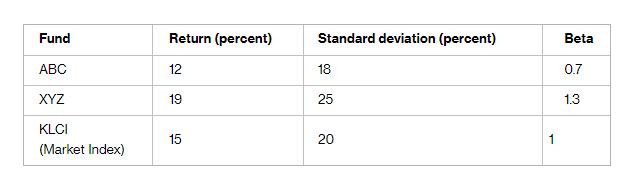

Assuming the risk-free rate is 7 percent, calculate Sharpe ratios for ABC, XYZ and KLCI. Compare the

Fantastic news! We've Found the answer you've been seeking!

Question:

Compare the performance of ABC and XYZ relative to the market index based on the answer in (a).

Assuming the risk-free rate is 7 percent, calculate Treynor's ratio for ABC, XYZ, and KLCI.

State the differences between the two measurements.

If the actual returns realized from ABC and XYZ funds are 12 and 19 percent respectively, given that the market return is 15 percent and beta is 0.7 and 1.3, calculate the expected return for both funds.

Calculate the differential return or alpha value for ABC and XYZ funds.

Expert Answer:

Sharpe Ratio Return of the fund Riskfree rate Standard deviation of the fund Calculation of the Shar... View the full answer

Related Book For

Fundamentals of Financial Management

ISBN: 978-1337395250

15th edition

Authors: Eugene F. Brigham, Joel F. Houston

Posted Date: