Question: Auditing Question Answer 11 Risks that may occur during assertion testing, but cannot be prevented due to the lack of time. 12 Reports that need

Auditing

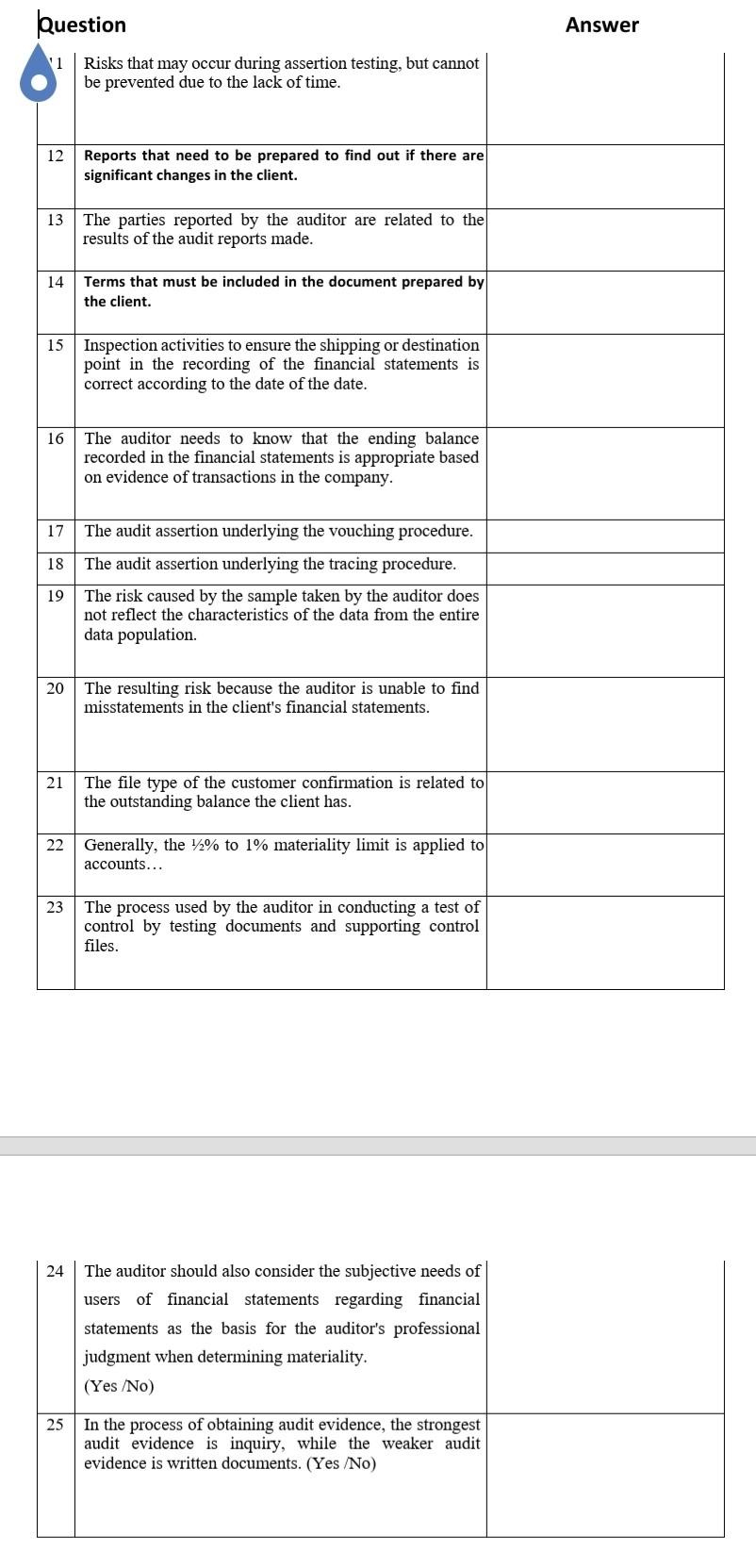

Question Answer 11 Risks that may occur during assertion testing, but cannot be prevented due to the lack of time. 12 Reports that need to be prepared to find out if there are significant changes in the client. 13 The parties reported by the auditor are related to the results of the audit reports made. 14 Terms that must be included in the document prepared by the client. 15 Inspection activities to ensure the shipping or destination point in the recording of the financial statements is correct according to the date of the date. 16 The auditor needs to know that the ending balance recorded in the financial statements is appropriate based on evidence of transactions in the company. 17 18 The audit assertion underlying the vouching procedure. The audit assertion underlying the tracing procedure. The risk caused by the sample taken by the auditor does not reflect the characteristics of the data from the entire data population. 19 20 The resulting risk because the auditor is unable to find misstatements in the client's financial statements. 21 The file type of the customer confirmation is related to the outstanding balance the client has. 22 Generally, the 12% to 1% materiality limit is applied to accounts... 23 The process used by the auditor in conducting a test of control by testing documents and supporting control files. 24 The auditor should also consider the subjective needs of users of financial statements regarding financial statements as the basis for the auditor's professional judgment when determining materiality. (Yes/No) 25 In the process of obtaining audit evidence, the strongest audit evidence is inquiry, while the weaker audit evidence is written documents. (Yes/No) Question Answer 11 Risks that may occur during assertion testing, but cannot be prevented due to the lack of time. 12 Reports that need to be prepared to find out if there are significant changes in the client. 13 The parties reported by the auditor are related to the results of the audit reports made. 14 Terms that must be included in the document prepared by the client. 15 Inspection activities to ensure the shipping or destination point in the recording of the financial statements is correct according to the date of the date. 16 The auditor needs to know that the ending balance recorded in the financial statements is appropriate based on evidence of transactions in the company. 17 18 The audit assertion underlying the vouching procedure. The audit assertion underlying the tracing procedure. The risk caused by the sample taken by the auditor does not reflect the characteristics of the data from the entire data population. 19 20 The resulting risk because the auditor is unable to find misstatements in the client's financial statements. 21 The file type of the customer confirmation is related to the outstanding balance the client has. 22 Generally, the 12% to 1% materiality limit is applied to accounts... 23 The process used by the auditor in conducting a test of control by testing documents and supporting control files. 24 The auditor should also consider the subjective needs of users of financial statements regarding financial statements as the basis for the auditor's professional judgment when determining materiality. (Yes/No) 25 In the process of obtaining audit evidence, the strongest audit evidence is inquiry, while the weaker audit evidence is written documents. (Yes/No)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts