Question: Attached problem The following table gives information about transactions on the Balance of Payments accounts of Country X denoted in U.S.D ($) Value($) rovecrrracecerance assets

Attached problem

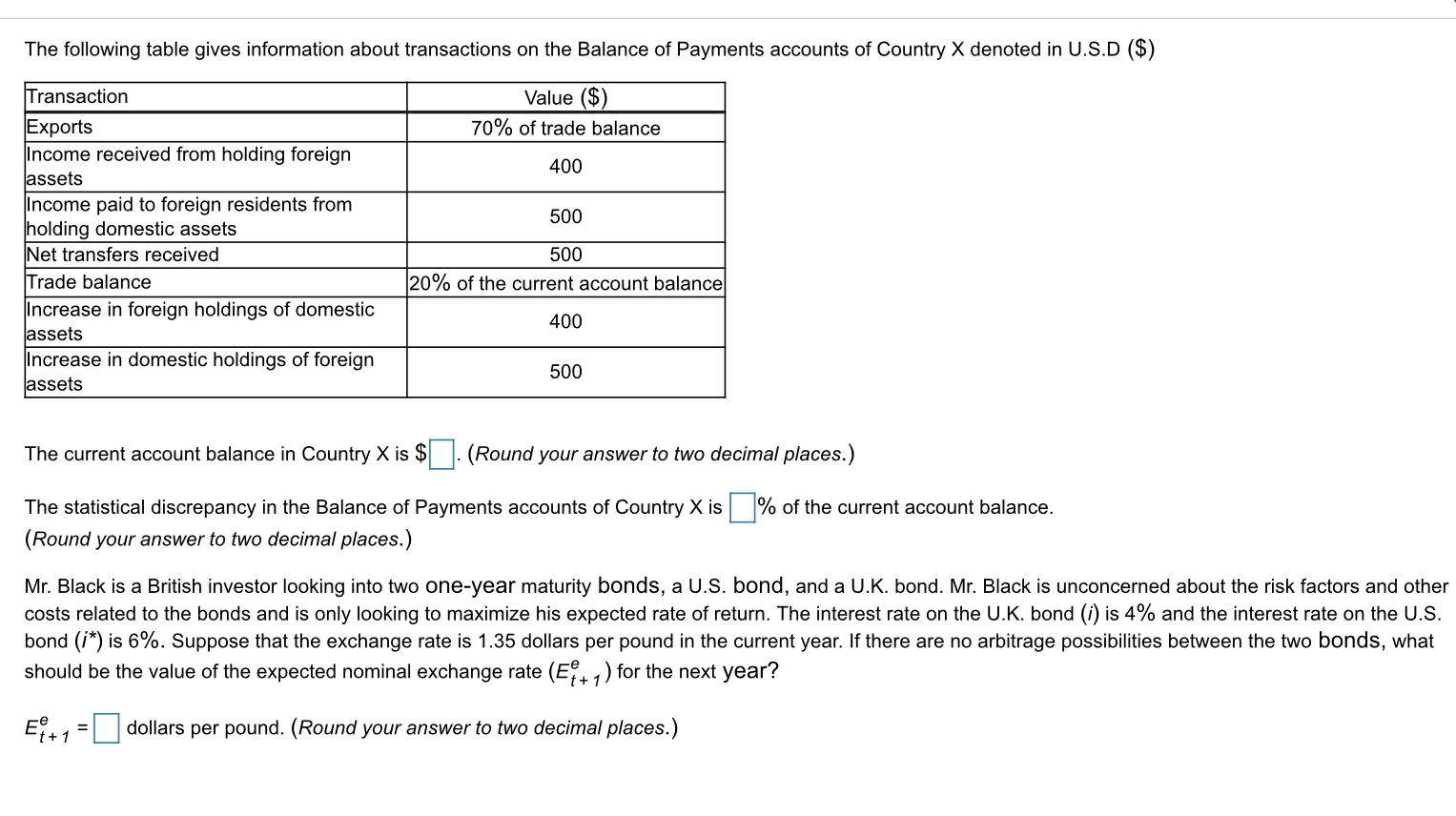

The following table gives information about transactions on the Balance of Payments accounts of Country X denoted in U.S.D ($) Value($) rovecrrracecerance assets holding domestic assets Nrecaveettranetereu sz_ _2o% at the current account balance assets Increase in domestic holdings of foreign assets The current account balance in Country X is $D. (Round your answer to two decimal places.) The statistical discrepancy in the Balance of Payments accounts of Country X is |:|% of the current account balance. (Round your answer to two decimal places.) Mr. Black is a British investor looking into two one-year maturity bonds, a US. bond, and a U.K. bond. Mr. Black is unconcerned about the risk factors and other costs related to the bonds and is only looking to maximize his expected rate of return. The interest rate on the U.K. bond (i) is 4% and the interest rate on the us. bond (P) is 6% Suppose that the exchange rate is 1. 35 dollars per pound in the current year. If there are no arbitrage possibilities between the two bonds. what should be the value of the expected nominal exchange rate (E?+1)forthe next year? Et+1=|:| dollars per pound. (Round your answer to two decimal places.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts