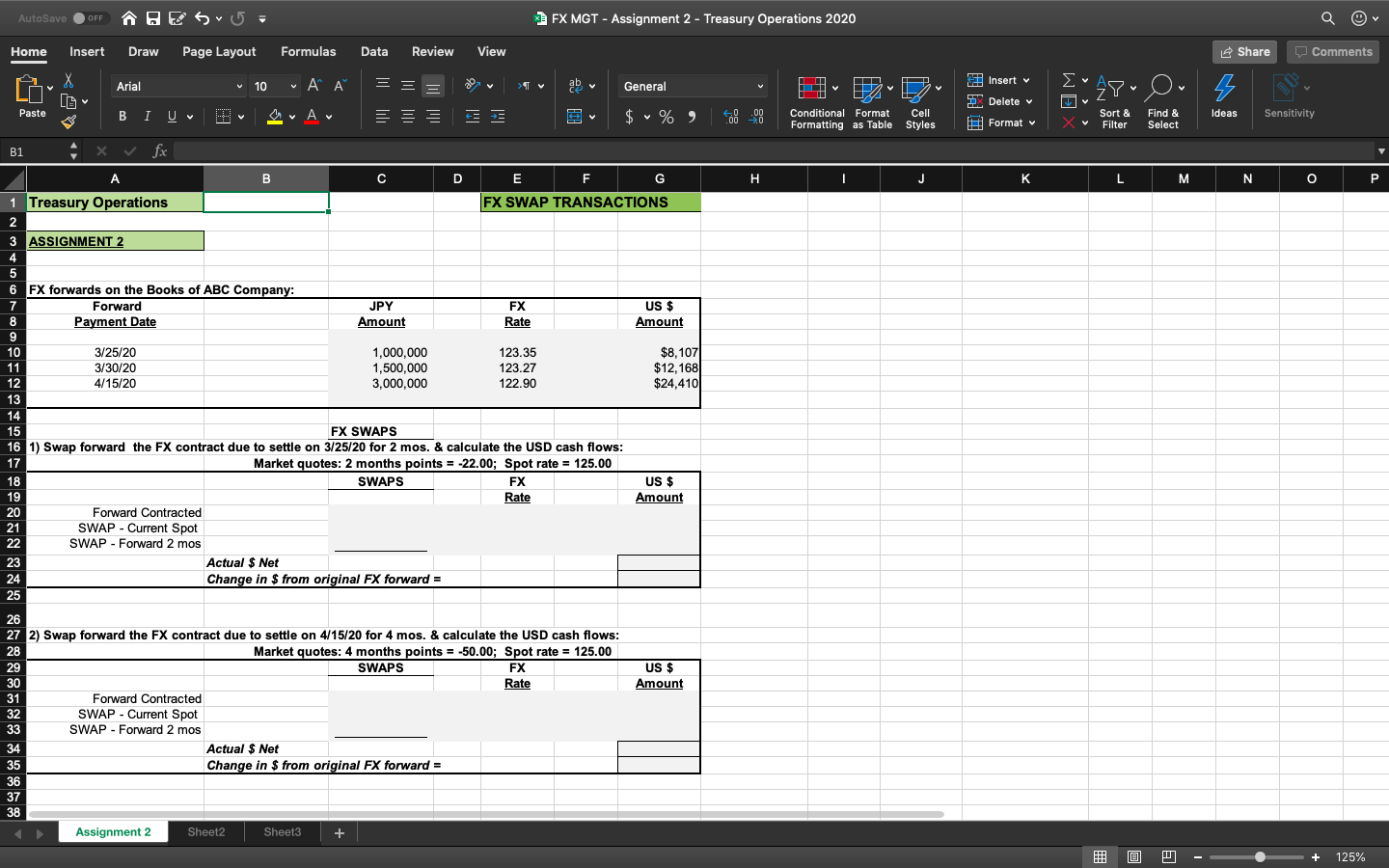

Question: AutoSave OFF THE Svo- FX MGT - Assignment 2 - Treasury Operations 2020 Home Insert Draw Page Layout Formulas Data Review View Share Comments Sou

AutoSave OFF THE Svo- FX MGT - Assignment 2 - Treasury Operations 2020 Home Insert Draw Page Layout Formulas Data Review View Share Comments Sou Tv aby General "Ayv O Z DS Cell Styles 23 Insert Delete Format Paste $ % ) 09 Conditional Format Formatting as Table Sort & XV Filter Find & Select ideas Sensitivity Arial 10 AA === BI U EU A E Bi xv fx A B C 1 Treasury Operations D E F G FX SWAP TRANSACTIONS H I J K L M N O P 3 ASSIGNMENT 2 6 FX forwards on the Books of ABC Company: Forward 8 Payment Date JPY Amount FX Rate US $ Amount 3/25/20 3/30/20 4/15/20 1,000,000 1,500,000 3,000,000 123.35 123.27 122.90 $8,107 $12,168 $24,4101 14 15 US $ Amount FX SWAPS 16 1) Swap forward the FX contract due to settle on 3/25/20 for 2 mos. & calculate the USD cash flows: 17 Market quotes: 2 months points = -22.00; Spot rate = 125.00 SWAPS FX Rate Forward Contracted SWAP - Current Spot SWAP - Forward 2 mos Actual $ Net Change in $ from original FX forward = US $ Amount 31 27 2) Swap forward the FX contract due to settle on 4/15/20 for 4 mos. & calculate the USD cash flows: Market quotes: 4 months points = -50.00; Spot rate = 125.00 SWAPS FX 30 Rate Forward Contracted 32 SWAP - Current Spot 33 SWAP - Forward 2 mos Actual $ Net Change in $ from original FX forward = Assignment 2 Sheet2 Sheet3 + @ 0 - - + 125% AutoSave OFF THE Svo- FX MGT - Assignment 2 - Treasury Operations 2020 Home Insert Draw Page Layout Formulas Data Review View Share Comments Sou Tv aby General "Ayv O Z DS Cell Styles 23 Insert Delete Format Paste $ % ) 09 Conditional Format Formatting as Table Sort & XV Filter Find & Select ideas Sensitivity Arial 10 AA === BI U EU A E Bi xv fx A B C 1 Treasury Operations D E F G FX SWAP TRANSACTIONS H I J K L M N O P 3 ASSIGNMENT 2 6 FX forwards on the Books of ABC Company: Forward 8 Payment Date JPY Amount FX Rate US $ Amount 3/25/20 3/30/20 4/15/20 1,000,000 1,500,000 3,000,000 123.35 123.27 122.90 $8,107 $12,168 $24,4101 14 15 US $ Amount FX SWAPS 16 1) Swap forward the FX contract due to settle on 3/25/20 for 2 mos. & calculate the USD cash flows: 17 Market quotes: 2 months points = -22.00; Spot rate = 125.00 SWAPS FX Rate Forward Contracted SWAP - Current Spot SWAP - Forward 2 mos Actual $ Net Change in $ from original FX forward = US $ Amount 31 27 2) Swap forward the FX contract due to settle on 4/15/20 for 4 mos. & calculate the USD cash flows: Market quotes: 4 months points = -50.00; Spot rate = 125.00 SWAPS FX 30 Rate Forward Contracted 32 SWAP - Current Spot 33 SWAP - Forward 2 mos Actual $ Net Change in $ from original FX forward = Assignment 2 Sheet2 Sheet3 + @ 0 - - + 125%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts