Question: auditing and assurance principles 2; given below are the data & requirements. thank you! The following is a partial list of the account balances, after

auditing and assurance principles 2; given below are the data & requirements. thank you!

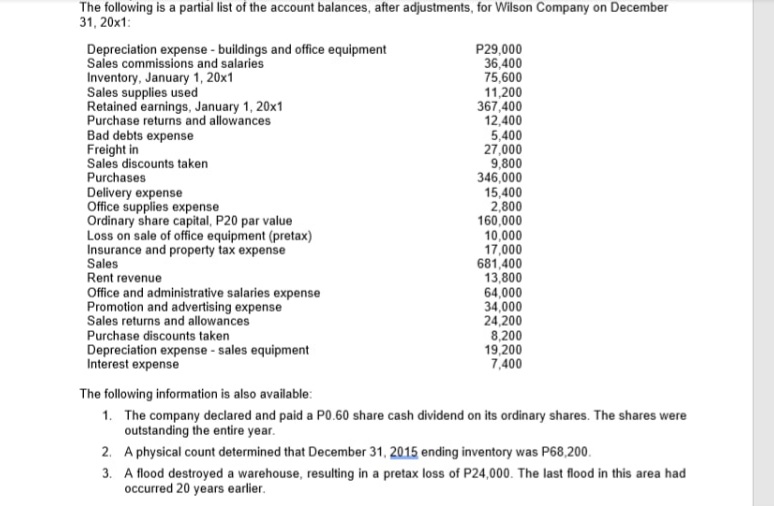

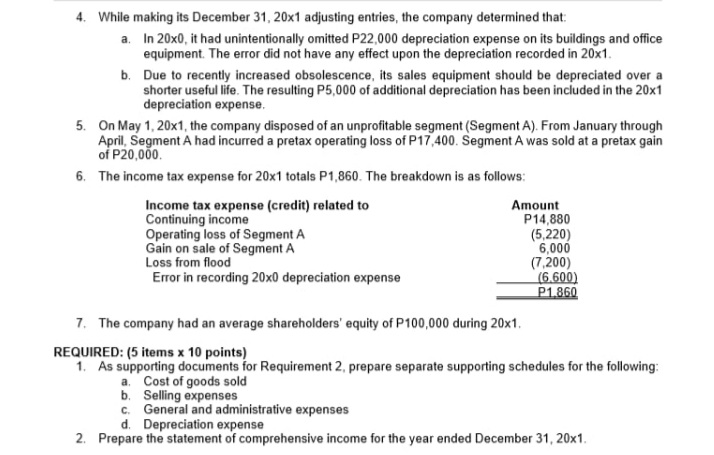

The following is a partial list of the account balances, after adjustments, for Wilson Company on December 31, 20x1: Depreciation expense - buildings and office equipment P29,000 Sales commissions and salaries 36,400 Inventory, January 1, 20x1 75,600 Sales supplies used 11,200 Retained earnings, January 1, 20x1 367,400 Purchase returns and allowances 12,400 Bad debts expense 5.400 Freight in 27,000 Sales discounts taken 9,800 Purchases 346,000 Delivery expense 15,400 Office supplies expense 2,800 Ordinary share capital, P20 par value 160,000 Loss on sale of office equipment (pretax) 10,000 Insurance and property tax expense 17,000 Sales 681,400 Rent revenue 13,800 Office and administrative salaries expense 64,000 Promotion and advertising expense 34.000 Sales returns and allowances 24,200 Purchase discounts taken 8.200 Depreciation expense - sales equipment 19,200 Interest expense 7,400 The following information is also available: 1. The company declared and paid a PO.60 share cash dividend on its ordinary shares. The shares were outstanding the entire year. 2. A physical count determined that December 31, 2015 ending inventory was P68,200. 3. A flood destroyed a warehouse, resulting in a pretax loss of P24,000. The last flood in this area had occurred 20 years earlier.4. While making its December 31, 20x1 adjusting entries, the company determined that: a. In 20x0, it had unintentionally omitted P22,000 depreciation expense on its buildings and office equipment. The error did not have any effect upon the depreciation recorded in 20x1. b. Due to recently increased obsolescence, its sales equipment should be depreciated over a shorter useful life. The resulting P5,000 of additional depreciation has been included in the 20x1 depreciation expense. 5. On May 1, 20x1, the company disposed of an unprofitable segment (Segment A). From January through April, Segment A had incurred a pretax operating loss of P17,400. Segment A was sold at a pretax gain of P20,000. 6. The income tax expense for 20x1 totals P1,860. The breakdown is as follows: Income tax expense (credit) related to Amount Continuing income P14,880 Operating loss of Segment A (5,220) Gain on sale of Segment A 6,000 Loss from flood (7,200) Error in recording 20x0 depreciation expense (6.600) P1 860 7. The company had an average shareholders' equity of P100,000 during 20x1. REQUIRED: (5 items x 10 points) 1. As supporting documents for Requirement 2, prepare separate supporting schedules for the following: a. Cost of goods sold b. Selling expenses C. General and administrative expenses d. Depreciation expense 2. Prepare the statement of comprehensive income for the year ended December 31, 20x1

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts