Question: Assume you are constructing the efficient portfolio frontier with three risky stocks A, B, and C as follows. Without any calculations, answer the two questions

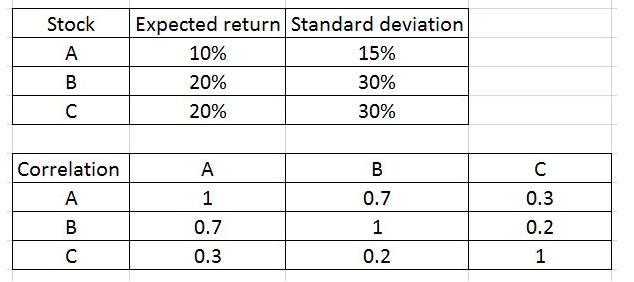

Assume you are constructing the efficient portfolio frontier with three risky stocks A, B, and C as follows.

Without any calculations, answer the two questions below and briefly explain. [An answer without any explanations will receive a mark of zero]

1) Assume a portfolio on the frontier has an expected return of 12.5%. Between B and C, which stock is given a higher weight?

2) Assume another portfolio on the frontier has an expected return of 20%. Between B and C, which stock is given a higher weight in this frontier portfolio this time?

Stock . Expected return Standard deviation 10% 15% 20% 30% 20% 30% B . B Correlation A 0.7 1 0.7 0.3 0.2 1 B 1 0.2 C 0.3 Stock . Expected return Standard deviation 10% 15% 20% 30% 20% 30% B . B Correlation A 0.7 1 0.7 0.3 0.2 1 B 1 0.2 C 0.3

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts