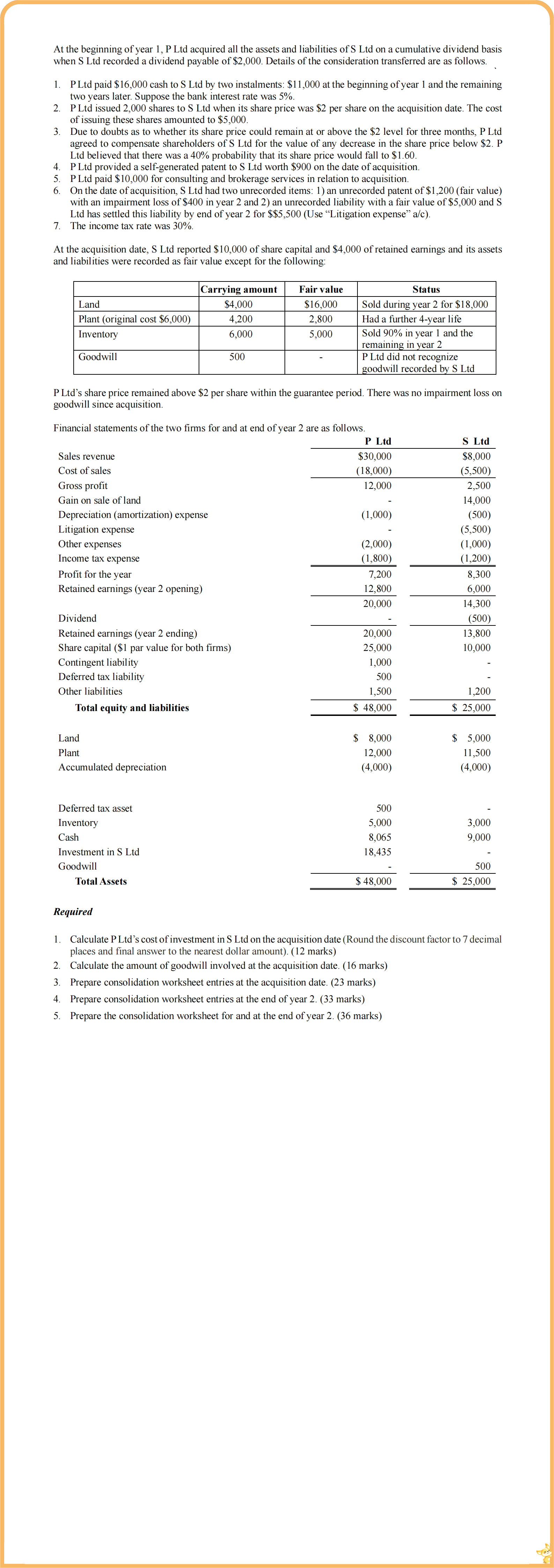

At the beginning of year 1, P Ltd acquired all the assets and liabilities of S...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

At the beginning of year 1, P Ltd acquired all the assets and liabilities of S Ltd on a cumulative dividend basis when S Ltd recorded a dividend payable of $2,000. Details of the consideration transferred are as follows. 1. PLtd paid $16,000 cash to S Ltd by two instalments: $11,000 at the beginning of year 1 and the remaining two years later. Suppose the bank interest rate was 5%. 2. P Ltd issued 2,000 shares to S Ltd when its share price was $2 per share on the acquisition date. The cost of issuing these shares amounted to $5,000. 3. Due to doubts as to whether its share price could remain at or above the $2 level for three months, P Ltd agreed to compensate shareholders of S Ltd for the value of any decrease in the share price below $2. P Ltd believed that there was a 40% probability that its share price would fall to $1.60. 4. P Ltd provided a self-generated patent to S Ltd worth $900 on the date of acquisition. 5. P Ltd paid $10,000 for consulting and brokerage services in relation to acquisition. 6. On the date of acquisition, S Ltd had two unrecorded items: 1) an unrecorded patent of $1,200 (fair value) with an impairment loss of $400 in year 2 and 2) an unrecorded liability with a fair value of $5,000 and S Ltd has settled this liability by end of year 2 for $$5,500 (Use Litigation expense a/c). 7. The income tax rate was 30%. At the acquisition date, S Ltd reported $10,000 of share capital and $4,000 of retained earnings and its assets and liabilities were recorded as fair value except for the following: Carrying amount Fair value Land $4,000 $16,000 Status Sold during year 2 for $18,000 Plant (original cost $6,000) 4,200 2,800 Had a further 4-year life Inventory 6,000 5,000 Sold 90% in year 1 and the remaining in year 2 Goodwill 500 P Ltd did not recognize goodwill recorded by S Ltd P Ltd's share price remained above $2 per share within the guarantee period. There was no impairment loss on goodwill since acquisition. Financial statements of the two firms for and at end of year 2 are as follows. P Ltd S Ltd Sales revenue $30,000 $8,000 Cost of sales (18,000) (5,500) Gross profit 12,000 2,500 Gain on sale of land 14,000 Depreciation (amortization) expense (1,000) (500) Litigation expense (5,500) Other expenses (2,000) (1,000) Income tax expense (1,800) (1,200) Profit for the year 7,200 8,300 Retained earnings (year 2 opening) 12,800 6,000 20,000 14,300 Dividend (500) Retained earnings (year 2 ending) 20,000 13,800 Share capital ($1 par value for both firms) 25,000 10,000 Contingent liability 1,000 Deferred tax liability 500 Other liabilities 1,500 1,200 Total equity and liabilities $ 48,000 $ 25,000 Land Plant Accumulated depreciation $ 8,000 12,000 (4,000) $ 5,000 11,500 (4,000) Deferred tax asset Inventory Cash Investment in S Ltd Goodwill Total Assets Required 500 5,000 3,000 8,065 9,000 18,435 500 $ 48,000 $ 25,000 1. Calculate P Ltd's cost of investment in S Ltd on the acquisition date (Round the discount factor to 7 decimal places and final answer to the nearest dollar amount). (12 marks) 2. Calculate the amount of goodwill involved at the acquisition date. (16 marks) 3. Prepare consolidation worksheet entries at the acquisition date. (23 marks) 4. Prepare consolidation worksheet entries at the end of year 2. (33 marks) 5. Prepare the consolidation worksheet for and at the end of year 2. (36 marks) At the beginning of year 1, P Ltd acquired all the assets and liabilities of S Ltd on a cumulative dividend basis when S Ltd recorded a dividend payable of $2,000. Details of the consideration transferred are as follows. 1. PLtd paid $16,000 cash to S Ltd by two instalments: $11,000 at the beginning of year 1 and the remaining two years later. Suppose the bank interest rate was 5%. 2. P Ltd issued 2,000 shares to S Ltd when its share price was $2 per share on the acquisition date. The cost of issuing these shares amounted to $5,000. 3. Due to doubts as to whether its share price could remain at or above the $2 level for three months, P Ltd agreed to compensate shareholders of S Ltd for the value of any decrease in the share price below $2. P Ltd believed that there was a 40% probability that its share price would fall to $1.60. 4. P Ltd provided a self-generated patent to S Ltd worth $900 on the date of acquisition. 5. P Ltd paid $10,000 for consulting and brokerage services in relation to acquisition. 6. On the date of acquisition, S Ltd had two unrecorded items: 1) an unrecorded patent of $1,200 (fair value) with an impairment loss of $400 in year 2 and 2) an unrecorded liability with a fair value of $5,000 and S Ltd has settled this liability by end of year 2 for $$5,500 (Use Litigation expense a/c). 7. The income tax rate was 30%. At the acquisition date, S Ltd reported $10,000 of share capital and $4,000 of retained earnings and its assets and liabilities were recorded as fair value except for the following: Carrying amount Fair value Land $4,000 $16,000 Status Sold during year 2 for $18,000 Plant (original cost $6,000) 4,200 2,800 Had a further 4-year life Inventory 6,000 5,000 Sold 90% in year 1 and the remaining in year 2 Goodwill 500 P Ltd did not recognize goodwill recorded by S Ltd P Ltd's share price remained above $2 per share within the guarantee period. There was no impairment loss on goodwill since acquisition. Financial statements of the two firms for and at end of year 2 are as follows. P Ltd S Ltd Sales revenue $30,000 $8,000 Cost of sales (18,000) (5,500) Gross profit 12,000 2,500 Gain on sale of land 14,000 Depreciation (amortization) expense (1,000) (500) Litigation expense (5,500) Other expenses (2,000) (1,000) Income tax expense (1,800) (1,200) Profit for the year 7,200 8,300 Retained earnings (year 2 opening) 12,800 6,000 20,000 14,300 Dividend (500) Retained earnings (year 2 ending) 20,000 13,800 Share capital ($1 par value for both firms) 25,000 10,000 Contingent liability 1,000 Deferred tax liability 500 Other liabilities 1,500 1,200 Total equity and liabilities $ 48,000 $ 25,000 Land Plant Accumulated depreciation $ 8,000 12,000 (4,000) $ 5,000 11,500 (4,000) Deferred tax asset Inventory Cash Investment in S Ltd Goodwill Total Assets Required 500 5,000 3,000 8,065 9,000 18,435 500 $ 48,000 $ 25,000 1. Calculate P Ltd's cost of investment in S Ltd on the acquisition date (Round the discount factor to 7 decimal places and final answer to the nearest dollar amount). (12 marks) 2. Calculate the amount of goodwill involved at the acquisition date. (16 marks) 3. Prepare consolidation worksheet entries at the acquisition date. (23 marks) 4. Prepare consolidation worksheet entries at the end of year 2. (33 marks) 5. Prepare the consolidation worksheet for and at the end of year 2. (36 marks)

Expert Answer:

Related Book For

Advanced Accounting

ISBN: 9780132568968

11th Edition

Authors: Floyd A. Beams, Joseph H. Anthony, Bruce Bettinghaus, Kenneth Smith

Posted Date:

Students also viewed these accounting questions

-

Question 4 The following is the baseline case that we have for Albion Computers in the class, where the exchange rate will remain at $/=1.60: Sales (50,000 units at 1,000/unit) Variable costs (50,000...

-

What is the Consumer Price Index (CPI)? Select one of the reports available at www.bls.gov/cpi/home.htm and create a presentation on price changes over the past two years. Discuss reasons for that...

-

The small steel plate is connected to the right angle bracket by a 10-mm diameter bolt (Figure P5.20). Determine the tensile stress at point A in the plate and the shear stress in the bolt. Figure...

-

For approximately 20 months, Robert E. McDonald perpetrated a scheme to solicit millions of dollars purportedly for a \($100\) million purchase by the RAI Entities and certain other related corporate...

-

Lawrence Industries most recent annual dividend was $1.80 per share (D 0 = $1.80), and the firms required return is 11%. Find the market value of Lawrences shares when: a. Dividends are expected to...

-

3. (25 points) Consider two firms out of a competitive industry. They have the following technologies: C(y) = y + 2y; C2(y) = 1.5y + 3y. Show these firms' individual supply functions on a...

-

Check the strain control F2 F3 F= 5LN E- 2 LN 5- 2 LN Mb= 500 Nm (c-D arainta) Song - 2 Mil Mz: Ck 22 Fi etkili 220 180 Snfta Me hesapland. Devamnda gerilme kontroln yapnz. 100 60 040

-

Amanda leased equipment worth $40,000 for 7 years. If the cost of borrowing is 5.76% compounded monthly, calculate the size of the lease payment that is required to be made at the beginning of each...

-

Last year, California Sushi and Such (CSS) had sales of $65 million. The firm's operating expenses amounted to $20 million and costs of goods sold totaled $15 million. In addition, CSS received...

-

Assume the total cost of a college education will be $235,000 when your child enters college in 18 years. You presently have $35,000 to invest. What annual rate of interest must you earn on your...

-

Louis is 25 years old and has a dream of having $1,000,000 in his investment account by the time he turns 50. If he invests in a fund that returns 5% per year (and compounds daily), how much does he...

-

Question 1 One year from today, investors anticipate that Amazing Inc. stock will pay a dividend of $3.25 per share. After that, investors believe that the dividend will grow at 20% per year for...

-

Suppose that the demand for cigarettes and supply of cigarettes in a hypothetical country are as follows: QD = 2000-200P QS = 200P Where QD is the number of packs demanded and P is the price per...

-

A handrail, which weighs 120 N and is 1.8 m long. was mounted to a wall adjacent to a small set of steps (Figure P4.26). The support at A has broken, and the rail has fallen about the loose bolt at 8...

-

1. When equipment was purchased with general fund resources, which of the following accounts would have been increased in the general fund? a. Due from general fixed assets account group b....

-

The balance sheet of Roger, Susan, and Tom, who share partnership profits 30 percent, 30 percent, and 40 percent, respectively, included the following balances on January 1, 2011, the date of...

-

Pal Corporation has $108,000 income from its own operations for 2011, and $42,000 income from Sir Corporation, its 70 percent-owned subsidiary. Sirs net income of $60,000 consists of $66,000...

-

In 1984, the number of German marks required to buy one U.S. dollar was 1.80. In 1987, the U.S. dollar was worth 2.00 marks. In 1992, the dollar was worth 1.50 marks. In 1997, the dollar was again...

-

Todays spot rate is S 0 $ = $0.009057355. The 90-day forward rate is F 1 $ = $0.008772945. a. Calculate the forward premium on Japanese yen in basis points and as a percentage premium or discount...

-

Describe locational, triangular, and covered interest arbitrage.

Study smarter with the SolutionInn App