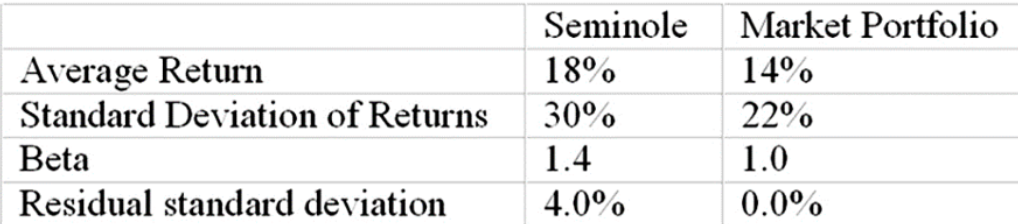

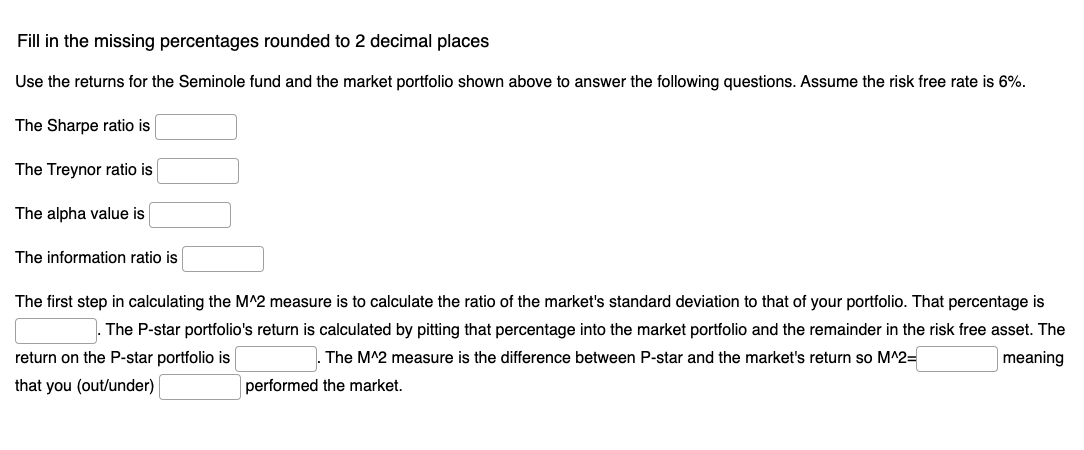

Question: Average Return Standard Deviation of Returns Beta Residual standard deviation Seminole 18% 30% 1.4 4.0% Market Portfolio 14% 22% 1.0 0.0% Fill in the missing

Average Return Standard Deviation of Returns Beta Residual standard deviation Seminole 18% 30% 1.4 4.0% Market Portfolio 14% 22% 1.0 0.0% Fill in the missing percentages rounded to 2 decimal places Use the returns for the Seminole fund and the market portfolio shown above to answer the following questions. Assume the risk free rate is 6%. The Sharpe ratio is The Treynor ratio is The alpha value is The information ratio is The first step in calculating the M^2 measure is to calculate the ratio of the market's standard deviation to that of your portfolio. That percentage is The P-star portfolio's return is calculated by pitting that percentage into the market portfolio and the remainder in the risk free asset. The return on the P-star portfolio is The M^2 measure is the difference between P-star and the market's return so M^2= meaning that you (out/under) performed the market

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts