 0.9735 20.5 2.2404 0.9388 0.9643 20.2 2.2326 0.9231 0.9551 20 2.2753 0.9075 0.9459 19.9 2.2583 0.8919 0.9367 19.8 2.2044 0.8763 0.9274 0.9178 0.9244 0.9312 0.9381 0.9452 0.9524

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts