Question: Aussie Dollar Forward. Use the following spot and forward bid-ask rates for the U.S. dollar/Australian dollar (US$ = A$1.00) exchange rate from December 10, 2010,

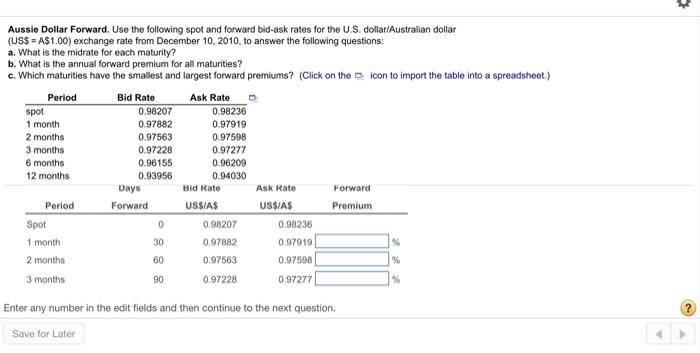

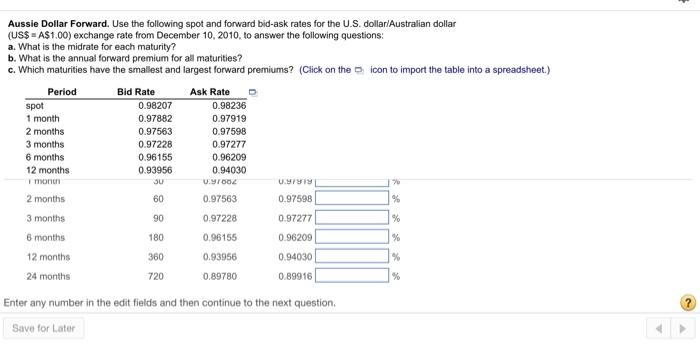

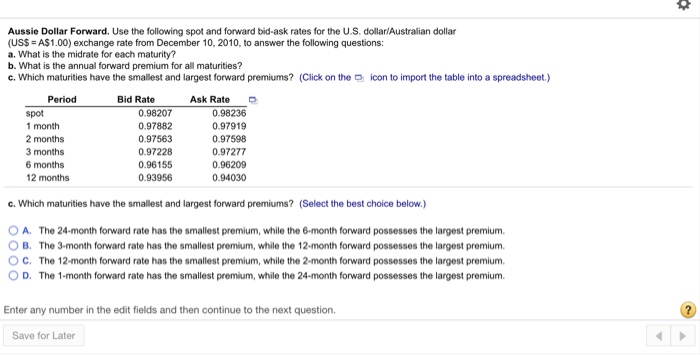

Aussie Dollar Forward. Use the following spot and forward bid-ask rates for the U.S. dollar/Australian dollar (US$ = A$1.00) exchange rate from December 10, 2010, to answer the following questions: a. What is the midrate for each maturity? b. What is the annual forward premium for all maturities? c, which maturities have the smallest and largest forward premiums? (Click on the-icon to import the table into a spreadsheet.) Period Bid Rate Ask Rate spot 1 month 2 months 3 months 6 months 12 months 0.98207 0.97882 0.97563 0.97228 0.96155 0.93956 0.98236 0.97919 0.97598 0.97277 0.96209 0.94030 Days Bid Kate Ask Kate Period Forward USSIAS USSIAS Spot 1 month 2 months 3 months 30 60 90 0.98207 0.97882 0.97563 0.97228 0.98236 0.97919 0.97598 0.97277 Enter any number in the edit fields and then continue to the next question. Save for Later

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts